Materials Dispatch cares about this topic for a simple operational reason: in every missile-defense sourcing cycle examined over the last decade, the technical bill of materials led back to the same bottleneck – Chinese rare earth processing and magnet capacity. Export-control scares, supplier failures, and the scramble to qualify even small non-Chinese magnet volumes have turned that bottleneck from an abstract geopolitical trope into a daily procurement constraint. The current Israel-Iran missile dynamic exposes that constraint brutally: the same country underpins the magnets inside the Arrow interceptor defending Tel Aviv and the navigation architecture inside the Fattah-series missiles flying toward it, while also positioning itself as a diplomatic broker. That is not a paradox; it is supply chain design.

- The underlying change is not a single law but the convergence of China’s roughly 90% control of rare earth processing, documented interceptor depletion in Israel, and slow-moving Western diversification efforts.

- Covered scope includes neodymium and samarium-cobalt magnet dependence in Arrow, THAAD, Patriot and David’s Sling; BeiDou-3 use in Iranian missiles; and Chinese leverage via oil trade and rare earth chokepoints.

- Operations are constrained by long magnet lead times, qualification cycles, and the reality that the US remains 100% net import dependent on finished rare earth magnets while EU and Japan only begin to scale alternatives.

- Interpretation remains bounded by public data; quantified 2026 shortage and price scenarios derive from published modeling, not from Materials Dispatch forecasts.

- The central asymmetry: China can influence both Israeli interceptor resupply and Iranian missile performance through materials and navigation supply chains in a way no other actor currently can.

FACTS: The Supply Chain Architecture Behind Sword, Shield, and Diplomacy

China’s Dominance in Rare Earth Processing and Finished Magnets

Open-source assessments converge on a central fact: China processes around 90% of the world’s rare earth oxides into usable materials and components. This includes the conversion of mined concentrates into separated oxides, metals, and high-performance magnets. The Australian Strategic Policy Institute (ASPI), in its work on strategic dependencies, has described US missile defense in particular as critically exposed to Chinese-controlled rare earth and magnet supply chains.

Rare earth permanent magnets – primarily neodymium–iron–boron (NdFeB) and samarium–cobalt (SmCo) – are mission-critical in modern missile defense systems. They appear in:

- Actuators for aerodynamic control surfaces and thrust-vectoring in interceptors such as Arrow and Patriot.

- Gimbal motors and guidance assemblies in seekers and radar systems used by THAAD and David’s Sling.

- Electric drive systems inside radar arrays and fire-control systems supporting these batteries.

The United States is assessed by government and academic sources as being 100% net import dependent on finished rare earth magnets. The bulk of those finished magnets, even when sourced via intermediaries, originate from Chinese processing and manufacturing capacity.

ASPI’s analysis of US missile defense identifies Chinese-controlled rare earth supply and magnet manufacturing as chokepoints for critical systems, including Patriot and THAAD, where magnet substitution or redesign is either technically constrained or would take years to validate for combat use.

Interceptor Depletion: RUSI Data on Arrow and David’s Sling

The Royal United Services Institute (RUSI) has documented the pace at which Israel’s missile-defense interceptors have been consumed under sustained attack. One assessment reports approximately 122 of 150 Arrow-2/3 interceptors used, and 135 of 250 David’s Sling interceptors expended, in recent barrages. That translates into a significant drawdown of stockpiles for systems that depend heavily on rare earth magnet content throughout their guidance and actuation subsystems.

RUSI’s depletion figures do not themselves quantify magnet consumption. that said, given that each interceptor embodies multiple NdFeB and, in some high-temperature locations, SmCo components, these depletion rates map directly into magnet replacement requirements. Replacement is constrained not only by financial appropriations and assembly capacity, but by the availability of qualified magnet supply – overwhelmingly tied back to Chinese processing.

Iranian Missiles and BeiDou-3 Military-Grade Navigation

On the offensive side of the current regional dynamic, Iranian ballistic and cruise missiles – including advanced designs such as the Fattah family – have reportedly integrated China’s BeiDou-3 satellite navigation system. Open-source technical analyses describe the use of BeiDou-3 military-encrypted signals, which enhance accuracy and resilience relative to unencrypted civilian navigation feeds.

These missiles also rely on components and materials that run through Chinese supply lines more broadly, including electronics, machine tools, and precursors relevant to propellant and structural materials. While not all of these rely on rare earths, the navigation and guidance stack is directly tied into Chinese space-based infrastructure and related component ecosystems.

China is also reported to purchase roughly 80% of Iran’s oil exports, largely through channels that circumvent formal Western sanctions frameworks. That oil revenue underpins Tehran’s fiscal capacity for missile development and procurement. The same bilateral trade relationship that moves oil also provides a foundation for technology, component, and materials flows relevant to Iran’s missile programs.

Western Vulnerability: ASPI and West Point Modern War Institute Assessments

ASPI’s report on strategic rare earth dependence in US missile defense highlights two linked facts:

- Chinese entities dominate the separation and processing stages for the specific rare earth elements required in high-coercivity NdFeB and SmCo magnets used in missile guidance and actuation.

- US missile defense programs rely on these magnets with limited substitute materials or designs qualified to the same performance and reliability standards.

The Modern War Institute at West Point has framed China’s rare earth monopoly as a national security risk, warning that a disruption in Chinese rare earth or magnet exports could significantly degrade the US defense industrial base’s ability to sustain missile-defense sortie rates. The institute’s assessment emphasizes the time required – measured in years, not months – to stand up non-Chinese alternatives at every stage from oxide separation to finished magnet production and system-level qualification.

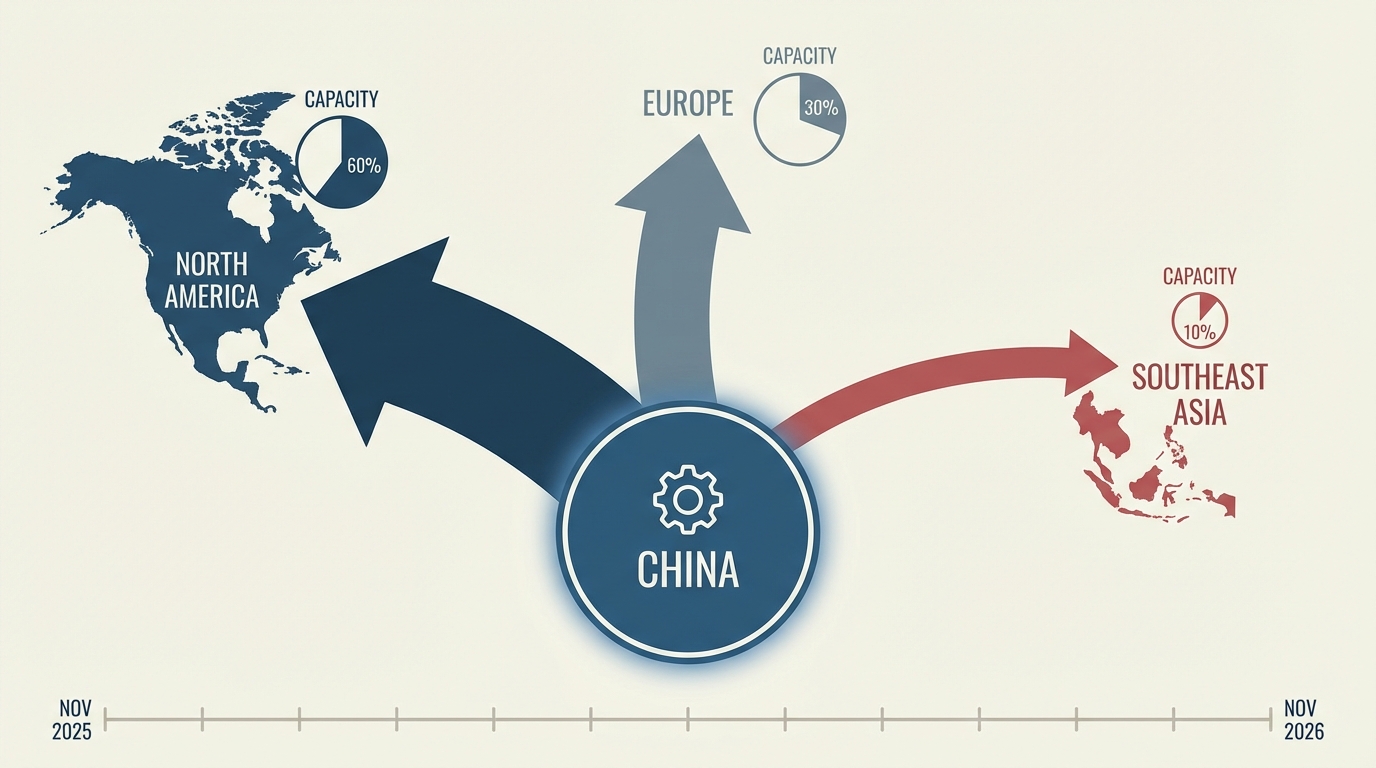

Regulatory and Strategic Responses: EU CRMA, Japan’s Stockpile, and 2026 Horizon Scenarios

Several jurisdictions have begun codifying responses to this structural dependence, with direct implications for defense supply chains:

- European Union – Critical Raw Materials Act (CRMA): By the second quarter of 2025, the CRMA’s Phase 2 benchmarks include a target for 10% of certain critical raw materials, including rare earths, to be processed domestically within the EU. For defense contractors, non-compliance can trigger fines reportedly in excess of €10 million, creating a formal regulatory incentive to diversify away from Chinese processing.

- Japan – Rare Earth Strategic Stockpile: By the fourth quarter of 2025, Japan’s rare earth strategy envisages doubling its strategic stockpile of NdFeB magnets to around 5,000 metric tonnes. This is particularly relevant given Japanese partnerships in missile-defense programs and co-production, where Japanese magnet capacity can act as a partial hedge against Chinese disruption.

- 2026 Horizon – Chinese Quota Scenarios: Bloomberg Intelligence has modeled potential Chinese quota tightening that could displace on the order of 13,000 metric tonnes of rare earth supply from global markets by 2026. In that scenario, Western buyers face modeled aggregate premiums of USD 2–3 billion, with dysprosium prices reaching around USD 1,200 per kilogram. These are scenario analyses, not certainties, but they illustrate the magnitude of financial and supply stress modeled under tighter export quotas.

These moves coexist with national-level programs in the US and elsewhere to seed domestic mining, separation, and magnet manufacturing, often through defense-focused industrial policy. However, the provided data do not specify exact volume or timing beyond the broad 2025–2026 horizons and the Japanese stockpile target.

China as Diplomatic Host and Supply Chain Gatekeeper

Parallel to its role as a materials and navigation supplier to both Israeli-aligned and Iranian-aligned systems, Beijing has positioned itself as a host for diplomatic initiatives and potential peace talks related to the conflict. This juxtaposition – Chinese-origin magnets inside interceptors defending Tel Aviv, Chinese navigation and trade flows enabling missiles targeting Israeli cities, and Chinese diplomats convening discussions – is grounded in the same structural fact: control over a set of industrial chokepoints that neither side can rapidly replace.

INTERPRETATION: How Structural Dependencies Translate into Leverage

From Monopoly to Leverage: The Asymmetry Embedded in Rare Earth Processing

To the extent that China maintains roughly 90% of rare earth processing and dominates finished magnet production, it holds a structural lever over both the pace and sustainability of missile-defense resupply in Israel, the US, and allied states. ASPI and West Point’s Modern War Institute are aligned on one core point: Western missile-defense architectures were built under an implicit assumption that cheap, reliable Chinese magnet supply would persist indefinitely. That assumption has already been challenged by Chinese export controls on other strategic materials such as gallium and germanium; magnets and rare earths sit one policy step away from similar treatment.

If Beijing were to tighten export licensing on specific magnet grades, prioritize domestic civil-industrial demand, or simply allow longer administrative delays for exports, interceptor production lead times in allied states would stretch. RUSI’s depletion figures show that Arrow and David’s Sling stocks can be drawn down quickly under sustained attack. In a scenario where interceptors are expended faster than they can be replaced and critical magnet components face longer or uncertain delivery, system-level readiness could erode even if funding and assembly capacity exist on paper.

The asymmetry is clear: even modest changes in Chinese export posture can ripple through Western defense industrial bases far more quickly than Western diversification efforts can come online. The multi-year timelines associated with new rare earth separation plants, alloying lines, and magnet factories put Western systems on the back foot in any short-notice crisis.

The “Sword and Shield” Feedback Loop: Iranian Missiles vs. Israeli Interceptors

The same industrial ecosystem that supports Western interceptors also underpins key capabilities on the Iranian side, albeit in different ways. BeiDou-3 integration into Iranian missiles ties guidance performance directly into Chinese space infrastructure and chipset ecosystems. Chinese demand for Iranian oil, reportedly around 80% of Tehran’s exports, provides fiscal oxygen for missile development programs. And Chinese-origin components and manufacturing know-how appear repeatedly in open-source missile forensics and supply chain mappings.

That said, there is an important structural difference. Iranian systems can tolerate cruder performance in some cases: larger circular error probable, more reliance on volume of fire rather than exquisite precision, and more flexible use of mid-tier electronics. Israeli and US missile-defense systems, by contrast, are engineered around high-precision intercepts that demand top-end guidance and control hardware. This makes magnet performance less fungible on the defensive side than on the offensive side.

If Chinese rare earth and magnet exports to Western-aligned defense industries were curtailed, Israeli interceptor production could face near-term constraints that would not automatically translate into equivalent constraints on Iranian missile output. Oil revenues can be redeployed into alternative components; guidance performance can be traded for volume; and lower-tech solutions can be fielded. The shield is more technologically brittle than the sword, and that brittleness runs straight through the magnet supply chain.

Regulation vs. Reality: Can EU, US, and Japan Close the Gap in Time?

On paper, measures like the EU CRMA’s 10% processing benchmark and Japan’s 5,000-tonne NdFeB stockpile are rational responses. They recognize that defense readiness is inseparable from critical materials security. However, these targets also underscore how small current non-Chinese capacities remain relative to global demand and to the concentration of processing in China.

If Bloomberg Intelligence’s 2026 quota scenario materializes – displacing roughly 13,000 tonnes of rare earth supply and driving modeled Western premiums and dysprosium price spikes – magnet availability for defense programs could become an explicit allocation problem rather than a background procurement concern. At that point, even well-intentioned regulatory benchmarks would be chasing a moving target: as China tightens supply or raises its own downstream consumption, the baseline against which “10% domestic processing” is measured may itself shrink in export-available terms.

In practice, Western defense primes and ministries have already begun multi-sourcing and pre-qualification of non-Chinese magnet suppliers. Yet, based on program-level audits Materials Dispatch has observed, qualification cycles often run several years, especially for high-reliability missile components. Even under optimistic scenarios, these efforts are unlikely to fully offset a determined Chinese tightening by 2026. The risk is a transitional window where stocks of interceptors – already partially depleted, as RUSI’s data shows – need fast replenishment, while the magnet supply base is still only partially diversified.

Diplomatic Hosting as an Extension of Industrial Power

Beijing’s role as a host for talks touching on Israel–Iran tensions is often framed purely in traditional diplomatic terms. From a materials and industrial perspective, it also reflects the reality that China sits at the junction of both parties’ critical supply chains. That positioning alters the geometry of any negotiation, even if it is never stated explicitly.

If Chinese policymakers perceive value in de-escalation, they have structural options – ranging from quiet tightening of certain export channels to technical “maintenance windows” in satellite navigation services – that could, in principle, alter the material conditions of the conflict. Conversely, neutral or permissive export behavior can allow both missile offense and missile defense to continue drawing on Chinese-enabled capabilities. The key point is not speculation about intent but recognition of capacity: no other state currently has comparable leverage over both sides’ material warfighting architectures at once.

This leverage does not automatically translate into overt coercion. It does, however, give Beijing a background influence over timelines: how fast interceptors can be replaced, how quickly certain missile capabilities can be iterated, and how credible long-war planning looks to capitals that remain magnet-dependent. In Materials Dispatch’s view, that quiet, structural power is underappreciated in mainstream assessments of the conflict.

WHAT TO WATCH: Signals of Shifting Leverage

- Chinese export licensing for rare earth magnets: Any move to add specific NdFeB or SmCo grades to tighter dual-use control lists, extend processing times, or introduce end-use certification requirements directly affecting defense contractors.

- MOFCOM quota announcements and commentary: Changes in annual or quarterly rare earth export quotas, especially language prioritizing domestic clean-tech or industrial upgrading over exports, which would squeeze available volumes for defense end-uses.

- Implementation details of EU CRMA enforcement: Actual enforcement actions or fines against defense suppliers over critical raw materials sourcing, which would signal how seriously Brussels intends to push non-Chinese processing for strategic programs.

- Japan’s strategic stockpile drawdowns: Evidence that Tokyo is tapping NdFeB stockpiles for defense co-production, particularly in missile or radar programs, would indicate that stress in global magnet markets is filtering into operational planning.

- US magnet manufacturing milestones: Commissioning of full-value-chain facilities (from separated oxides to finished magnets) and, crucially, their qualification into specific missile-defense programs, not just commercial EV or wind applications.

- BeiDou-3 service posture and chip export patterns: Any change in availability, signal characteristics, or export rules for high-grade BeiDou navigation modules to Middle Eastern buyers, particularly those linked to Iranian missile programs.

- China–Iran oil trade volumes and terms: Sustained or rising Chinese intake of Iranian oil, especially under sanctions pressure, which continues to underpin missile development budgets and trade-based access to dual-use goods.

- RUSI and similar analyses on interceptor stockpiles: Updated figures on Arrow, David’s Sling, Patriot, and THAAD inventories and usage rates under attack scenarios, as a real-time proxy for magnet-demand stress.

- Public or leaked references to magnet shortages in defense contracting: Contract delays, program re-baselining, or formal notices citing rare earth or magnet availability as a schedule driver.

- Beijing’s public framing of its mediation role: Shifts in Chinese official rhetoric that link peace initiatives with “stability in global supply chains”, which would indicate an explicit awareness of leverage at the intersection of materials and security.

Conclusion

The current missile confrontation around Israel reveals more than tactical interplay between interceptors and incoming missiles; it exposes the degree to which both offense and defense are wired into the same Chinese-centered materials and navigation infrastructure. Rare earth magnets and BeiDou-3 chips are not abstract strategic assets – they are the quiet components that determine how many salvos can be fired, how accurately, and for how long.

Regulatory moves in the EU, stockpiling in Japan, and nascent US magnet initiatives acknowledge the risk but do not erase the near- to medium-term asymmetry. As long as the United States remains fully import dependent on finished rare earth magnets and China dominates processing, Beijing holds structural leverage over the tempo and sustainability of Western missile-defense operations. For Materials Dispatch, active monitoring of regulatory and industrial weak signals around these chokepoints remains central to understanding how the next phase of this conflict – and any negotiated outcome – will be materially constrained.

Note on Materials Dispatch methodology Materials Dispatch builds its briefings by cross-referencing primary texts from relevant authorities and administrations with open-source defense analyses and specialist research on rare earth supply chains. These regulatory and technical readings are then mapped against observed market behavior and end-use specifications in systems such as missile interceptors and satellite-navigation-guided munitions, to link legal frameworks and industrial capabilities with concrete operational constraints.