The Day the Assembly Line Stopped: What the Ford Explorer Halt Really Signals

For more than a decade, rare earths sat in the “strategic risk” slide deck but rarely in the actual production incident log. That changed when, in early 2025, Ford halted Explorer production because it could not secure critical rare earth permanent magnets. At the same time, dysprosium was reported trading at around $1,125/kg and terbium at $4,500/kg in Western spot markets, at massive premiums to Chinese domestic pricing. This was not a debate about export policy in a conference room; it was an empty assembly line.

Materials Dispatch has seen rare earth issues disrupt margins, delay model launches, and force quiet motor redesigns. A complete halt of a mainstream vehicle program marks a different phase: critical materials are now a direct determinant of civilian industrial output, not just a background geopolitical worry. This briefing separates what is known from what is inferred, and argues that the Explorer halt is a systemic indicator, not an isolated misstep.

- The Ford Explorer halt in 2025 over rare earth magnet shortages marks a visible operational failure, not just a procurement headache.

- Dysprosium at $1,125/kg and terbium at $4,500/kg in Western spot markets highlight a bifurcated price system versus Chinese domestic markets.

- McKinsey projections of rare earth magnet demand rising from about 59,000 to 186,000 metric tons by 2035 point to a structural supply-demand squeeze.

- NdFeB magnet constraints now sit at the critical path for EV drivetrains and industrial motors, especially where high-temperature performance is non-negotiable.

- Operationally, magnet supply has moved from a Tier‑2 component issue to a board-level risk, with implications for design, sourcing, and regional industrial competitiveness.

FACTS: What Can Be Stated with Confidence

Ford’s 2025 Explorer Production Halt

In early 2025, Ford halted production of its Explorer line because it could not secure sufficient volumes of rare earth permanent magnets for key powertrain and systems components. Reporting around the episode linked the disruption specifically to shortages of neodymium-iron-boron (NdFeB) magnets containing heavy rare earth dopants for high-temperature performance.

The affected magnets are used in traction motors, power steering, and other critical systems where compact, high-torque, and high-efficiency performance is required. Substitute technologies exist (for example, induction or wound-rotor motors), but they require substantial redesign, validation, and retooling. As a result, the immediate lever available to the OEM was not rapid substitution, but line stoppage.

Dysprosium and Terbium Western Spot Prices in 2025

At the time of the Explorer halt, dysprosium was reported trading at around $1,125 per kilogram and terbium at approximately $4,500 per kilogram in Western spot markets. These levels represented substantial premiums to contemporary Chinese domestic prices for the same oxides and metals.

Dysprosium and terbium are heavy rare earth elements used in small quantities as dopants in NdFeB magnets to maintain coercivity and performance at elevated temperatures. High-temperature traction motors for EVs, hybrid systems, and industrial drives are typical applications. The price spike and premium over Chinese domestic levels are consistent with a situation in which:

- Chinese producers and consumers operate in a protected or semi-insulated domestic price environment.

- Export availability is constrained by a mix of policy, licensing, and internal demand prioritization.

- Western and allied buyers compete in a residual, thinner, higher-priced pool of material and finished magnets.

McKinsey Rare Earth Magnet Demand Projections to 2035

McKinsey analysis referenced in industry discussions projects that demand for rare earths used in permanent magnets could rise from roughly 59,000 metric tons to about 186,000 metric tons by 2035. The central drivers identified are:

- Rising global EV and hybrid vehicle production, particularly magnet-intensive permanent magnet synchronous motors.

- Expansion of renewable generation, especially wind power using direct-drive or hybrid-drive generators with NdFeB magnets.

- Growth in industrial automation, robotics, and high-efficiency motor use across manufacturing and logistics.

This projection implies roughly a threefold increase in demand for magnet-related rare earth oxides and metals over a decade-scale horizon. It assumes continued dominance of NdFeB-type systems in high-performance applications and only gradual penetration of alternative motor technologies.

NdFeB Magnets in EV and Industrial Motor Architectures

NdFeB (neodymium-iron-boron) permanent magnets are widely used in:

- Electric and hybrid vehicle traction motors, where high power density and efficiency are essential.

- Industrial motors and drives operating under continuous duty cycles and elevated temperatures.

- Robotics, automation systems, compressors, pumps, and HVAC units targeting energy efficiency standards.

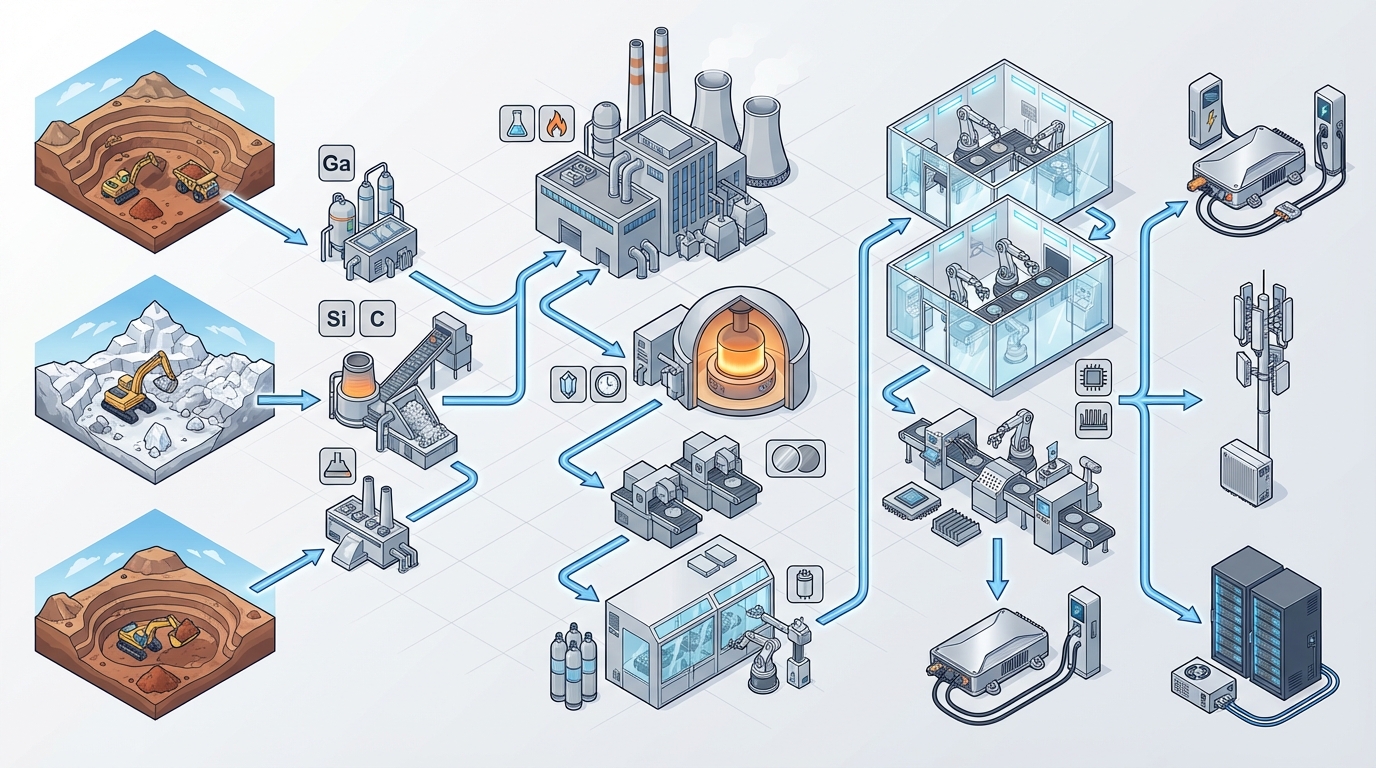

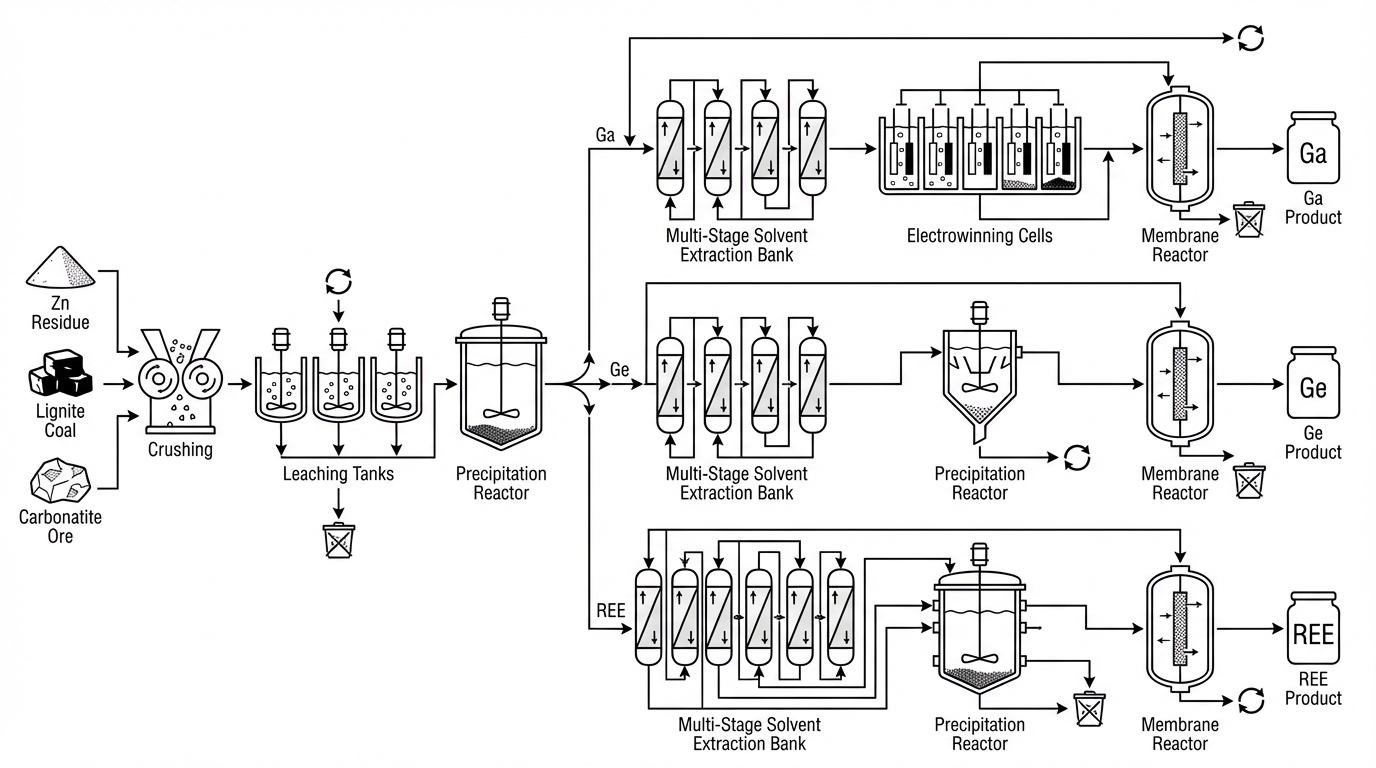

To meet temperature and coercivity requirements in drive motors, NdFeB magnets are often partially doped with dysprosium and, in more demanding cases, terbium. These heavy rare earths are much scarcer and more geographically concentrated than the light rare earths (such as neodymium and praseodymium). Processing and magnet fabrication capacity for high-Dy/Tb compositions has historically been heavily concentrated in China and, to a lesser extent, in Japan.

Across the past decade, several governments and corporate consortia have announced programs to expand non-Chinese mining, separation, and magnet-making capacity. However, as of the mid‑2020s, the bulk of high-performance NdFeB magnet production still traces back, directly or indirectly, to Chinese supply chains.

INTERPRETATION: How This Changes the Industrial Risk Map

The Ford Explorer halt is widely treated in technical and policy circles as a “wake-up call.” Materials Dispatch takes a harder view: it is not a wake-up call; it is the first widely visible casualty of a structural shift that was already underway. Several conditional readings follow from the facts above.

From Theoretical Risk to Binding Constraint

If a high-volume, mainstream vehicle platform can be halted for lack of rare earth magnets, then rare earth availability has crossed from “margin and sourcing issue” to “hard production cap” for Western automotive manufacturing. This event indicates that:

- Contingency sourcing for NdFeB magnets did not keep pace with the concentration of supply and the escalation of policy risk.

- Alternative motor architectures were not ready for rapid substitution at the required scale and certification level.

- Internal risk models underestimated the probability and impact of simultaneous shortages in both raw heavy rare earths and finished magnets.

Materials Dispatch has observed similar patterns at a smaller scale: industrial OEMs forced into last-minute redesigns to de-spec heavy rare earth content or shift torque curves because magnet suppliers quietly reallocated constrained material to defense or domestic customers. The Explorer halt extends this from engineering compromise into outright production stoppage.

A Bifurcated Market: Two Price Systems, Two Realities

Dysprosium at $1,125/kg and terbium at $4,500/kg in Western spot markets, trading at “massive premiums” over Chinese domestic prices, point to a de facto dual system:

- Inside China (and partially in closely integrated neighbors), prices reflect a large, captive ecosystem with policy-mediated stability and privileged allocation.

- Outside that ecosystem, prices reflect scarcity, policy risk premia, and the cost of ramping smaller, less integrated supply chains.

If this divergence persists, Western OEMs are effectively competing not against Chinese companies at the same input price, but against Chinese companies with structurally cheaper and more secure access to the same performance-critical materials. That is not a commodity disadvantage; it is a technology platform disadvantage, because permanent magnets sit at the heart of EV drivetrains, high-efficiency motors, and a growing slice of industrial automation.

McKinsey’s 59k-186k MT Projection: Demand Growth That Outruns Plausible Supply

McKinsey’s projection of magnet rare earth demand climbing from about 59,000 to 186,000 metric tons by 2035 sketches a future in which demand growth is not incremental but exponential. If that scenario materializes, several implications follow:

- Even aggressive, well-funded non-Chinese mining and separation ramp‑ups may only offset part of the increased pull, not replace existing Chinese dominance.

- NdFeB magnet capacity, rather than ore availability, is likely to remain the primary bottleneck, especially for high-Dy/Tb compositions.

- Product designers and platform planners face a moving constraint: what is technically optimal (high-Dy NdFeB) may be structurally unreliable in volume.

It is plausible that, under the high-demand end of this range, entire EV and industrial product segments will be defined more by magnet allocation than by consumer demand or assembly capacity. In that world, the Explorer halt looks less like an outlier and more like the first case study.

NdFeB Shortages: How They Cascade Through EV and Industrial Motors

NdFeB magnet shortages do not simply reduce output linearly. They force triage. Materials Dispatch has observed procurement and engineering teams forced into difficult allocations when magnet supply tightens:

- Prioritizing magnets for flagship EV and hybrid models while delaying lower-margin variants or ICE-electrification upgrades.

- Redirecting high-Dy/Tb compositions to applications with the harshest duty cycles (towing, fleet, off‑highway, industrial drives), leaving others with downgraded or redesigned motor options.

- Shifting some product lines to ferrite-based or induction motors, accepting trade-offs in efficiency, weight, or package size.

In industrial motors, similar patterns emerge: high-efficiency, premium motors continue to receive NdFeB magnets, while cost-sensitive segments risk a slide back toward less efficient technologies. This undercuts regulatory and corporate energy-efficiency objectives and complicates planning for utilities and grid operators expecting certain efficiency baselines in new industrial loads.

Governance Failures: When “Components” Were Treated Like Commodities

One uncomfortable conclusion from the Explorer incident is that many OEM governance structures treated magnets as generic components, not strategic chokepoints. In multiple supplier audits, Materials Dispatch has seen:

- Magnet supply chains mapped only to Tier 1 motor suppliers, with little visibility into upstream rare earth sourcing or processing.

- Risk registers that captured rare earths at the level of “critical materials” but did not tie them explicitly to model-specific production constraints.

- Capital allocation that favored visible end-assembly capacity over midstream partnerships in metals-to-magnets processing.

When dysprosium and terbium markets tightened, this lack of granularity translated into slow reaction times. The system was optimized to negotiate prices, not to secure physical availability under stress. By the time the magnet shortfall reached the Explorer line, the buffer of supplier inventories, alternative formulations, and short-term substitution options was already exhausted.

Policy Focus Misaligned: Mines vs. Magnets

Western policy responses in the early 2020s leaned heavily toward mine development and early-stage processing: supporting new rare earth projects, streamlining permitting, and funding separation plants. Those steps address part of the problem, but the Explorer halt argues that the system bottleneck now sits further downstream:

- Finished magnet capacity, particularly for high-coercivity NdFeB variants, remains concentrated in a small number of jurisdictions.

- Qualification cycles for new magnet plants into automotive and industrial platforms are long and complex, involving safety, reliability, and warranty considerations.

- Without robust metals-to-magnets infrastructure, new mines simply reroute ore back into the same constrained processing ecosystems.

If policy and corporate capital continue to over-weight upstream projects while under-weighting magnet manufacturing, then similar production halts are likely to appear in other vehicle programs and in industrial sectors. The Explorer case is best read as a stress test that the current configuration failed.

Procurement and Design: Late Convergence of Two Worlds

In practice, the rare earth crisis is forcing an overdue convergence between procurement and engineering. Historically, many organizations treated motor architecture as a fixed technical choice and magnet sourcing as a commercial exercise. The Explorer halt demonstrates that, for NdFeB-based systems:

- Design choices (magnet type, Dy/Tb loading, operating temperature margins) now embed long-term geopolitical and supply risk.

- Procurement strategies (single vs multi-sourcing, regional diversification, depth of transparency into Tier 2 and Tier 3) feed directly into production resilience.

- Board-level risk appetite around dependence on Chinese-centric supply chains is no longer an abstract ethical or political discussion; it connects to unit output and employment.

Materials Dispatch has already seen internal pressure rising from operations teams toward more integrated critical materials governance: cross-functional committees, deeper supplier audits, and formal scenario work on export controls and dual-pricing regimes. The Explorer halt is likely to accelerate that shift in other OEMs and industrial groups.

WHAT TO WATCH: Indicators of Whether This Was an Exception or the New Normal

Several observable signals will indicate whether the Explorer episode remains an outlier or becomes the template for Western industrial exposure to rare earths:

- Magnet plant announcements outside China: Concrete progress on NdFeB magnet facilities in North America, Europe, and allied Asian countries, including actual commissioning and automotive qualification, not just groundbreaking ceremonies.

- OEM disclosures on motor architectures: Shifts toward alternative motor technologies in new EV platforms, explicit mentions of reduced heavy rare earth dependence, or formal statements about magnet sourcing diversification.

- Export policy and licensing changes: Any tightening or loosening in Chinese export regimes for heavy rare earths, metals, and magnet technologies, and corresponding responses from Japan, the EU, and the U.S.

- Persistent price gaps: Ongoing or widening differentials between Chinese domestic and Western spot prices for dysprosium and terbium, signalling whether bifurcation is transitory or entrenched.

- Defense procurement behaviors: Evidence that defense programs are locking in long-term magnet supply in ways that crowd out civilian demand, especially for high-spec NdFeB products.

- Recurrent production disruptions: Any repeat of line halts or extended delays in other mainstream vehicle programs, heavy equipment lines, or industrial motor product families linked explicitly to magnet shortages.

- Recycling and substitution progress: Demonstrated, scaled use of rare earth recycling from end-of-life magnets and uptake of designs that lower or eliminate Dy/Tb content while retaining performance.

Conclusion

The 2025 Ford Explorer halt converts rare earth risk from a slide in a geopolitical deck into a visible hole in Western industrial output. Dysprosium and terbium’s elevated Western spot prices, far above Chinese domestic levels, expose a bifurcated system in which one industrial bloc controls both material and manufacturing depth, while another operates on residual access and price spikes.

If McKinsey’s high-end demand projection is even directionally correct, the Explorer episode will not remain unique. NdFeB magnets, especially high-temperature, heavy rare earth variants, are now a principal bottleneck for EV and industrial motor deployment. The critical question is whether corporate governance and public policy realign quickly enough toward the midstream magnets chokepoint rather than remaining fixated purely upstream.

For Materials Dispatch, this incident marks a clear transition: critical materials are no longer a background risk to be noted; they are a primary determinant of which factories run and which stand idle. Active monitoring of regulatory and industrial weak signals around magnets, heavy rare earths, and motor technologies will define how this story evolves.

Note on Materials Dispatch methodology Materials Dispatch integrates continuous monitoring of regulatory texts and administrative decisions in key jurisdictions with close tracking of industrial project developments and technology roadmaps. This briefing cross-references those regulatory and market signals with detailed analysis of end-use technical specifications in automotive and industrial motors to assess where materials constraints translate into real-world production risk.