China accounts for ~98% of global low-purity gallium, creating a structural supply choke point.

Export licensing (from Aug 2023) and a U.S.-targeted ban (announced Dec 3, 2024; suspended Nov 2025–Nov 2026) drove spot prices from about $240/kg to roughly $575/kg.

Ongoing licensing discipline and technology controls are likely to keep supply risk elevated through at least 2027.

Producers and downstream operators should map exposure, lock multi-year offtakes from non-Chinese sources, and build strategic stockpiles where feasible.

The Gallium Shock: Market Dynamics and Strategic Imperatives

Executive Summary

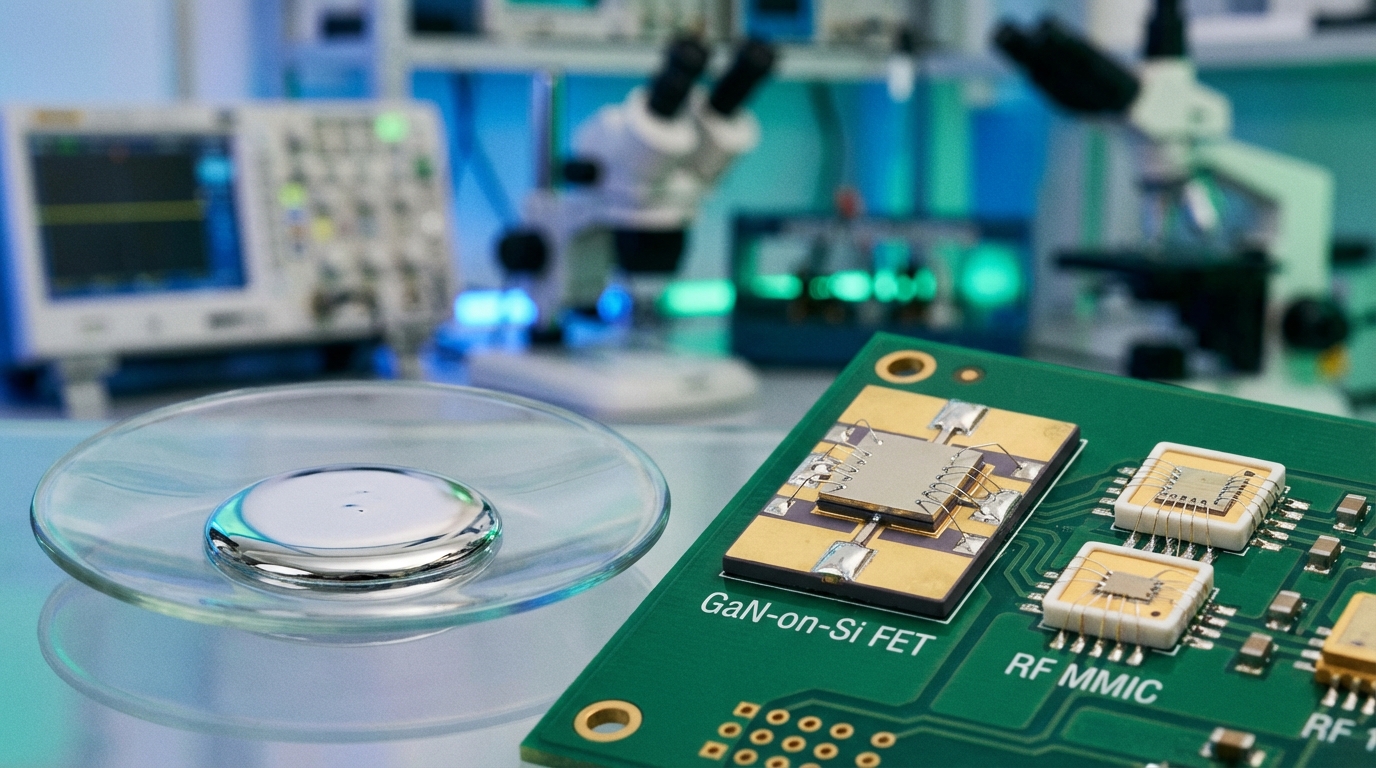

Materials Dispatch assesses how China’s near-monopoly on gallium—a byproduct metal vital for gallium-arsenide (GaAs) and gallium-nitride (GaN) semiconductors—has been leveraged through export licensing and a targeted restriction on U.S. shipments. Licensing controls since August 2023 and a Dec. 3, 2024 ban (suspended Nov. 2025–Nov. 2026) helped push spot prices from about $240/kg in mid-2023 to roughly $575/kg by December 2024. Crucially, the measures did not only constrain trade flows; they also tightened access to extraction technologies (notably ion-exchange/resin pathways). That combination supports structurally high supply risk through at least 2027, forcing semiconductor, defense, and power-electronics supply chains to move from scenario discussion to operational resilience planning.

Market Context and Supply Concentration

Gallium is recovered as a minor stream from aluminum and zinc refining, yet it underpins key technologies: RF front-ends, power electronics, radar, optical sensors, and high-efficiency LEDs. China controls approximately 98% of global low-purity output, creating a single-point failure dynamic for anything that depends on refined gallium supply. The strategic implication is straightforward: even when end-market demand is stable, licensing and technology controls can abruptly alter availability of material that downstream firms cannot easily substitute in the short run.

Before restrictions, U.S. exposure was especially sensitive because the supply chain was narrowly sourced and inventory depth was thin relative to the scale of semiconductor and defense demand. In practice, that means “spot” availability is not only a function of production capacity—it reflects whether qualified sellers can ship and whether customs clearance and end-use declarations remain acceptable under the licensing regime.

Policy Timeline and Price Impact

Licensing Shock (Aug 2023): Exports of gallium and germanium required MOFCOM licenses and end-use declarations (export licensing is a permit system where authorities review the exporter, end-user, and intended use). Chinese customs data indicated near-zero wrought gallium exports during the first months after controls tightened. Exports then reappeared at much lower volumes in October 2023—reflecting the compliance friction and discretionary nature of licensing. Spot markets responded quickly: prices moved higher by the October 2023 period, setting the tone for a prolonged repricing rather than a brief spike.

Global semiconductor supply chains rely heavily on Chinese gallium exports.

U.S. Ban & Technology Controls (Dec 3, 2024): MOFCOM escalated measures with a country-specific export ban on gallium, germanium, antimony, and superhard materials to the United States. At the same time, the export control catalogue was expanded to restrict gallium extraction technologies—specifically “technologies and processes to extract metallic gallium from alumina mother liquor using ion-exchange or resin methods.” That matters commercially because it targets the recovery pathway that supports conversion from feedstock streams into metal. Prices peaked at about $575/kg in December 2024 as buyers priced in both reduced trade access and reduced medium-term recovery optionality.

Partial Suspension (Nov 2025–Nov 2026): A temporary lift of the U.S. ban reduced political signalling risk but did not remove the underlying licensing and technology controls. As a result, downstream buyers should not interpret the suspension as a full return to “pre-shock” market normalcy; it primarily changes the risk of outright shipment prohibition to the U.S., while compliance requirements and technology restrictions continue to constrain the broader supply system.

Economic and Strategic Impacts

Gallium’s supply leverage becomes visible in how quickly disruptions propagate into manufacturing lead times. A gallium shortage is not like a commodity inventory issue that can be resolved through routine brokerage; it can interrupt component qualification cycles for GaAs/GaN RF and power devices, slow radar and sensor procurement timelines, and complicate substitution decisions across device architectures.

Regulatory attention also follows the supply logic. In Europe, gallium’s status as a strategic resource has been used to reinforce the policy focus on critical raw materials—an approach designed to support diversification, transparency, and stockholding where supply risk is concentrated. Taken together, these developments underline a market reality: the “real” constraint is not only mining or refining volumes, but the ability to legally and technically recover gallium into usable forms.

Gallium and gallium-based semiconductors are critical for power electronics and advanced communications.

Supply-Side Response

Global high-purity production and recycling are meaningful balancing factors, but the shock exposed how asymmetric the geography of upstream capability remains. Non-Chinese recovery projects have been announced across multiple jurisdictions, yet most are still at feasibility, engineering, or early implementation stages relative to the immediacy of downstream demand. That lag is economically important: even credible projects do not neutralize risk for lead times that can span quarters of device fabrication and qualification.

Recycling capacity outside China remains limited compared with the scale implied by global tightness. For industrial planners, that means the “supply response” is likely to be incremental rather than immediate—pushing the market toward a longer period of negotiated offtakes, careful quality management, and higher dependence on storage and contracted procurement.

Scenarios & Probabilities

Managed Constriction (Base Case, ~60%): Licensing remains discretionary and technology controls remain in place. Price premiums persist as buyers continue to source via contracted channels rather than pure spot purchasing, while non-Chinese capacity additions gradually improve medium-term availability toward the late 2020s.

Escalation & Crackdown (High Stress, ~25%): Renewed geopolitical tensions increase the likelihood of targeted enforcement, re-export scrutiny, and sharper shipment restrictions. The outcome is less about total global output and more about sudden loss of route access—driving acute shortages and episodic spikes.

Diversification Relief (Optimistic, ~15%): Alliances deepen and recovery pathways diversify. Alternative resin and processing compliance pathways, plus more robust upstream contracting, reduce reliance on Chinese-origin supply and gradually ease pricing pressure toward earlier baselines.

Actionable Intelligence

Materials Dispatch recommends a three-horizon response:

Immediate (Next 4 Weeks): Map gallium exposure to Tier-3 suppliers (not just cell or device assemblers). Stress-test inventories against a six-month cutoff scenario, and review force-majeure plus re-export clauses to ensure contractual compliance aligns with export licensing requirements and end-use documentation expectations.

Short-Term (Next Quarter): Secure multi-year offtake agreements with non-Chinese recovery/refining counterparties where quality and compliance can be validated. Align corporate stockpile targets with national or consortium initiatives (including programs referenced in U.S. and EU contexts, such as Project Vault and EU critical-material policy efforts), focusing on the material forms actually required by downstream processes.

Long-Term (Through 2027+): Co-invest in upstream recovery and recycling pathways, and integrate gallium risk into fab siting and product qualification planning. Codify critical-material playbooks for single-supplier and route-access scenarios to prevent procurement decisions from being driven solely by spot price movements.

Signals to Monitor

Price Levels: Track European and global spot markers closely, but treat large price prints as a sign of route-risk and licensing friction—not just supply scarcity.

Policy Updates: Monitor MOFCOM notices for changes in licensing mechanics, expansions or clarifications of extraction-technology controls, and any further updates to U.S. ban suspension timing after Nov 2026.

Re-export Flows: Watch for discrepancies between Chinese export reporting and U.S./EU import data, particularly when routing intermediates appear to increase.

Project Milestones: Prioritize announcements tied to FID and commissioning timelines for non-Chinese recovery capacity, since earlier-stage plans do not address near-term procurement constraints.

Stockpile Actions: Follow public procurement developments and strategic-reserve frameworks that attempt to translate policy intent into physical availability.

Conclusion

China’s export licensing and the U.S.-targeted ban have crystallized gallium’s role as a strategic lever in semiconductor and defense supply chains. With technology controls aimed at extraction pathways, tightness risk is likely to remain elevated through at least 2027 even when the U.S. shipment restriction is temporarily suspended. Operators should accelerate exposure mapping, diversify sourcing through credible non-Chinese projects, and institutionalise strategic stockpiling and contractual compliance to reduce vulnerability to future route disruptions.

Materials Dispatch has seen too many “one-off” disruptions in critical materials turn into structural regime shifts: China’s rare earth export quotas in the early 2010s, COVID-era logistics breakdowns, and more recent titanium and gallium restrictions. Each time, buyers and compliance teams tended to dismiss the first signals, only to scramble once paperwork and cargo were already blocked. MOFCOM Announcement 61 fits that same pattern, but with a twist: it targets the global downstream, not just exports at China’s border.

Across automotive, aerospace, wind energy and defense supply chains that Materials Dispatch has reviewed, rare earths are still treated as invisible trace materials: a magnet, a phosphor, a polishing powder, buried deep in bills of materials and safety data sheets. MOFCOM Announcement 61 effectively drags those traces into the center of regulatory risk management. For any organization that cares about supply security, compliance exposure, and strategic autonomy, ignoring this rule looks less and less defensible.

Key Points

MOFCOM Announcement 61 (October 2025) introduces an export licensing requirement tied to 0.1% or more Chinese-origin rare earth content in products, including those manufactured outside China.

The rule is explicitly extraterritorial: non-Chinese manufacturers shipping products that cross the 0.1% threshold are brought into a Chinese licensing process if Chinese-origin rare earths are involved.

Enforcement is formally suspended until November 27, 2026, creating a finite window before full application; voluntary compliance reporting is encouraged during this period.

Legal analyses (GvW, Clark Hill) frame the measure as comparable in ambition to U.S. ITAR extraterritorial controls, but applied to a far broader, largely commercial set of downstream products.

If enforced as written, the rule would force compliance, purchasing and engineering teams to establish traceable rare earth provenance and content quantification down to the 0.1% level across complex global supply chains.

FACTS: What MOFCOM Announcement 61 Actually Says and How It Is Structured

Core scope and legal framing

MOFCOM Announcement 61, issued in October 2025, is formally presented by China’s Ministry of Commerce as an export control measure covering certain rare earth elements (REEs) and related items. The Announcement places rare earth oxides, metals, alloys, compounds and selected downstream products under a licensing regime when exported from China.

The text goes significantly further than traditional export controls that only regulate goods leaving the jurisdiction in which they were produced. Announcement 61 explicitly extends its reach to “products manufactured outside the territory of the People’s Republic of China” that contain specified rare earth content originating in China, provided that such products are exported and meet defined thresholds. This is the anchor of the rule’s extraterritorial character.

The 0.1% Chinese-origin rare earth content threshold

A central technical feature of Announcement 61 is the quantitative trigger: an export license is required where the cumulative content of Chinese-origin rare earth elements in a product exceeds 0.1% by weight in the finished good. This threshold is applied to all Chinese-sourced REEs present in the item, aggregated across oxides, metals, alloys, compounds and embedded materials such as permanent magnets.

The rule is designed to capture both relatively simple products (for example, individual rare earth magnets) and complex assemblies where rare earths are only one among many materials: electric vehicle traction motors, wind turbine generators, avionics, guidance systems, or high-performance alloys used in aerospace and defense applications.

Announcement 61 and accompanying technical guidance indicate that compliance assessments may rely on high-sensitivity analytical methods such as inductively coupled plasma mass spectrometry (ICP-MS) or equivalent laboratory techniques. The explicit reference to analytical chemistry methods makes clear that the 0.1% level is intended as an enforceable quantitative threshold, not merely a nominal figure.

Extraterritorial reach and obligations for entities outside China

The legal text covers “any products manufactured outside China” that incorporate Chinese-origin REEs above the 0.1% threshold and are destined for export, regardless of where the manufacturer is established. In practice, this means that a factory in Europe, North America or Southeast Asia would fall under the scope of Announcement 61 if it uses Chinese-origin rare earth materials and its finished products are exported in ways that intersect Chinese jurisdiction or logistics.

For covered transactions, the rule requires an export license to be obtained from MOFCOM before shipment. License applications are to be submitted via MOFCOM’s online portal and must include, at a minimum:

Identification of all rare earth elements present in the product and confirmation of which portion is of Chinese origin.

Details of the processing chain for the Chinese-origin REEs, including intermediaries and processing locations.

Information on the final product type and technical characteristics.

Declared end use and end-user information, in line with standard export control practice.

These requirements essentially create a documentation regime for rare earth provenance and end-use, anchored in Chinese administrative procedures, that attaches to non-Chinese manufacturing where Chinese-origin REEs are present above the threshold.

Suspension of enforcement and key dates

Announcement 61 was initially framed for enforcement beginning on January 1, 2026. that said, an addendum issued on December 1, 2025, suspended full enforcement until November 27, 2026. During this suspension period:

Global REE supply flows with laboratory testing inset.

The 0.1% rule and associated licensing provisions remain on the books but are not applied to block exports in the normal course.

MOFCOM encourages voluntary submission of information and trial use of the licensing portal, effectively treating the period as a live pilot phase.

The Announcement and addendum specify that after the suspension expires, shipments that fall under the rule and are not properly licensed may be subject to measures including denial of export licenses, seizure at Chinese ports, and administrative sanctions such as inclusion on Chinese blacklists.

Public reporting and legal commentaries describe this suspension as linked to ongoing trade and security negotiations, but the legal text itself is clear on one point: the rule is deferred, not withdrawn, and a specific enforcement date is set for late November 2026.

Exemptions and special provisions

Announcement 61 and related guidance outline limited exemptions. These include specific carve-outs for humanitarian aid and certain categories of academic or scientific research materials, subject to case-by-case approval. There are also provisions for pre-approved defense contracts where Chinese entities are formal partners and where end-use and end-user are already known to Chinese authorities.

Notably, there is no general exemption for Western or other foreign original equipment manufacturers (OEMs). Dual-use items that could serve both civilian and military purposes, such as rare earth-based alloys used in aerospace components, are explicitly flagged as sensitive and are expected to require detailed end-user certificates and more intensive scrutiny.

Legal and policy context: comparison to U.S. ITAR extraterritorial controls

Several law firms, including GvW in Europe and Clark Hill in the United States, have analyzed Announcement 61 against the backdrop of existing extraterritorial control regimes. The most consistent point of reference is the U.S. International Traffic in Arms Regulations (ITAR), which regulate defense articles, services and technical data and extend U.S. jurisdiction to foreign-made products that incorporate controlled U.S.-origin content.

The ITAR regime is long-standing and focuses primarily on defense and national security-related items. Any foreign product that incorporates ITAR-controlled components or technical data can be subject to U.S. licensing requirements, regardless of where the final product is manufactured or exported. That is the core extraterritorial precedent.

Announcement 61 does something conceptually analogous: it asserts Chinese regulatory authority over foreign-manufactured products based on the origin and presence of a particular material class (Chinese-sourced REEs), above a defined percentage. However, its scope is structurally different. Instead of targeting a narrow set of explicitly military articles, it potentially reaches a much broader and more commercially oriented universe of goods where rare earths play enabling roles: electric vehicles, grid and wind power equipment, consumer electronics, industrial automation, and many more.

INTERPRETATION: How This Rule Rewires Compliance, Sovereignty, and Industrial Planning

From “export control” to extraterritorial regulatory claim

On its face, Announcement 61 is an export control regulation. In substance, to the extent that it is enforced as written, it behaves more like a broad extraterritorial regulatory claim over a material class and its downstream embodiments worldwide. Labeling this merely as “China’s latest export control” understates the shift.

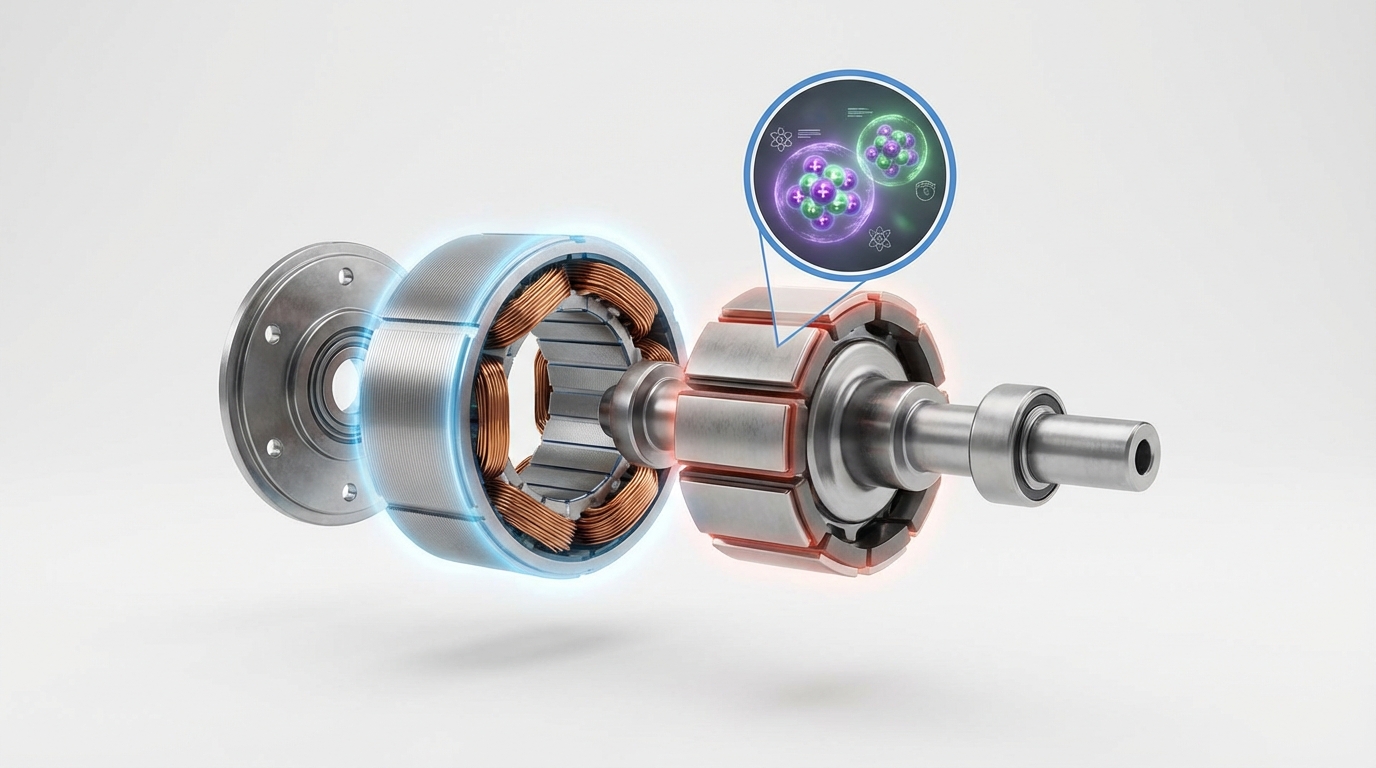

Exploded view of an EV motor and magnet with microscopic trace-level magnification.

The core move is simple but consequential: China ties its licensing power not only to the act of exporting goods from its territory, but also to the historical fact that material originated in Chinese mines and refineries, wherever that material is subsequently transformed. That logic is familiar from ITAR and other strategic trade controls, but applying it to rare earth content above 0.1% pulls an enormous swath of otherwise “normal” industrial and consumer products into a defense-style regulatory perimeter.

If that perimeter becomes operational, China effectively gains a compliance lever over foreign plants whose only connection to Chinese jurisdiction is the original sourcing of REEs in their components. From a sovereignty perspective, this is a direct challenge to the assumption that regulatory control over a factory’s outputs lies solely with the country in which that factory operates.

Compliance at the molecular level: data, labs, and supply chain transparency

The 0.1% threshold, combined with the requirement to identify Chinese-origin content, implies a level of traceability and materials characterization that most commercial supply chains have not yet internalized. Materials Dispatch has seen even sophisticated OEMs struggle to answer basic questions about rare earth content deeper than Tier 1 suppliers, let alone to distinguish Chinese-origin fractions from non-Chinese material in multi-source blends.

If enforcement proceeds on schedule after November 27, 2026, compliance teams would need reliable answers to three interlocking questions for any product that might intersect Announcement 61:

Is there rare earth content at all? Many companies currently do not have structured databases capturing REE usage across all components and subassemblies, particularly for legacy products.

What is the total rare earth mass fraction in the finished good? This requires bills of materials aligned with realistic density and composition data, or access to lab testing when documentation is incomplete.

What share of that content is Chinese-origin? This is the most challenging dimension, demanding provenance declarations from suppliers and, in many cases, from their own upstream providers.

Analytical techniques like ICP-MS can technically resolve rare earth content well below 0.1%, but lab capacity, sample preparation, and cost considerations limit the feasibility of routine testing for every product line. Without structured provenance data from suppliers, companies would be forced into probabilistic assumptions that may not satisfy regulators, whether in Beijing or in other capitals responding to the rule.

Sectors most exposed: automotive, aerospace, wind, and defense

Materials Dispatch’s review of bills of materials and supplier maps across key sectors suggests that some industries are structurally more exposed to Announcement 61 than others, purely due to their dependence on rare earth-intensive components.

Automotive and EVs. Electric vehicle traction motors, power steering systems, and a growing set of comfort and safety features rely on permanent magnets and sensors that often contain neodymium, praseodymium, dysprosium and related REEs. In many current designs, the rare earth content in a motor or actuator is comfortably above 0.1% by weight. If any fraction of that rare earth stream is Chinese-origin, the finished vehicle or subassembly could fall under Announcement 61 when exported in certain trade flows.

Aerospace. High-temperature alloys, actuators, radar systems, and other avionics frequently incorporate REEs for performance reasons. Dual-use status is common, blurring civilian and military categories. For aerospace OEMs that already juggle ITAR, EU dual-use regulations and other national regimes, the introduction of a Chinese-origin REE trigger adds another compliance dimension that cuts across existing classification schemes.

Wind energy and grid equipment. Direct-drive wind turbine generators and high-efficiency grid equipment use large volumes of rare earth magnets. Given their size and composition, the 0.1% threshold is easily exceeded. Projects exporting components or complete systems along routes that intersect Chinese jurisdiction or logistics channels may find themselves unexpectedly grappling with MOFCOM licensing requirements.

Conceptual ‘REE passport’ ledger for provenance tracking.

Defense and advanced security applications. Guidance systems, precision munitions, electronic warfare equipment and secure communications all have rare earth heavy components. In many defense-industrial cases, there is already a push to reduce dependence on Chinese-origin REEs due to strategic concerns. Announcement 61 adds a legal and administrative dimension to that strategic logic, especially for systems that combine U.S. ITAR-controlled technology with Chinese-origin materials.

ITAR as mirror and warning: what extraterritorial control looks like in practice

Compliance professionals familiar with U.S. ITAR and related regimes have a living example of how extraterritorial controls reshape industrial behavior over time. Under ITAR, non-U.S. companies building systems that incorporate controlled U.S. components or technical data have gradually restructured supply chains, documentation practices and even R&D programs to manage licensing risks.

If MOFCOM applies Announcement 61 with similar consistency and duration, a comparable pattern could emerge around rare earth sourcing and documentation, with a few critical differences:

ITAR is anchored in a narrow category of clearly defense-related items; Announcement 61 reaches into mainstream industrial products whose primary use is civilian.

ITAR is administered by the United States, a country that is a key but not dominant supplier of most materials; China currently plays a uniquely large role in rare earth mining and processing, which magnifies the leverage of any origin-based rule.

Companies have had decades to internalize ITAR compliance; Announcement 61 compresses its adaptation timeline into the period leading up to and following November 27, 2026.

Legal commentaries from GvW and Clark Hill converge on one uncomfortable point: even if foreign courts ultimately reject the extraterritorial claim in principle, companies whose goods transit Chinese ports or who depend on Chinese-origin rare earth inputs will experience the rule as practically binding. In that sense, the question becomes less “Is this jurisdictionally legitimate?” and more “How much supply chain flexibility exists to avoid or accommodate it?”

Why many OEMs are still slow to react

Despite the potential reach of Announcement 61, Materials Dispatch encounters a striking disconnect in discussions with automotive, industrial and energy equipment producers. In many cases, the regulation is known in headline form but parked in the “future risk” bucket, with the suspension to November 2026 interpreted as a signal that the rule may never bite.

Three structural reasons appear repeatedly:

Rare earths are still invisible in governance structures. Corporate materials risk frameworks often treat REEs as a subset of “other metals”, without specific key performance indicators or dedicated reporting to boards and regulators. What is not explicitly measured is rarely prioritized in compliance roadmaps.

Data gaps run deep beyond Tier 1. Even where companies have invested heavily in human rights and carbon-footprint traceability, those systems typically track mine of origin and processing for a handful of flagship materials (for example, cobalt, lithium, nickel). Rare earths, particularly in magnets and specialized alloys, are often entirely absent from those dashboards.

Suspension breeds complacency. The 2026 enforcement date feels distant in annual planning cycles dominated by nearer-term cost, product launch and regulatory deadlines. That tends to push rare earth provenance workstreams down the queue, especially when they involve complex engagement with Tier 2 and Tier 3 suppliers.

The risk is not that every clause of Announcement 61 will immediately and uniformly apply on November 28, 2026. The more realistic concern is that enforcement begins in targeted areas-particular sectors, routes, or end-use categories-and catches unprepared supply chains at precisely the weak points where alternative sourcing is hardest.

WHAT TO WATCH: Signals That Will Define How Far the 0.1% Rule Reaches

Implementing rules and FAQs from MOFCOM. Detailed guidance on how Chinese origin will be determined, what documentation is deemed sufficient, and how mixed-origin material is treated will reveal how administratively aggressive the regime is intended to be.

Behavior during the suspension window. Even while formal enforcement is paused, patterns in voluntary filings, licensing trials and treatment of “test cases” at ports will indicate how strictly the 0.1% threshold may be applied in practice.

Alignment with other Chinese controls. Links between Announcement 61 and existing export restrictions on sensitive technologies (for example, AI chips, advanced materials) would signal an integrated strategy rather than a stand-alone measure.

Corporate disclosures and board-level attention. The appearance of Announcement 61 in public risk factor disclosures, ESG reports, or board committee agendas will show which sectors are beginning to internalize the rule as more than a theoretical concern.

Development of rare earth traceability tools. Growth in specialized software, certification schemes and lab capacity aimed at REE provenance would indicate that industry is operationalizing compliance, not merely discussing it.

Diplomatic and WTO-level reactions. Formal challenges or coordinated responses from other major economies-whether in trade fora or through their own countervailing measures—will shape how sustainable China’s extraterritorial stance is over the medium term.

Interaction with ITAR and allied controls. Cases where a single product is simultaneously captured by ITAR and Announcement 61 will be especially revealing, testing how companies and governments navigate overlapping, and potentially conflicting, extraterritorial claims.

Conclusion

MOFCOM Announcement 61’s 0.1% rule is not just another twist in the long story of rare earth export policy. It is an explicit attempt to anchor regulatory authority in material origin and carry that authority downstream, across borders and into factories that have never considered themselves under Chinese jurisdiction. For any organization that depends indirectly on Chinese-sourced rare earths, the legal text moves the conversation from abstract “overdependence” to concrete licensing risk.

Whether the rule ultimately operates as a narrow, selectively enforced tool or as a broad, normalized compliance regime will depend on choices made in Beijing, responses in Washington, Brussels and other capitals, and the degree to which industrial players build real visibility into their rare earth footprints. Materials Dispatch will continue active monitoring of regulatory and industrial weak signals that will determine which of these paths becomes reality.

Note on Materials Dispatch methodology Materials Dispatch bases this briefing on direct readings of official regulatory texts and implementing documents, continuous monitoring of communications from trade and export control authorities, and cross-checks with legal analyses such as those from GvW and Clark Hill. This is combined with bottom-up mapping of critical material usage in end-use sectors and technical specifications, in order to connect abstract rules to the actual behavior of automotive, aerospace, energy and defense supply chains.

Project Vault: How a $10 Billion Stockpile Quietly Rewired Critical Minerals Policy

Materials Dispatch cares about Project Vault for a blunt reason: this is the first time since the Cold War that the United States and a broad coalition of partners have decided that rare earths, cobalt, gallium, and other strategic inputs are too important to leave to a mostly uncoordinated spot market. Clients allocate multi‑year budgets to secure these materials; suppliers and traders structure portfolios around them. Every time Chinese export controls choke gallium flows, or rare earth shipments stall in a port strike, procurement teams have to rewrite playbooks in real time. Project Vault turns those ad‑hoc stress tests into a permanent policy environment.

For Materials Dispatch, the inflection point was the sequence of shocks between 2020 and 2025: COVID‑era logistics breakdowns, the 2023 Chinese export license regime on gallium and germanium, and rolling rumors of rare earth quota tightening. Each episode forced defense primes, EV supply chains, and magnet makers to overpay for last‑minute tonnage or accept production delays. Against that backdrop, a $10 billion U.S. strategic stockpile, tied to a 55‑nation preferential trade framework with price support mechanisms, is not a marginal policy tweak; it is a structural rewrite.

Key points

Project Vault commits $10 billion to U.S.-led critical minerals stockpiling, procurement, and allied capacity building, announced at the February 2026 Critical Minerals Ministerial in Washington.

A 55‑nation “Minerals Security Alliance” framework layers preferential trade and price support mechanisms over Vault, effectively carving out a bloc market for non‑Chinese supply.

Compared with the legacy U.S. National Defense Stockpile and allied reserves, Vault is larger, more targeted to REEs and battery metals, and explicitly linked to pricing floors and tender schedules.

If implemented broadly as announced, Vault and the alliance framework could structurally reroute supply, narrow arbitrage for traders, and hard‑wire provenance and compliance expectations into contracts.

Execution risks are significant: intra‑bloc tensions, verification challenges, and potential Chinese countermeasures could limit how far the framework actually shifts market power.

FACTS: What Project Vault and the 55‑Nation Framework Actually Do

1. Core design of Project Vault

At the February 2026 Critical Minerals Ministerial in Washington, D.C., the United States announced Project Vault, a critical minerals stockpiling initiative with an initial $10 billion commitment. The program is structured around three pillars:

Acquisition and storage: A multi‑year acquisition program for strategic minerals, including rare earth oxides (with emphasis on neodymium, praseodymium, and dysprosium), cobalt, gallium, lithium, and nickel, paired with investments in storage and handling infrastructure.

Domestic processing incentives: Funding to expand U.S. processing and refining capacity for these materials, complementing the physical stockpile and aiming to reduce dependence on foreign refining, particularly from China.

Allied capacity building: Support for partner countries’ mining and processing projects, tied to the broader preferential trade framework agreed at the same ministerial.

According to U.S. government statements, Vault is designed as a standing buyer through structured tenders, not a one‑off procurement. Program documents describe recurring tenders for rare earth oxides and cobalt, targeting a strategic reserve equivalent to a significant share of combined defense and electric vehicle demand over a defined multi‑year horizon. The funding draw reportedly rests partly on Defense Production Act authorities and recent industrial policy legislation.

Compared to the pre‑Vault U.S. National Defense Stockpile (NDS), which held relatively modest tonnages of rare earths and focused heavily on legacy metals such as beryllium, chromium, and titanium, Vault explicitly prioritizes materials that underpin permanent magnets, advanced electronics, and battery chemistries. NDS operations historically lacked explicit price support mechanisms; Vault’s architecture directly contemplates interacting with market price signals.

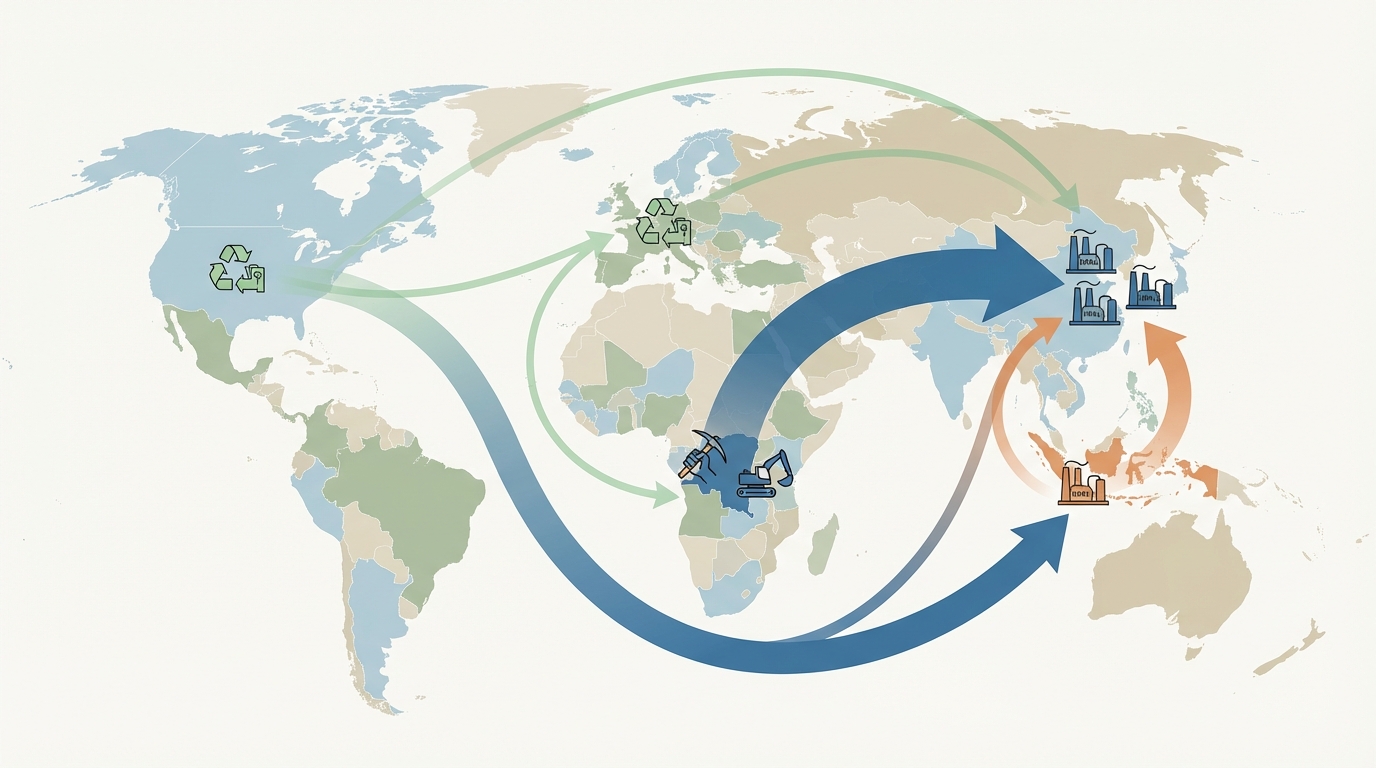

2. The 55‑nation “Minerals Security Alliance” framework

Alongside Vault, the ministerial produced a 55‑nation preferential trade and coordination framework widely referred to as a Minerals Security Alliance (MSA). Participating states reportedly include:

The Five Eyes countries (United States, Canada, United Kingdom, Australia, New Zealand).

Most EU member states, plus Japan and South Korea.

Several major resource holders in Latin America and Africa, including Brazil, South Africa, and the Democratic Republic of the Congo.

Key Indo‑Pacific partners such as India.

The framework is described as offering preferential tariff treatment for intra‑bloc trade in specified critical minerals, while establishing coordination mechanisms on export volumes, environmental and labor standards, and traceability requirements. A shared price support fund, backed in part by U.S. commitments, is intended to operate alongside Project Vault by stabilizing prices for certain minerals extracted and processed within the bloc.

Program descriptions cite the use of digital provenance tools, including blockchain‑based tracking and third‑party audits, to verify origin and compliance for shipments claiming MSA preferences. Implementation dates in the communiqués place the first wave of these requirements in the second half of 2026, with further tightening thereafter.

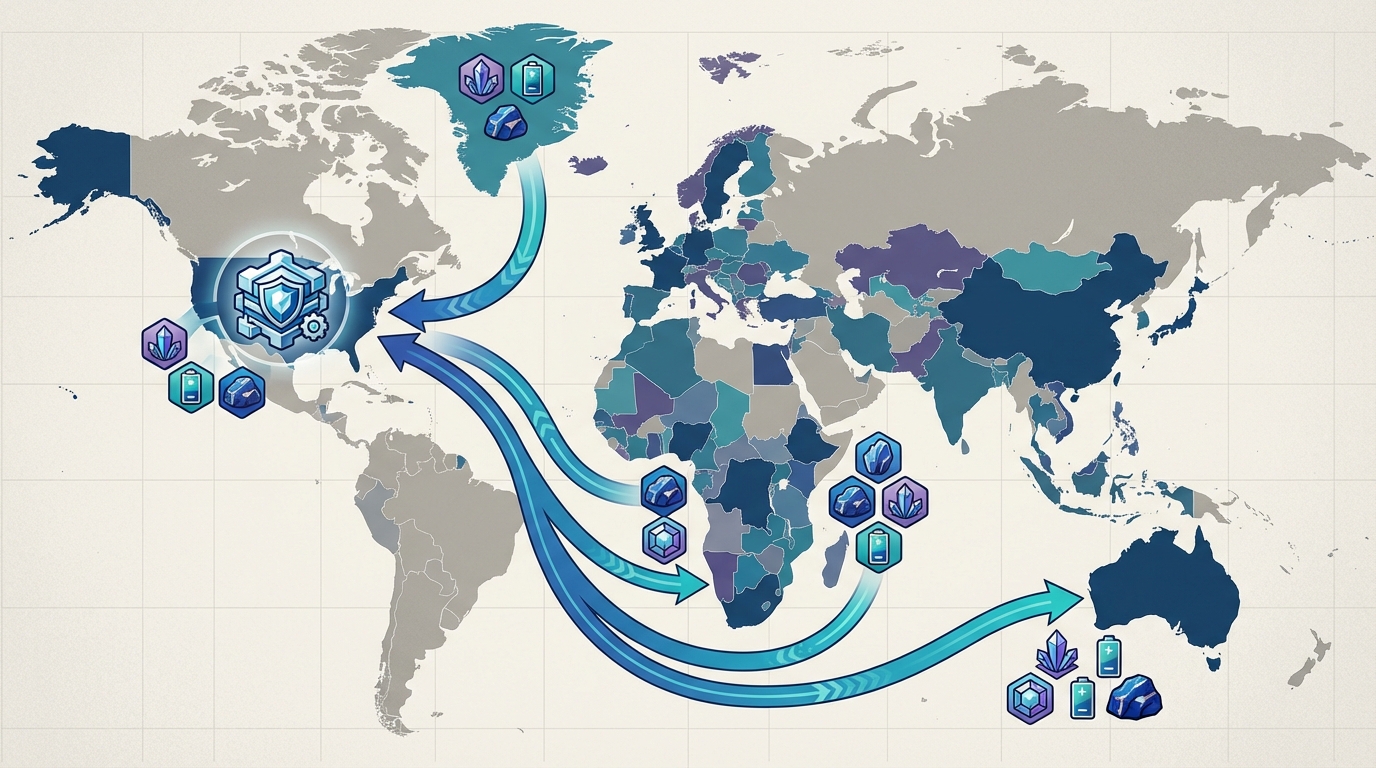

Map of the Minerals Security Alliance and international mineral flows.

3. Price support mechanisms and observable market signals

Vault and the MSA framework incorporate price support mechanisms in two distinct ways:

Direct stockpile purchasing: Vault tenders act as a buyer of last resort for allied production, creating an effective floor for certain materials when spot prices weaken.

Dedicated support fund: Within the 55‑nation framework, a pooled fund is allocated to stabilizing prices via mechanisms such as guaranteed minimums, loan guarantees, or deficiency payments on qualifying output.

Public and industry data points give some sense of the reference levels in play. Fastmarkets assessments cited in ministerial briefings put neodymium‑praseodymium (NdPr) prices at around $212.60/kg for praseodymium at the time of the meeting, reportedly up about 47% year‑to‑date. Internal modeling referenced by officials implied that Vault’s procurement and support mechanisms could be consistent with sustained levels closer to $250/kg in tight‑supply scenarios, particularly if Chinese export quotas were tightened further.

In cobalt, basis trades between London Metal Exchange contracts and Shanghai physical premiums were reported to have widened by around 15% around the time of the announcement, reflecting shifting expectations around floor prices and bloc‑aligned demand. For dysprosium, internal government planning materials referenced Vault’s role in covering a projected 2026 U.S. deficit, where anticipated demand of roughly 1,000 metric tons was expected to exceed assured supply by around 600 metric tons in the absence of dedicated stockpiling.

4. Comparison with existing U.S. and allied stockpiling programs

Historically, the U.S. National Defense Stockpile and comparable allied programs were:

Focused on a broader set of industrial and military metals, with less emphasis on rare earths and battery materials.

Run largely as unilateral, nationally scoped programs, with only loose coordination through NATO or bilateral arrangements.

Administered with limited integration into trade policy or explicit price support regimes.

By contrast, Project Vault is characterized by:

A larger nominal budget than recent NDS authorizations, concentrated on a tighter list of critical inputs.

Formal linkage to a multinational preferential trade framework, rather than standalone national stockpiling.

A design that anticipates regular market interaction via tenders and support mechanisms intended to influence both availability and pricing, not just emergency readiness.

Allied initiatives, such as Australia’s critical minerals reserve programs and the European Union’s strategic raw materials initiatives, exist alongside Vault but do not, on their own, combine the same scale of U.S. funding, explicit price interaction, and bloc‑wide trade preferences. Ministerial documentation emphasizes coordination rather than replacement of these existing efforts.

INTERPRETATION: How Project Vault May Rewire Markets and Operations

5. A deliberate shift from market‑first to state‑directed security

Materials Dispatch’s reading is that Project Vault represents a conscious decision to treat key critical minerals as strategic assets analogous to munitions or energy reserves, not just as commodities managed via private contracts. To the extent that Vault tenders proceed on the announced scale, a non‑commercial buyer enters the market with objectives that are explicitly not profit‑maximizing: resilience, national security, and allied leverage sit ahead of short‑term price efficiency.

This shift did not emerge in a vacuum. The 2010 rare earth export dispute between China and Japan, the COVID‑era shipping breakdown, and the 2023 Chinese export controls on gallium and germanium all tested the assumption that global markets would always clear efficiently. In practice, procurement teams ended up scrambling to qualify new suppliers, paying up for marginal tons, or pausing production. Vault is a policy response to that operational reality.

If Vault consistently absorbs a defined slice of non‑Chinese rare earth and cobalt output on bloc‑friendly terms, the “world price” for these materials could bifurcate: a bloc‑linked corridor with implicit or explicit floors, and a residual market for non‑aligned buyers with more volatility and potentially higher embedded geopolitical risk. From a risk‑management perspective, that is a deliberate trade‑off: less exposure to sudden shocks for bloc‑aligned demand, more fragmentation and complexity for everyone else.

6. Operational implications across the chain

For upstream mining and processing projects in aligned jurisdictions, Vault and the MSA framework function as a de‑risking overlay. If tenders and support mechanisms are executed as described, long‑cycle projects in Australia, North America, and parts of Africa gain a clearer path to sustained demand for compliant tonnage. That tends to:

Shorten decision cycles around expansions or new projects that can meet MSA environmental, labor, and provenance standards.

Elevate the importance of independent ESG audits, blockchain‑style traceability, and export licensing disciplines in project evaluation.

Make offtake linked to MSA eligibility more valuable than physically similar material lacking verified provenance, purely because of policy overlay.

For traders and midstream processors, the move cuts both ways. On one hand, predictable government tenders and price support mechanisms reduce downside risk for qualified flows. On the other, classic arbitrage between regions may narrow if a majority of non‑Chinese supply is directed into the bloc via preference regimes. Basis trades, particularly in cobalt, already reflect this: widening spreads between LME benchmarks and Chinese physical markets around the Vault announcement signal diverging risk and policy regimes rather than pure logistics or quality differentials.

Downstream manufacturers-especially magnet producers, EV makers, and defense primes-stand at the sharp end of provenance and compliance requirements. If MSA certification effectively adds ninety days to contract cycles, as some ministerial briefings have suggested, that is a non‑trivial alteration of procurement workflows. Legacy playbooks that prioritized cheapest compliant tonnage from anywhere are being displaced by multi‑criteria sourcing: origin, auditability, and alignment with bloc policy now sit alongside technical specifications and cost.

The dysprosium example is emblematic. Internal planning assumptions that Vault stockpiles will cover a projected 2026 gap between U.S. demand and secure supply effectively anchor defense planners’ expectations. To the extent Vault actually acquires that material on schedule, missile guidance systems and high‑temperature magnets feel less exposed to quota shocks or port disruptions. If acquisitions lag, the same projected gap could reappear with added complexity, as potential spot supply outside the bloc faces stricter compliance filters.

7. Can the 55‑nation framework hold under real pressure?

The most ambitious part of the ministerial outcome is not the $10 billion headline, but the assumption that 55 countries with very different geological profiles and political economies can sustain a coherent Minerals Security Alliance.

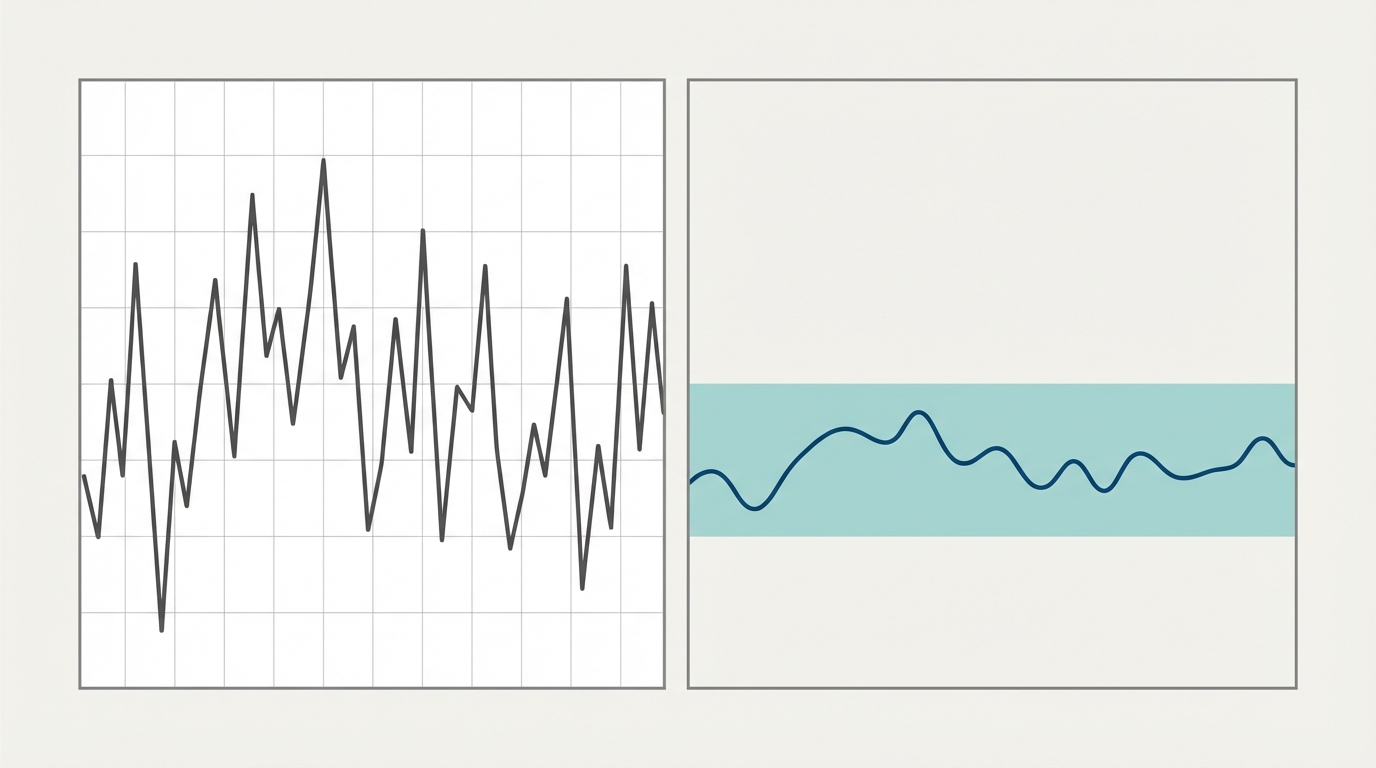

Diagrammatic comparison of market volatility vs. price-supported floor.

There are clear strengths. Concentrating a large share of non‑Chinese rare earth and cobalt reserves inside an explicit framework, with U.S. financial backing and shared standards, materially increases collective bargaining power with downstream industry. For states such as Australia or Canada, the framework validates years of work pushing critical minerals from niche topic to strategic agenda. For processing‑constrained economies like the United States, the alliance creates a structured environment to import refined material without being wholly dependent on adversarial suppliers.

However, Materials Dispatch does not see the framework as a done deal. To the extent that environmental, labor, and traceability standards are enforced rigorously, some producer states will face real domestic trade‑offs. Brazil’s niobium producers or DRC cobalt operations may find that stricter audit regimes collide with domestic political priorities. India’s desire to expand its own processing industry could create friction if alliance export coordination is perceived as constraining its autonomy.

Verification and enforcement are another pressure point. Provenance fraud has already appeared in rare earth supply chains, including documented cases where throughput from high‑profile operations did not match declared exports. Blockchain tracking and ISO‑type certifications help, but they are not a panacea. If verification lags or bad actors can launder non‑compliant material into the MSA stream, the credibility of the framework’s “trusted supply” claim erodes quickly.

Finally, there is the question of Chinese counter‑strategy. If Beijing responds with targeted quota tightening, tax incentives for allied‑country plants that continue to use Chinese‑origin intermediates, or subsidized offtake for non‑aligned producers, the bloc could face a moving target. In that scenario, Vault’s tenders and price supports would be operating not against a static benchmark, but against a rival state‑directed system with its own levers.

WHAT TO WATCH: Signals That Will Define Project Vault’s Real Impact

Vault tender cadence and fill rates: Whether REE and cobalt tenders are fully subscribed, partially filled, or repeatedly delayed will show how quickly upstream projects are aligning to bloc requirements.

Fastmarkets NdPr and dysprosium behavior vs. implied floors: Persistent divergence between observed prices (e.g., the $212.60/kg praseodymium reference) and implied Vault floor levels near $250/kg would signal either over‑ or under‑delivery of stockpiling commitments.

Share of non‑Chinese supply tied to MSA contracts: Public disclosures from producers such as Australian REE miners or North American cobalt refiners will indicate how much tonnage is effectively removed from free‑floating global trade.

Enforcement cases and provenance disputes: Early audits, shipment rejections, or fraud investigations around MSA‑certified flows will reveal how serious member states are about standards versus volume.

Chinese policy responses: Any new export quota rounds, licensing regimes, or targeted subsidies for non‑aligned projects will define whether Vault is operating in a cooperative, competitive, or confrontational ecosystem.

Evolution of allied national stockpiles: Adjustments to the U.S. NDS, EU strategic reserves, or allied national programs in light of Vault will show whether governments view Vault as additive or partially substitutive.

Conclusion

Project Vault is not a technocratic footnote; it is a deliberate decision to move critical minerals away from a loosely coordinated global spot system toward a bloc‑anchored, state‑directed architecture. The $10 billion commitment, coupled with a 55‑nation preferential framework and explicit price support mechanisms, signals that the United States and its partners are prepared to absorb real economic and diplomatic friction to secure supply.

Whether this ultimately reduces strategic vulnerability or simply fragments markets depends on execution: the credibility of tenders and floors, the cohesion of alliance members, and the nature of Chinese countermeasures. For now, the operational reality is already shifting. Procurement, compliance, and supply chain governance are being re‑written around Vault and the MSA, regardless of whether all long‑term goals are met. Materials Dispatch will continue active monitoring of regulatory and industrial weak signals around Project Vault and the Minerals Security Alliance, as these will define how much of the announced architecture translates into durable structural change.

Note on Materials Dispatch methodology Materials Dispatch assessments integrate continuous monitoring of U.S., EU, Chinese, and allied regulatory texts, communiqués, and agency rulemakings with observable market behavior where price and volume data are available. For Project Vault and the Minerals Security Alliance, this briefing cross‑references official ministerial documentation with reported tender structures and end‑use technical specifications in sectors such as permanent magnets, battery materials, and defense systems, without projecting unverified numerical forecasts.

**Ammonium perchlorate oxidizer capacity – not warhead manufacturing or guidance electronics – now sets the hard ceiling on Western missile surge production. Pentagon multiyear contracts for fourfold Tomahawk and AMRAAM output run ahead of propellant precursor reality, while Chinese export controls, Utah environmental constraints, and rail bottlenecks converge into a single chokepoint. The U.S. Department of Defense has responded with an unprecedented $1B convertible equity injection into L3Harris Missile Solutions in January 2026, tied to an H2 2026 IPO, effectively turning a propulsion supplier into a quasi-public critical infrastructure platform. This is not a generic “munitions shortfall” story; it is a specific oxidizer, process, and financing constraint that now defines the outer limit of Western missile industrial capacity.**

The Propellant Bottleneck in Western Missile Production

In Western missile manufacturing, the loudest debates have focused on launchers, seekers, and guidance electronics. The actual industrial constraint is quieter and far more chemical: solid rocket motor (SRM) propellant, and specifically ammonium perchlorate (AP), now sets the upper bound on how many Tomahawk, THAAD, PAC‑3, and Standard Missiles can be produced in any given year.

The Pentagon has explicitly identified solid rocket motor propellant production as a severe constraint on munitions surge capacity. This is not a generic “capacity” issue; it is a narrow, materials-and-process bottleneck centered on AP oxidizer output and its precursors, from sodium perchlorate and perchloric acid through to qualified composite propellant batches. When this chain stalls, SRM casings, guidance kits, and warheads queue up unused.

The institutional response is equally unusual. In January 2026, the U.S. Department of Defense (DoD) executed a $1 billion convertible equity investment into L3Harris Missile Solutions, with an IPO planned for the second half of 2026. That structure breaks with decades of reliance on traditional cost‑plus and fixed‑price contracting, effectively turning missile propulsion capacity into a form of critical infrastructure financed via a hybrid public-private balance sheet.

Materials Dispatch’s view is straightforward: AP precursor chemistry, environmental permitting, and logistics – not factory headcount or assembly tooling — are now the binding constraints on Western missile surge. The L3Harris convertible is best understood as an industrial resilience instrument aimed at that specific chokepoint, rather than as a financial innovation in search of a problem.

Ammonium Perchlorate: Chemistry, Production, and Inflexible Demand

Ammonium perchlorate (NH₄ClO₄) is the dominant oxidizer in composite solid propellants used across Western tactical and strategic missile fleets. In typical hydroxyl‑terminated polybutadiene (HTPB) formulations, AP accounts for the majority of the propellant mass. It provides the oxygen needed to burn the polymer binder and metallic fuel (often aluminum) at the pressure and temperature profile required for high‑thrust, high‑specific‑impulse SRMs.

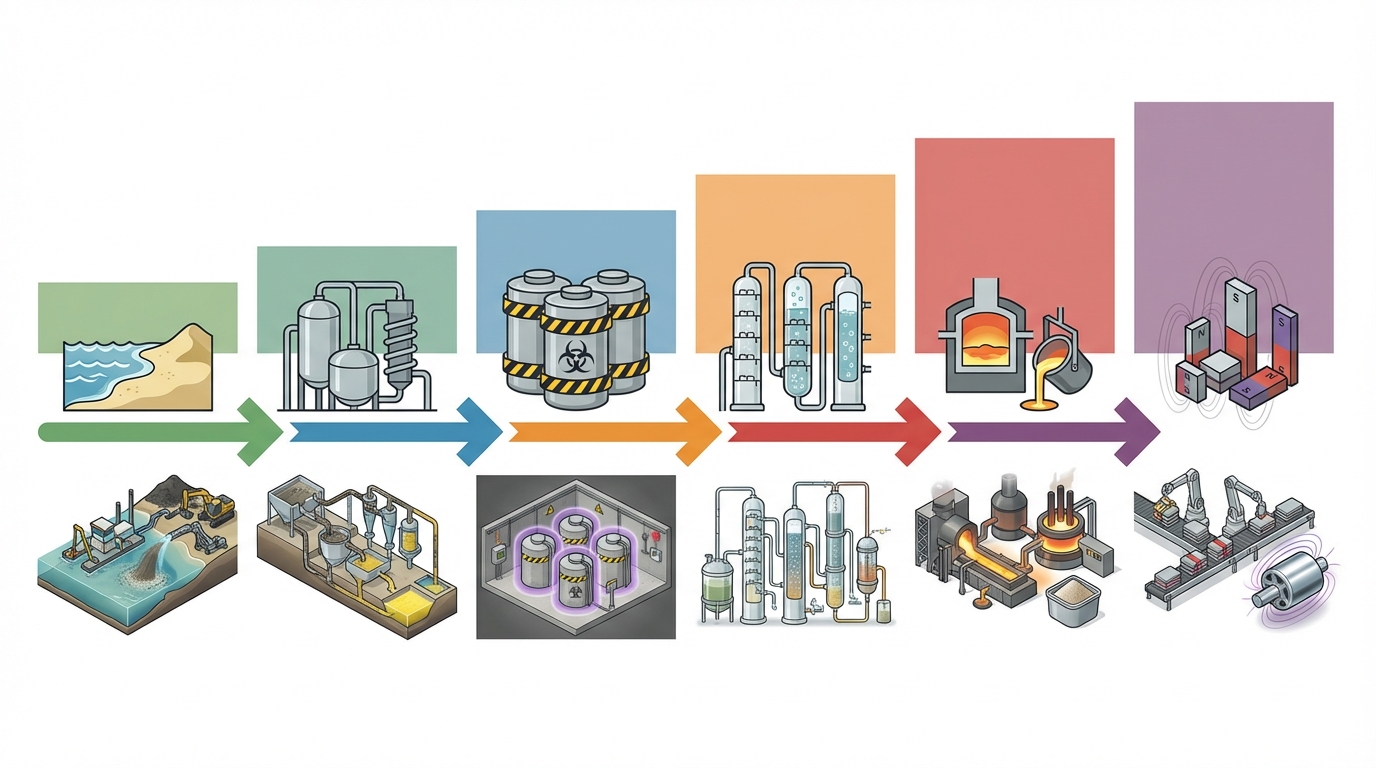

AP production follows a multi‑step chemical route:

Chlorate/chlorite production: Sodium chlorate or sodium perchlorate is produced by electrolyzing brine solutions. This is an energy‑intensive process requiring specialized cells, corrosion‑resistant materials, and stable electricity supply.

Perchloric acid synthesis: Sodium perchlorate is converted into perchloric acid (HClO₄), typically via ion‑exchange or reaction with mineral acids, under strict controls due to the strong oxidizing nature of the acid.

Ammonium perchlorate crystallization: Perchloric acid reacts with ammonia to form AP, which is then crystallized, washed, and sized to meet strict particle size distributions and purity specifications for propellant formulations.

Each stage has distinct infrastructure requirements: electrolysis cells and power access at the front; glass‑lined or specialty‑metal reactors and advanced scrubbers in the middle; and crystallizers, dryers, and milling/classification systems at the back end. These facilities are subject to hazardous chemical regulations, environmental emissions limits, and explosive safety standards, making rapid greenfield build‑out difficult.

Unlike many other inputs, AP is effectively non‑substitutable for the current generation of high‑performance tactical SRMs. Ammonium nitrate and other oxidizers can support lower‑energy propellants, but they change burn rate, temperature, and impulse to an extent that would force full missile redesign and requalification. For systems such as PAC‑3 or Standard Missile interceptors, that is not a near‑term option without accepting significant performance degradation.

This is where the bottleneck becomes structural: demand for AP is relatively inelastic at the missile‑design level, while supply expansion runs into chemistry, permitting, and capital constraints simultaneously.

Program-Level Dependence: Tomahawk, THAAD, PAC‑3, and Standard Missile

The Pentagon’s concern is not abstract. The core U.S. and allied missile families that underpin both deterrence and day‑to‑day operations are all anchored on AP‑based SRMs, typically with multiple stages and, in some cases, divert and attitude control motors that further increase oxidizer demand.

Tomahawk cruise missile: Uses solid propellant for its booster phase, bringing the missile up to speed before the turbofan cruise engine takes over. Any fourfold increase in Tomahawk output, as targeted in recent multiyear procurement plans, translates directly into a proportional increase in SRM propellant demand for boosters.

THAAD (Terminal High Altitude Area Defense): Relies on a large single‑stage solid motor to accelerate a hit‑to‑kill interceptor to very high velocities. The motor’s propellant load is substantial, meaning even modest production increases consume significant AP tonnage.

PAC‑3 (Patriot Advanced Capability‑3): Uses dual‑pulse motors and additional divert thrusters, all based on composite propellant. Multiyear procurement arrangements aiming at around four times baseline production multiply AP requirements across several motor types per interceptor.

Standard Missile family (SM‑2, SM‑3, SM‑6): Incorporates solid boosters and, in some variants, solid second stages. Navy plans for expanded ship‑based air and missile defense capacity are, in practice, AP‑demand expansion plans in disguise.

In aggregate, these families tie a large share of Western military AP consumption to a relatively small number of propellant producers and precursor facilities. When Pentagon planners talk about “4x Tomahawk and AMRAAM production” under multiyear contracts, those quantities imply AP requirements that move the entire Western oxidizer market. Production targets on paper outstrip the comfortable capacity envelope of existing AP infrastructure.

The critical point is that AP demand is driven by per‑missile propellant mass and architecture, not by easily compressible overhead. No amount of assembly‑line optimization can compensate for a shortfall in oxidizer throughput; a missing guidance unit stops one missile, but a missing AP batch can stall an entire production lot.

Where the Supply Chain Fails: Geopolitics, Regulation, Logistics

Recent data on precursor sourcing and plant operations shows that three reinforcing factors — geopolitical exposure, environmental compliance, and transport frictions — are converging on AP to create a durable bottleneck.

Geopolitical Exposure in Perchlorate Precursors

AP production depends on a steady flow of perchlorate and chlorate intermediates. Market analysis indicates that roughly 30-40% of perchloric acid precursors used by Western oxidizer producers trace back to Chinese sodium perchlorate exports. That dependency was tolerable when trade was stable; it becomes a hard risk factor once export policy is weaponized.

In 2025, China imposed export controls on perchlorate‑related chemicals that broadly mirror earlier restrictions on rare earth elements. While the affected HS codes differ, the logic is similar: prioritize domestic and aligned end‑uses, scrutinize defense‑adjacent flows, and retain policy leverage over competitors’ critical materials. For Western AP producers, this has translated into a potential shortfall on the order of 5,000-7,000 metric tonnes per year of precursors relative to planned missile surge profiles.

In a market where total Western AP demand is only in the low tens of thousands of tonnes per year, losing several thousand tonnes of precursor capacity is not a marginal inconvenience; it is a systemic constraint that ripples through every missile program tied to solid propulsion.

Environmental Regulation and Utah’s Oxidizer Hub

On the domestic side, the main U.S. AP production hub sits in Utah, a state facing increasingly stringent air‑quality oversight. Utah’s designation as a Class I ozone non‑attainment area has direct implications for high‑emissions chemical plants, including oxidizer facilities where chloride‑ and nitrogen‑bearing exhaust streams require advanced treatment.

Regulatory filings and industry disclosures indicate that Utah AP producers are planning scrubber and emissions‑control upgrades valued in excess of $150 million by the latter half of this decade. During retrofit windows, engineering schedules anticipate that approximately 20% of existing capacity will be idled. Even if upgrades ultimately enable higher throughput, the interim effect is fewer tonnes of qualified AP reaching SRM mixers at exactly the moment missile demand is surging.

AP plants are not trivial to re‑site. They require specialized safety arcs, water and power access, and transport links for hazardous materials. Environmental reviews, community acceptance, and explosive safety siting constraints turn every greenfield oxidizer project into a multi‑year effort, even before the first reactor vessel is poured.

Rail-Dependent Logistics and Vulnerable Corridors

The physical flow from AP crystallizer to missile motor is also fragile. U.S. AP production in Utah feeds propellant mixing and motor assembly plants concentrated in Arkansas, Alabama, and other Southern manufacturing hubs. That path runs overwhelmingly by rail, both for cost and for hazardous materials regulations that restrict long‑haul road movements of oxidizers at relevant volumes.

Typical lead times from Utah plants to SRM manufacturing centers run in the four‑to‑six week range for standard rail service. Those timings were manageable under peacetime procurement rhythms. Under surge conditions, they introduce a material delay between any change in oxidizer output and tangible relief at missile assembly lines.

The vulnerability of this corridor was made visible in 2025, when Union Pacific derailments in the western United States delayed approximately 2,000 metric tonnes of critical chemical cargoes, including AP and related materials. Even when no product was lost, cars awaiting rerouting or inspection extended delivery timelines and forced SRM plants to re‑sequence production around missing lots.

Because AP is both a strong oxidizer and an energetic material, re‑routing via ad hoc channels is rarely an option. Storage buffers mitigate these shocks only partially; a delay of a few thousand tonnes into a tightly scheduled SRM mixing calendar can translate into multi‑month gaps in downstream missile output.

DPA Title III: Necessary but Not Sufficient for Propellant Capacity

The U.S. government has not ignored the AP problem. Over several years, the Defense Production Act (DPA) Title III program has issued solicitations aimed at strengthening solid rocket motor and propellant capacity. These have supported plant modernizations, incremental capacity expansions, and in some cases new mixing and casting infrastructure.

that said, Title III is structurally optimized for marginal improvements and risk‑sharing on specific projects, not for rewiring an entire precursor value chain. Several recurring friction points have emerged:

Project size versus cost‑share rules: Greenfield AP or chlorate plants are capital‑intensive. Title III support typically covers only a fraction of total project cost, leaving the remainder to be financed by firms that face commodity‑like pricing and concentrated offtake risk.

Permitting timelines: Even when funding is available, environmental reviews and local permitting can run into multi‑year timeframes, particularly for projects involving perchlorates, acids, and other hazardous chemicals.

Scope bias: Many solicitations have focused on downstream capacity (propellant mixing, motor case production, casting and cure facilities), assuming precursor supply could be managed through existing channels. The 2025 Chinese export controls and Utah regulatory tightening have shown that assumption to be fragile.

Title III remains a useful tool, especially for debottlenecking specific stages or co‑funding modernization. But as AP moved from being a manageable risk to a hard constraint, the Pentagon was left with a gap: traditional grants and cost‑share mechanisms have struggled to mobilize the scale and speed of capital required for new precursor and oxidizer capacity.

The Pentagon–L3Harris $1B Convertible: Structure and Industrial Logic

Against this backdrop, the January 2026 $1 billion convertible equity investment into L3Harris Missile Solutions represents an explicit attempt to break out of the Title III cage. Instead of adding another layer of project‑by‑project cost‑sharing, the DoD has taken a direct capital stake in a propulsion‑centric business unit, with a clear path to an initial public offering planned for the second half of 2026.

Public disclosures indicate that the instrument is structured as a convertible equity stake rather than a classic grant or loan. In practice, that means the DoD provides upfront capital in exchange for securities that convert into common equity under defined conditions, such as the planned IPO. The structure aligns several industrial‑base objectives:

Speed of capital deployment: Unlike procurement contracts, which release cash against delivered units or milestones, and unlike Title III awards, which often require extensive cost justifications, a large convertible equity infusion can move onto a company’s balance sheet rapidly and be deployed into capex according to an integrated industrial plan.

Risk distribution: Facility construction risk, cost overruns, and market risk are borne primarily by the corporate entity and future shareholders, not solely by the DoD. At the same time, the DoD retains leverage through its position as a major customer and convertible holder.

Signal to private capital: A government equity stake tied to a missile‑propulsion pure‑play slated for IPO signals that AP and SRM capacity are treated as critical operational infrastructure. That signal is designed to crowd in additional private capital alongside the government’s anchor position.

Governance access: Equity, even if structured with limited voting rights, provides more direct visibility into project pipelines, timelines, and risk than arm’s‑length contracts. That matters when AP precursor plants and motor lines become strategic assets in their own right.

From an industrial resilience perspective, the move effectively reclassifies a portion of the solid propulsion base as a quasi‑public utility. Instead of relying solely on annual appropriations and contract vehicles, the DoD now sits on the cap table of a key SRM actor, with the explicit intent of accelerating oxidizer and motor capacity build‑out ahead of confirmed unit demand.

It is also notable that the security is convertible, not perpetual common equity. That design allows eventual dilution and exit once the IPO market has absorbed the risk and once AP/SRM capacity has reached targeted levels, preserving flexibility for future policy shifts.

Execution Constraints: From Equity Infusion to Qualified Propellant

Injecting $1 billion in January 2026 does not immediately translate into more Tomahawk boosters in 2027. The solid propulsion value chain imposes real timelines between capital, concrete, and qualified propellant.

Site selection and permitting: Any new AP or precursor facility driven by the L3Harris Missile Solutions capital will still navigate local zoning, environmental impact assessments, and explosive safety siting. Even with political support, these processes introduce unavoidable lags.

Equipment lead times: Electrolysis cells, acid handling systems, crystallizers, and high‑energy milling equipment are specialized and often built to order. Lead times for some critical items can extend well beyond a year, especially when multiple projects compete for the same vendor capacity.

Process qualification: Propellant‑grade AP is not a generic commodity. Any new line or plant has to demonstrate consistent purity, particle size distribution, and thermal stability. That entails extended production trials and testing campaigns with SRM integrators before full‑rate supply.

Downstream integration: Additional AP volume only translates into missile throughput if propellant mixers, motor casting facilities, and test stands expand in parallel. DPA Title III solicitations have already targeted some of these stages, but they remain coupled to precursor availability.

This is where the IPO timeline becomes relevant. With an H2 2026 listing planned, L3Harris Missile Solutions is effectively using the DoD’s convertible as bridge capital to fund early design, permitting, and long‑lead equipment commitments, while expecting public‑market proceeds and follow‑on debt to finance later construction phases and downstream integration.

The critical execution risk is sequencing. If precursor plant projects slip due to permitting or equipment delays, while downstream mixing and motor lines come online on time, the system simply shifts the bottleneck further upstream. Conversely, if AP capacity is ready but shipping and storage constraints lag, oxidizer can accumulate at origin without reducing lead times into SRM plants.

Scenarios 2026–2030: Surge, Shortfall, and Stockpile Tradeoffs

Considering AP precursor risks, DPA initiatives, and the L3Harris convertible, three broad industrial scenarios frame the 2026–2030 window.

1. Managed Surge: Incremental Debottlenecking and Staggered Capacity

In a managed surge scenario, existing AP facilities in Utah complete environmental upgrades broadly on schedule, with only the anticipated 20% temporary capacity idling. Alternative precursor sources partly backfill the loss of Chinese sodium perchlorate, keeping the net shortfall closer to the lower end of the 5,000–7,000 tonne band.

The L3Harris Missile Solutions capital programme brings incremental new AP and mixing capacity online toward the end of the decade, while DPA Title III projects deepen redundancy in SRM mixing and casting. Under this trajectory, fourfold missile production targets for Tomahawk and AMRAAM are not fully met, but output steps up substantially relative to the pre‑2022 baseline, with most delay attributable to qualification and logistics rather than absolute chemical scarcity.

2. Hard Constraint: Regulatory Slippage and Precursor Shock

A harder‑constraint scenario emerges if environmental permitting for expansions stretches out, local opposition slows new oxidizer projects, or if Chinese export controls tighten further or are mirrored by other precursor‑producing states. Under that pattern, the upper end of the 5,000–7,000 tonne precursor shortfall materializes or is even exceeded.

In this case, the L3Harris convertible still underwrites critical new infrastructure, but the practical impact shifts into the 2029–2030 window. Missile programmes face binding AP rationing, with program offices trading production slots between fleets. Stockpiles of already‑cast motors become a key tool for buffering shocks, but replenishment cycles lengthen.

From a technical standpoint, propellant formulators may be forced to explore higher‑risk substitutions or process adjustments to stretch available AP, but any such moves carry qualification and reliability implications that weapon‑system integrators treat with justified caution.

3. Overbuild and Latent Capacity: Equity Pulls Forward the Curve

A more optimistic scenario sees the $1 billion convertible acting as a catalyst that overbuilds oxidizer capacity relative to immediate procurement plans. If permitting proceeds smoothly and IPO markets accept L3Harris Missile Solutions at favorable terms, the company and its ecosystem could end the decade with substantial latent AP and SRM capacity.

In that world, the structural bottleneck might migrate away from oxidizer to other inputs — for example, specific alloys for motor cases or nozzle components, or highly specialized test and inspection equipment. But even in that case, the AP constraint will not have vanished; it will have been displaced by concerted industrial policy and financing, not by organic market dynamics.

Historical Echoes: From Shuttle Boosters to Today’s Industrial Base

The present AP bottleneck has historical analogues. During the Space Shuttle era, solid rocket boosters relied on large composite propellant segments that concentrated oxidizer demand in very few facilities. Accidents, quality‑control issues, and local regulatory pressures highlighted how vulnerable a launch system could be to a single propellant line or plant.

There is also a broader echo in other critical materials episodes, such as earlier depletion scares in hydrazine propellants or the post‑Cold War contraction of nitrate‑based explosives capacity. In each case, military programmes assumed the continued availability of legacy chemical infrastructures long after commercial markets had moved on or consolidated.

What distinguishes the current AP situation is the combination of three factors rarely seen together:

Geopolitical contestation over upstream precursors, including export controls shaped explicitly with defense end‑uses in mind.

Domestic environmental tightening in precisely the regions where legacy oxidizer plants are located, forcing costly retrofits and threatening local social licence.

Financial innovation in the form of direct government convertible equity, taking the industrial base partly outside the traditional procurement and grant toolkit.

This combination makes the AP case a template for how other defense‑critical chemicals and materials may play out in coming years: a small number of chokepoints, magnified by geopolitics and regulation, addressed via hybrid public–private capital structures rather than purely contractual remedies.

Synthesis: What Really Constrains the Next Missile Surge

For defense industry analysts, propulsion engineers, and munitions‑supply specialists, the core insight is that the limiting factor in Western missile surge capacity is no longer assembly‑line footprint or even warhead manufacturing. It is the ability to source, process, and deliver consistent, qualified batches of ammonium perchlorate and its precursors under tightening regulatory and geopolitical conditions.

Tomahawk, THAAD, PAC‑3, and Standard Missile programmes are all effectively indexed to AP throughput. Multiyear procurement contracts targeting fourfold production increases represent an intention; AP and precursor capacity determine how much of that intention can translate into fielded hardware, and on what timeline.

DPA Title III solicitations have played an important role in sustaining this ecosystem, but their design is inherently incremental. The Pentagon’s $1 billion convertible equity stake in L3Harris Missile Solutions, with an H2 2026 IPO in view, signals recognition that the oxidizer bottleneck is a structural industrial‑base issue requiring a different toolset.

From Materials Dispatch’s perspective, three trade‑offs define the space over the next decade:

Speed versus governance: Direct equity accelerates capital deployment but draws the DoD closer to corporate decision‑making and market volatility.

Redundancy versus cost: Building surplus AP and SRM capacity enhances resilience but risks under‑utilization in peacetime and political scrutiny over “excess” capability.

Environmental compliance versus concentration: Upgrading and expanding legacy plants in regulated jurisdictions trades single‑site risk against the complexity of siting new facilities elsewhere.

The outcome will depend less on abstract budget levels and more on the execution of specific chemical plants, rail corridors, and qualification programmes. Materials Dispatch is actively monitoring weak signals across these domains — from precursor export‑control notices and Utah air‑quality rulemakings to Title III solicitation language and L3Harris Missile Solutions’ pre‑IPO disclosures — because those are the levers that will ultimately determine how many missiles Western arsenals can credibly field under surge conditions.

Note on Materials Dispatch methodology Materials Dispatch combines close reading of official industrial‑base reports, export‑control filings, and DPA Title III documentation with tracking of corporate disclosures from firms such as L3Harris, as well as technical specifications for missile propulsion systems. This triangulation between policy texts, market data, and end‑use engineering requirements underpins the assessment of where bottlenecks are truly emerging in AP and solid rocket motor supply chains.

India sits on some of the world’s most substantial rare earth reserves and yet contributes only a sliver of global production. For Materials Dispatch, this gap is not an academic curiosity; it is a concrete supply-chain risk. Over the past decade, every serious rare earth disruption-Chinese export curbs, Myanmar instability, opaque licensing changes-has translated into hard procurement problems for downstream users in magnets, motors, catalysts, and defense systems. Internal sourcing cycles have repeatedly run into the same roadblock: India appears on paper as a “sleeping giant” in rare earth geology, but on the ground it behaves like a marginal supplier.

The 2025-2026 policy pivot in India, centered on monazite-based value chains and new manufacturing schemes, is the first credible attempt to close that gap. It deserves close, critical scrutiny because it has the potential to change sourcing options for magnets and refined oxides, while also introducing new regulatory and operational complexities around nuclear-linked minerals, coastal mining, and state-backed monopolies.

Change: India is moving from raw monazite extraction towards an integrated rare earth value chain, anchored by a new permanent magnet manufacturing scheme and planned rare earth corridors.

Scope: The focus is on monazite-based reserves, downstream processing, and rare earth permanent magnets, under a regime still dominated by state-owned IREL and atomic energy regulators.

What is covered: Geological endowment, institutional/regulatory framework, and headline policy measures (scheme outlays, capacity targets, corridor concepts).

What is not covered: Precise project-by-project economics, detailed pricing outcomes, and definitive timelines for all corridor elements, which remain either unpublished or fluid.

Operational angle: To the extent that these measures are executed, they could partially diversify supply away from China’s refining dominance, but only after navigating thorium regulations, community resistance to beach mining, and the constraints of a de facto monopoly.

FACTS: Resource Base, Institutional Setting, and New Policies

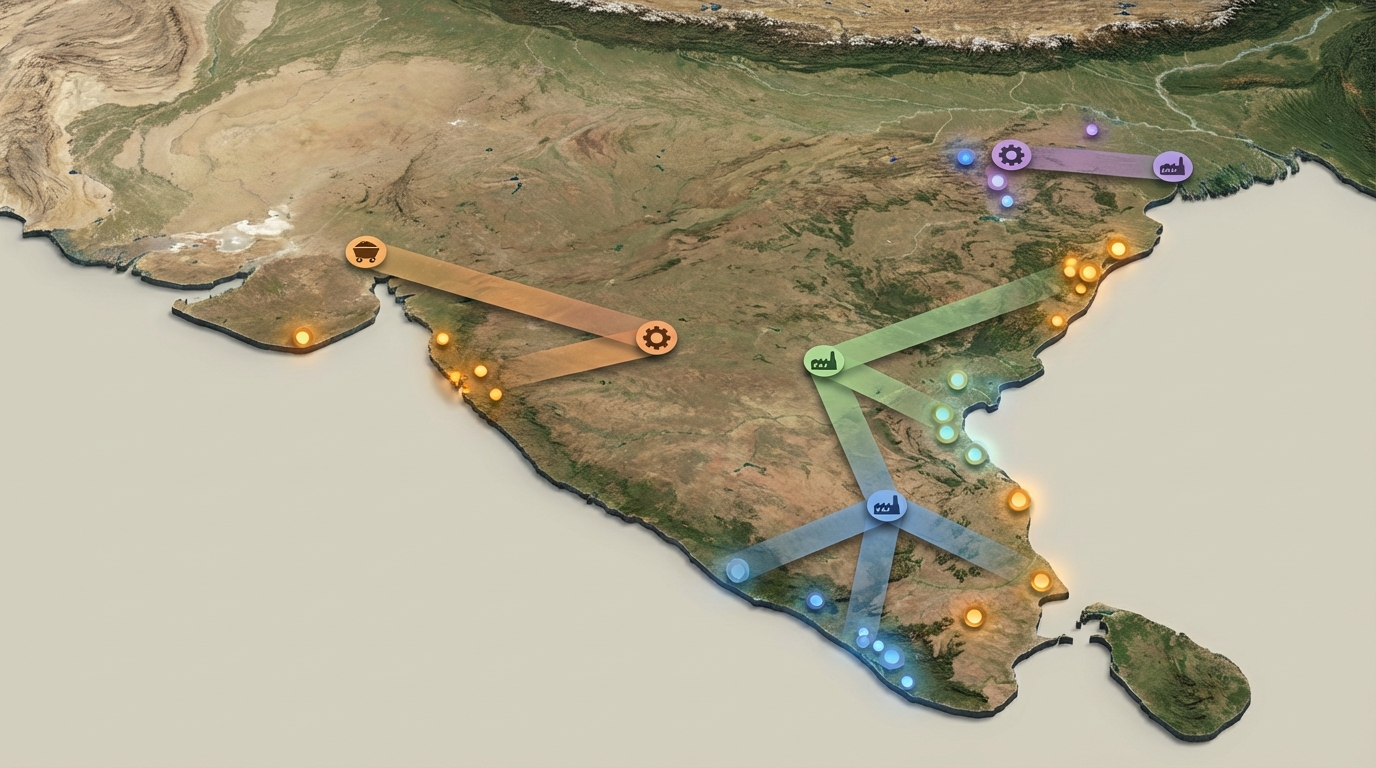

India’s rare earth reserves and monazite dominance

According to public geological reporting and international comparisons, India holds the world’s third-largest rare earth oxide (REO) reserves at around 6.9 million tonnes. Annual rare earth production, however, has been estimated at only about 2,900 tonnes in 2024, which corresponds to less than 1% of global output. The contrast between reserves and production is the core structural fact behind the “sleeping giant” label widely applied to India in this sector.

Unlike many other producing regions where bastnäsite or hard-rock deposits dominate, India’s rare earth endowment is heavily concentrated in monazite-bearing beach and inland placer sands along the coasts of states such as Andhra Pradesh, Kerala, Odisha, and Tamil Nadu, with additional occurrences in Gujarat, Maharashtra, Jharkhand, and West Bengal. Monazite typically contains both light rare earth elements and thorium, which brings the sector under India’s atomic energy and radiation safety framework.