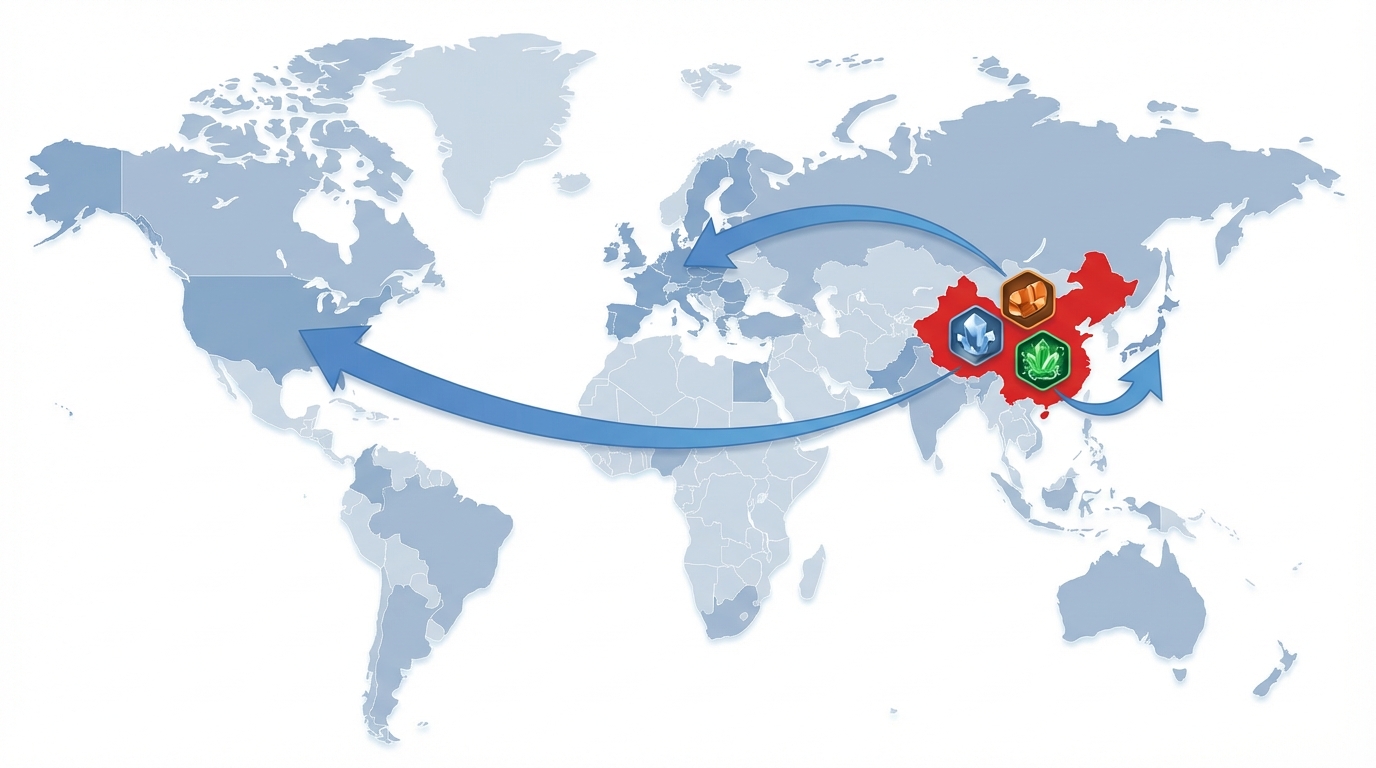

China commands roughly 98–99% of primary low-purity gallium production, creating a “by-product trap” for global supply response.

Since July 2023, Beijing has sequenced licensing, embargoes, technology controls and tactical suspensions to toggle gallium exports on short notice.

Allied initiatives to develop alternative recovery capacity face economic and technological hurdles absent long-term offtake assurances.

Procurement, supply-chain and compliance teams must map indirect gallium exposure and plan for rapid policy reversals.

Executive Summary

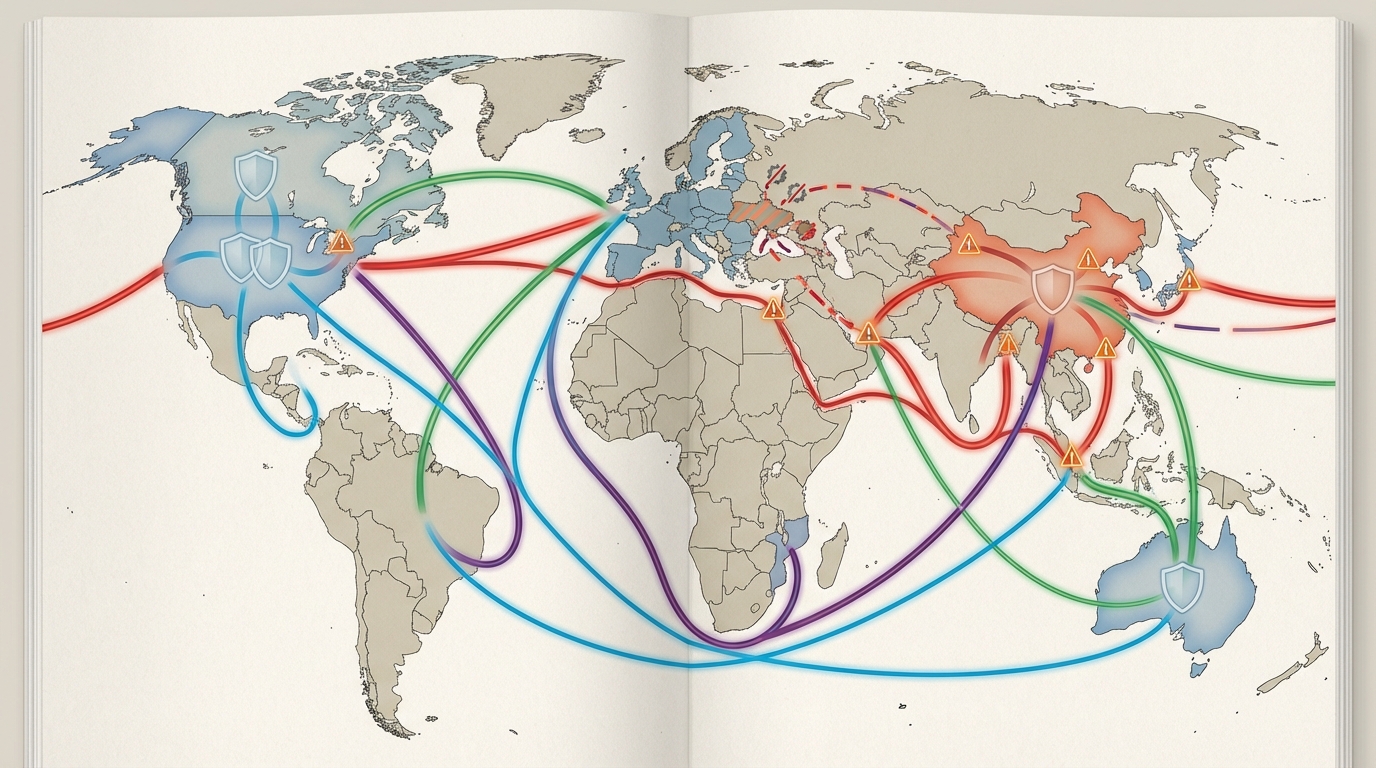

China’s calibrated export and technology controls on gallium since mid-2023 reveal a deliberate playbook for exerting leverage over Western semiconductor, defense and clean-tech supply chains. Gallium is not scarce geologically—it is a minor by-product of bauxite and zinc refining—but China’s 98–99% share of primary low-purity gallium production and its proprietary extraction technologies empower Beijing to impose sudden restrictions. Even after the November 2025 suspension of the U.S. civilian export ban (extended through late 2026), the regulatory and technology choke points remain in place, posing persistent disruption risks for procurement and strategy teams.

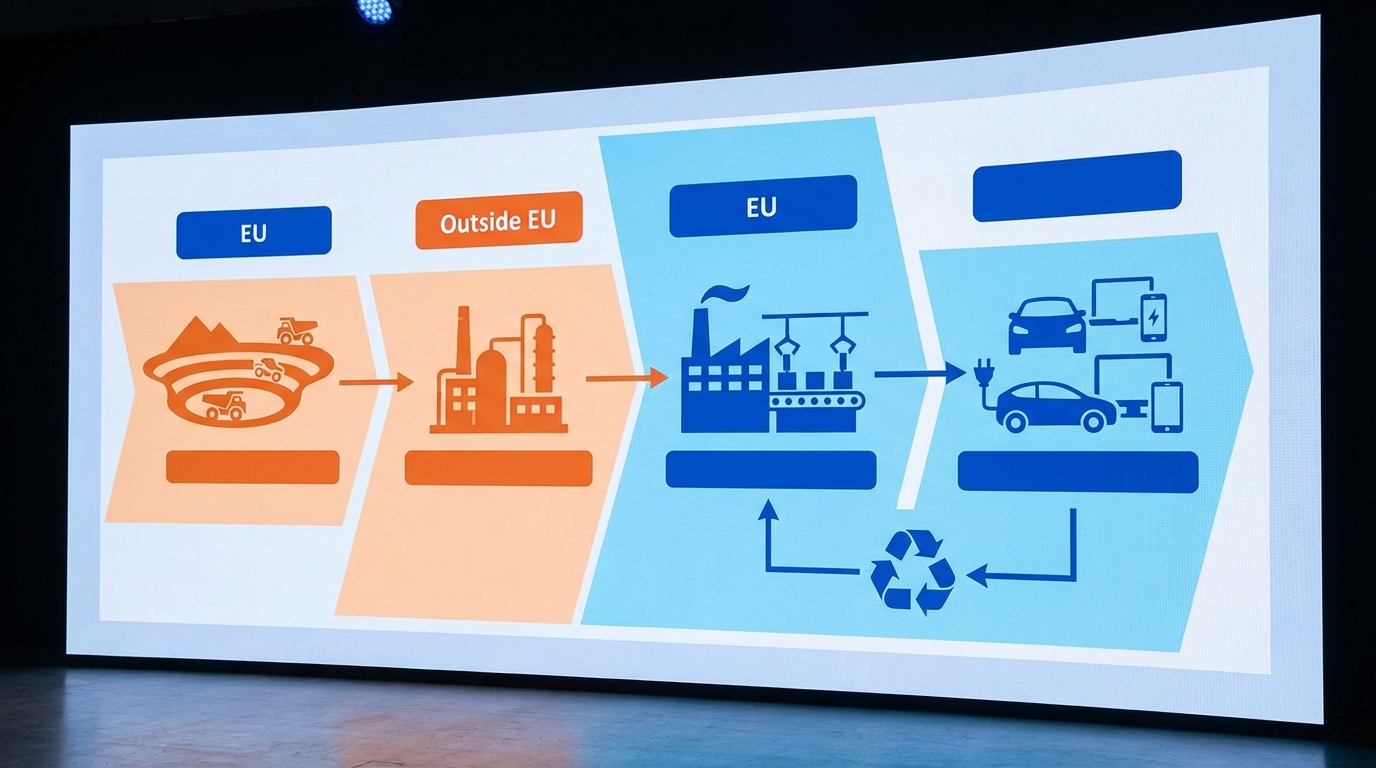

Defining the “By-Product Trap”

The term “by-product trap” captures a structural constraint: non-Chinese producers cannot scale gallium output quickly because gallium is produced incidentally during large-scale aluminum and zinc operations. Re-establishing recovery circuits typically requires multi-year investments, qualified permitting, and process validation—meaning volumes cannot be toggled at the speed that policy can be toggled. In practice, this creates a reflexive market dynamic: when restrictions tighten, buyers face not only availability risk, but also the prospect that higher prices may be temporary if Chinese supply temporarily re-accelerates later, suppressing incentives to build outside capacity.

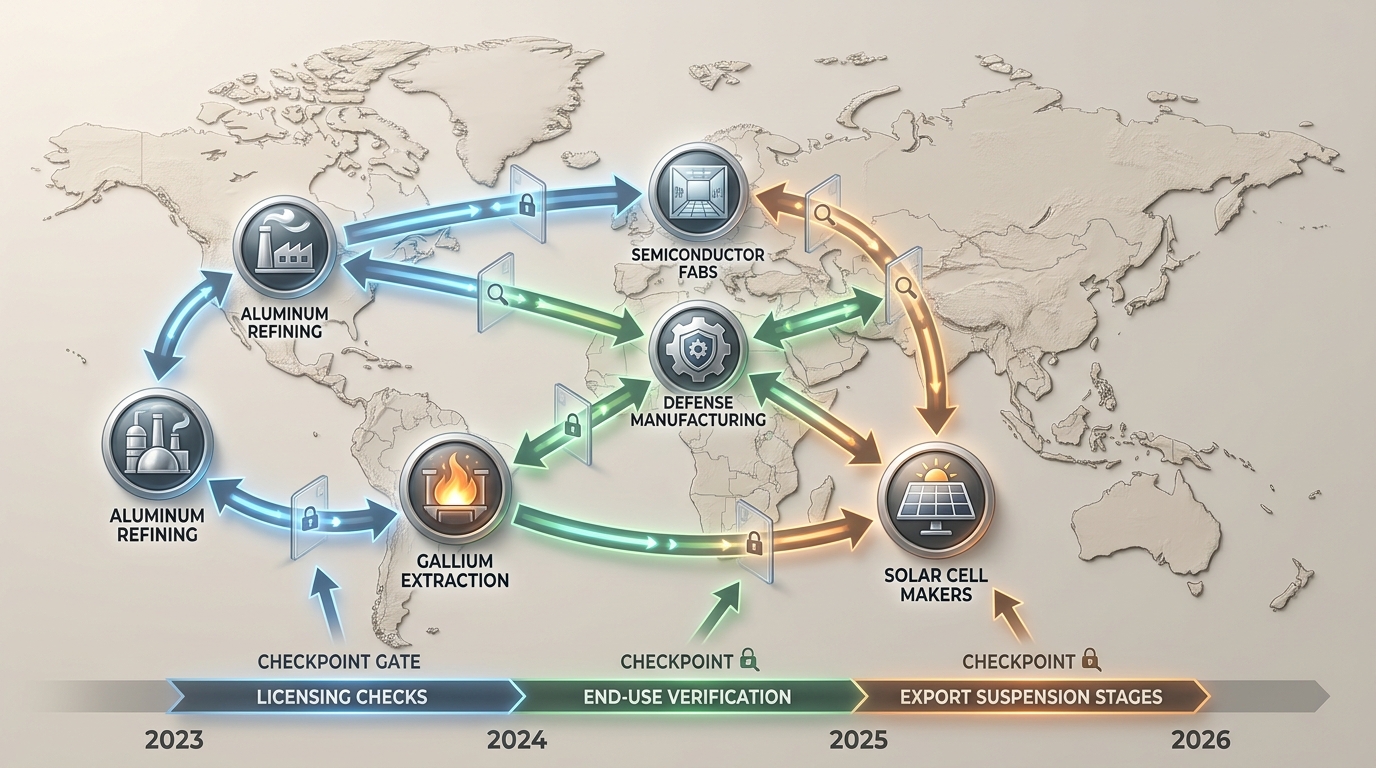

Export Control Timeline

July 2023: MOFCOM introduces licensing requirements for gallium and germanium exports, quickly reshaping pricing and export flows as end-use scrutiny tightens.

December 2024: Announcement No. 46 enacts a de facto embargo on U.S. gallium imports, halting civilian shipments and tightening the effective boundary for military end-use.

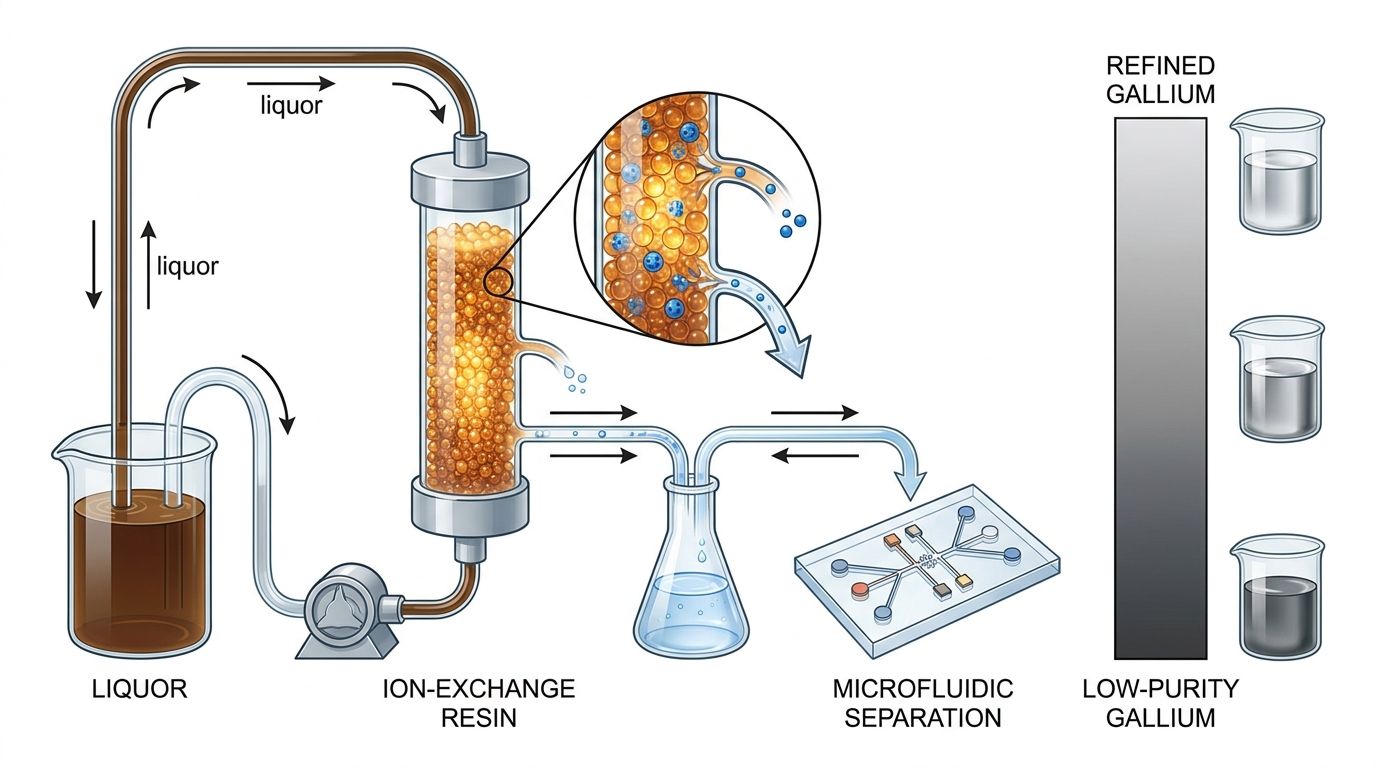

January–May 2025: Technology controls on extraction processes—specifically purification approaches that rely on ion-exchange and resin methodologies—alongside coordinated anti-smuggling enforcement deepen China’s chokehold on both volumes and know-how.

November 2025: Announcement No. 72 suspends the civilian embargo until late 2026 but preserves licensing authority, military restrictions and technology controls for rapid re-implementation.

Market and Price Dynamics

Gallium prices have behaved like a policy indicator rather than a pure supply-demand equilibrium. When licensing and enforcement tighten, buyers experience both immediate transactional friction (longer lead times, narrower sourcing channels, compliance overhead) and forward-looking uncertainty about whether volumes will be available in subsequent quarters. That uncertainty tends to flow through contracts, inventory strategies and safety-stock policies—raising effective demand even when end-user consumption has not changed.

USGS-based scenario analysis estimates that a sustained gallium and germanium cut-off could cost the U.S. economy $3.4 billion in GDP, with semiconductors bearing about half the impact. The key procurement implication is not merely “what happens if supply disappears,” but how quickly downstream plans can absorb upstream volatility when specifications, qualification testing and replacement approvals introduce friction.

Visual timeline of licensing → embargo → suspension and downstream impacts.

For market participants, the most important nuance is that gallium’s by-product origin means that alternative supply is not elastic. Even where material exists in scrap or industrial streams, converting it into usable gallium requires recovery pathways and quality certification—so short-term price signals do not automatically translate into rapid, fungible supply.

Fragmented Coverage and Strategic Blind Spots

Specialist commodity analysts and policy think tanks meticulously track gallium export measures, production quotas and price effects. Mainstream tech and gaming-oriented outlets, however, often focus on downstream semiconductor shortages—GPUs, AI chips and lithography capacity—without naming gallium as an upstream bottleneck. This siloed coverage risks underestimating how quickly a “hardware story” can become a “critical minerals story” when Beijing activates its regulatory switch.

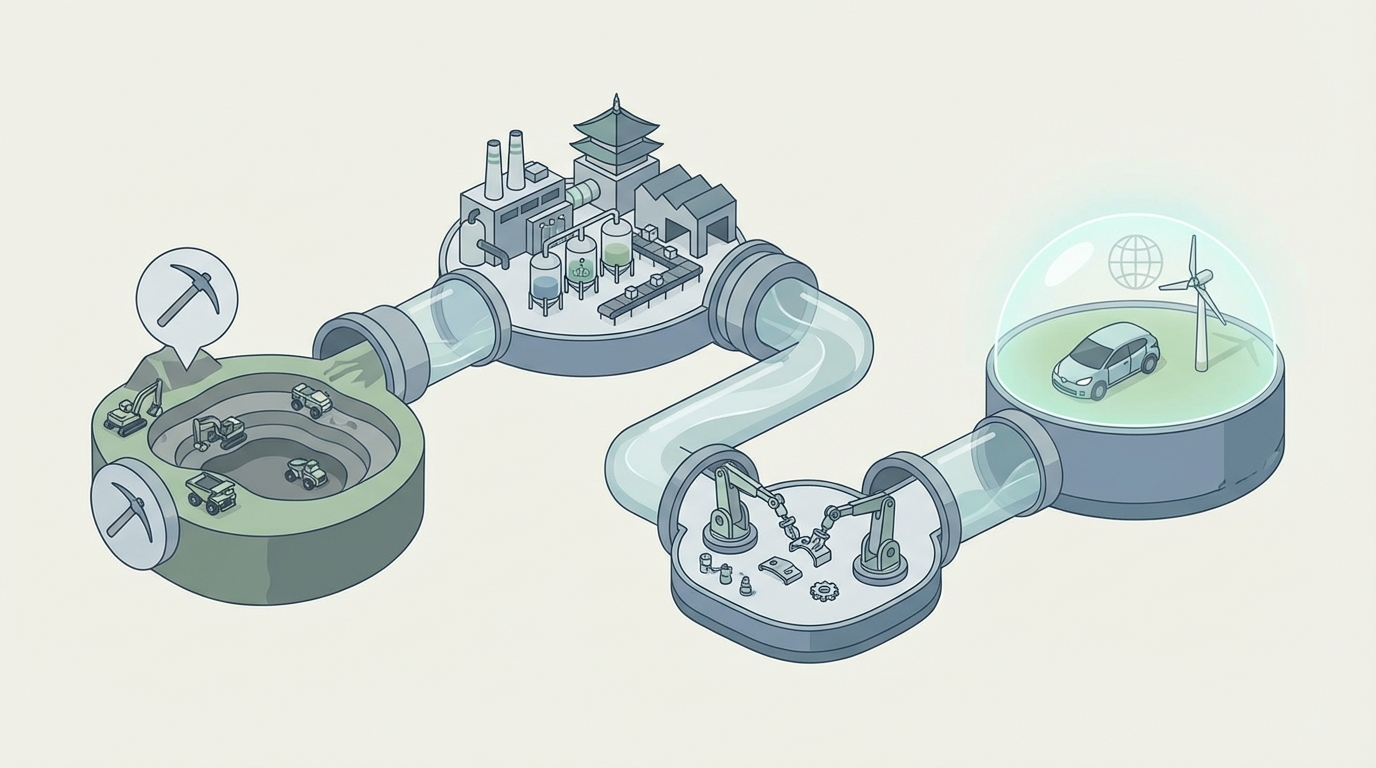

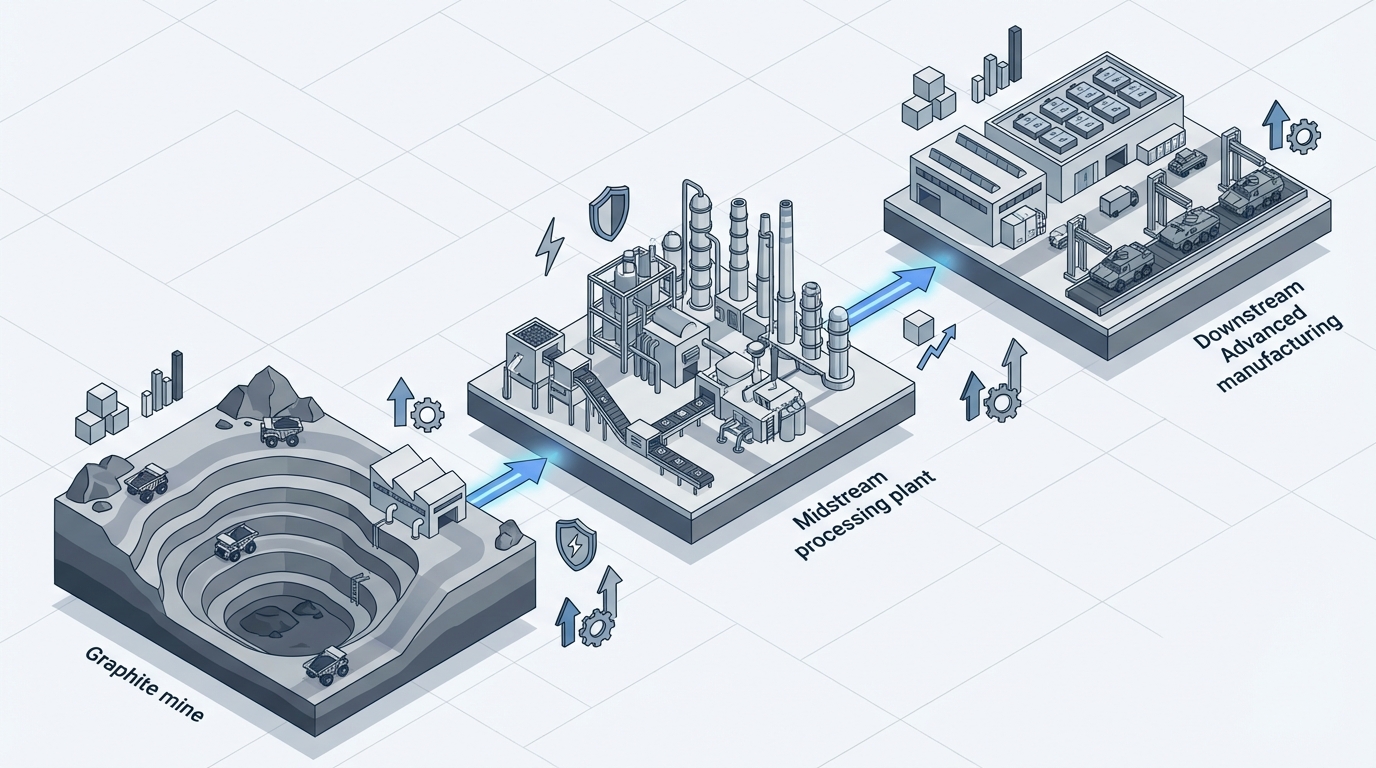

Process diagram showing why extraction technology is a control point.

For institutional stakeholders, the practical problem is measurement: if gallium exposure is not mapped by end-application, then policy moves can be misread as isolated input disruptions rather than as repeatable sovereign-risk events. In turn, that misreading delays mitigation—such as qualification of alternative feedstocks, redesign of procurement specifications, and compliance controls that prevent sourcing from becoming a legal and operational liability.

Allied Responses and Alternative Supply Efforts

Governments and firms in the U.S., EU, Japan, South Korea and Australia have launched feasibility work aimed at recovering gallium from bauxite, zinc and industrial scrap. European refiners and industrial groups have explored recovery pathways, while Japanese and Korean players emphasize closed-loop recycling strategies to reduce reliance on fresh primary feedstock. Australia’s bauxite-linked pathways have also been examined, though many efforts remain constrained by pilot-stage scale-up and commercialization risk.

Illustrate semiconductor supply vulnerability under export restrictions.

Across these initiatives, two challenges recur. First, by-product recovery is capital intensive: it requires additional processing steps, quality control and integration into existing refinery or waste-treatment workflows. Second, absent credible protection against future Chinese market surges, investment returns can remain uncertain—especially if policy can be tightened or relaxed faster than alternative capacity can qualify and deliver on consistent specifications.

Implications for Industry Stakeholders

Procurement and Category Management

Map direct and indirect gallium exposure. Treat gallium as a cross-cutting input across RF and power electronics, LEDs/optics, and PV-linked bills of materials—then document where qualification and substitution are realistic versus where they are not.

Scrutinize provenance, not just geography. Move beyond “country of last transformation” labels. For by-product metals, feedstock integrity and process history materially affect compliance posture and technical acceptance.

Negotiate inventory buffers and contractual resilience. Build flexible delivery terms, and add contingency clauses that explicitly address export control events and compliance-driven shipment holds.

Plan for recycled gallium as a structured supply lever. Integrate recycling streams from scrap and end-of-life devices where possible, and treat recovery yield variability as a managed risk rather than an assumption of steady-state output.

Supply-Chain Strategy and Operations

Scenario-plan for rapid policy toggles. Treat licensing changes, enforcement campaigns and temporary suspensions as repeatable scenarios. Then assess the downstream ripple effects on production schedules and inventory consumption rates.

Engage early with recovery projects, but anchor risk allocation. Use consortia or anchor offtake discussions to clarify who bears commercialization, yield and compliance certification risk.

Coordinate with R&D on material substitutes where technically viable. Substitute materials—such as silicon carbide in power electronics contexts—should be evaluated as qualification programs, not as instantaneous substitutes.

Embed regulatory monitoring into S&OP cycles. Incorporate signal monitoring across MOFCOM-linked developments and Western critical minerals/export control frameworks so forecasting assumptions are updated before procurement commitments become irreversible.

Trading Desks and Risk Management

Anticipate policy-driven volatility. Calibrate hedging logic to scenario distributions shaped by regulatory timing, not only by observed spot price behavior.

Monitor basis risk across venues. Track differences between Chinese domestic pricing signals, Rotterdam-linked market references, and end-user procurement pricing to avoid assuming uniform pass-through.

Avoid overestimating “normalization” from downstream announcements. Materials constraints—especially for by-product metals—can remain binding even when consumer-facing production schedules appear stable.

Compliance and Legal Considerations

Operate under dual-jurisdiction risk. Track both Chinese export control lists and Western critical minerals frameworks to prevent misalignment between sourcing decisions and compliance obligations.

Strengthen due diligence on intermediaries. Enhanced screening is essential for intermediaries and re-export hubs, given the elevated risk of illicit diversion pathways during policy tightening.

Prepare for evolving “trusted source” expectations. Expect procurement systems to increasingly favor documentation-intensive sourcing, especially where end-use verification and process provenance become gating factors.

Conclusion

China’s gallium playbook demonstrates how targeted export and technology controls on a by-product metal can deliver outsized leverage over critical supply chains. The November 2025 civilian suspension does not remove the underlying choke points; it only changes the timing and the conditions under which restrictions may be activated. Decision-makers should treat gallium as an enduring vulnerability—using this window to diversify sourcing, reinforce recycling, and institutionalize policy-risk scenarios into strategic planning.

Due Diligence Review: ESG and Community‑Risk Red Flags in Strategic Mineral Projects

We reviewed a cross‑section of 15 strategic mineral projects—covering rare earths, lithium, nickel, cobalt and platinum‑group metals (PGMs)—to assess how environmental, social and governance (ESG) issues and community disputes are affecting operational continuity and upstream supply availability. Our work draws on site and virtual audits, regulatory filings, local media monitoring and direct qualification discussions with operators and downstream offtakers.

Key Takeaways

ESG and community disputes consistently convert into hard operational events: delayed expansions, frozen tailings projects, and halted water licences, which in turn shorten effective supply.

Water and tailings management are the dominant technical flashpoints across jurisdictions; projects with independently verified systems show materially less disruption.

Indigenous and local equity participation tends to channel conflict into negotiation rather than obstruction; absence of meaningful sharing correlates with escalations.

Governance fragility and sanctions amplify local incidents into national policy responses that can materially reduce available tonnage to ESG‑sensitive offtakers.

Analytical Lens: How ESG and Community Risk Becomes an Operational Event

The principal lesson from the dataset is straightforward: ESG disagreements rarely remain within public affairs teams. They become path‑critical operational events—delayed shaft sinking, frozen concentrator upgrades, revoked water or tailings permits—that sit on the same schedule drivers as geotechnical failures or metallurgical setbacks.

Across the portfolio four structural channels dominate:

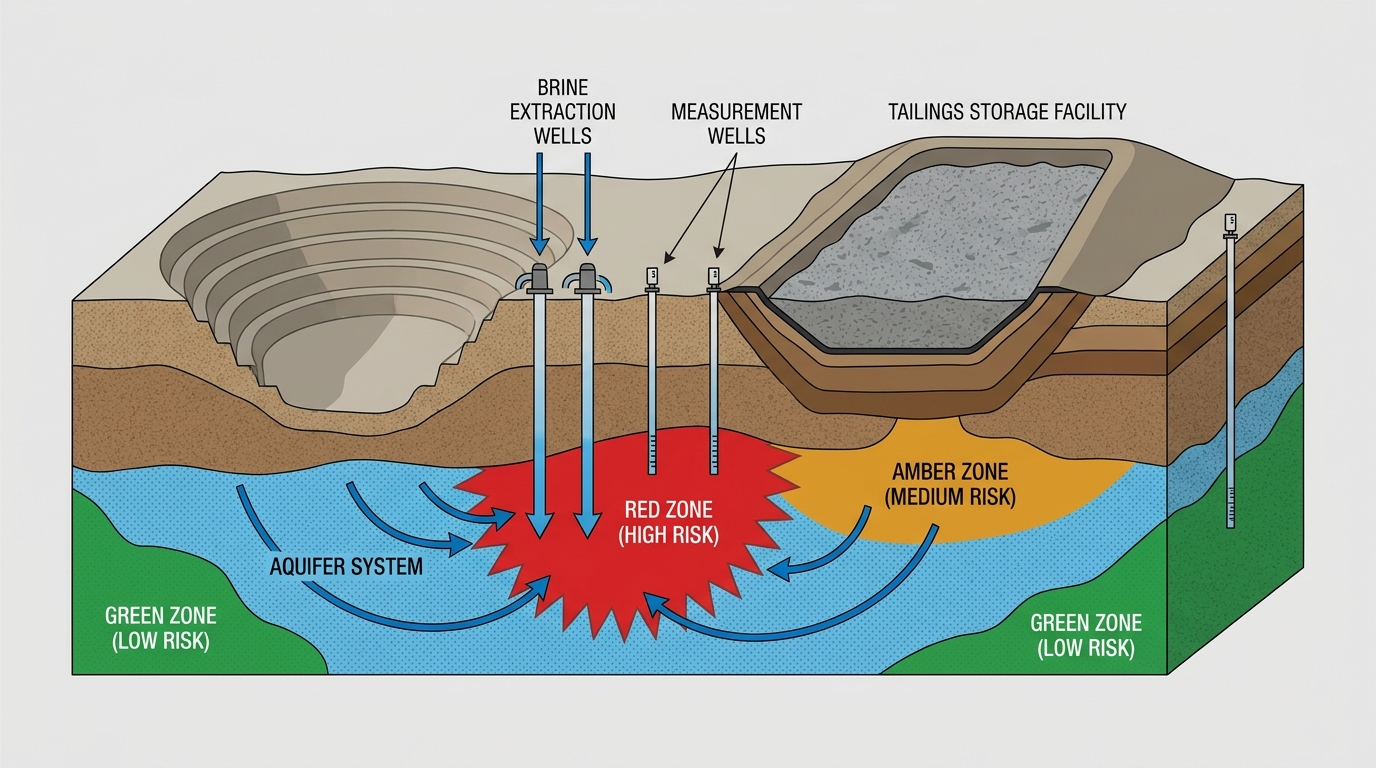

Water and tailings exposure – Community concern about groundwater drawdown and tailings storage repeatedly triggers regulatory pauses. Projects adhering to international standards such as the Global Industry Standard on Tailings Management (GISTM) and with transparent monitoring experience shorter interruptions.

Indigenous and community consent – First Nations and Indigenous groups are asserting leverage through court actions, blockades and renegotiation of impact‑benefit agreements; this operates as an ongoing critical path risk rather than a single permitting hurdle.

Climate and natural‑hazard sensitivity – More frequent heatwaves, cyclones and permafrost thaw interact with legacy infrastructure and tailings designs to create recurring outage patterns.

Governance and sanction fragility – In jurisdictions with sanction or export‑control exposure, ESG findings are rapidly entangled with national policy, export quotas (government limits on the volume or value of goods allowed to leave a country) and external audits, increasing the probability of supply disruptions.

Power and infrastructure reliability – Opposition to new transmission lines or access roads compounds logistical fragility, producing bottlenecks that amplify delivery variance.

From a supply‑chain perspective, this collapses into a few operational questions: Will a water license or tailings permit hold through expansion? Is social licence resilient to a geotechnical setback? Are sanction and reputational risks acceptable for downstream OEMs with internal ESG screens?

Case Focus: Rare Earth and Lithium Supply in the United States

Two US projects in the dataset—Mountain Pass (California) and Thacker Pass (Nevada)—illustrate how ESG dynamics can shape strategic mineral reliability even in jurisdictions perceived as stable. Together they underpin a sizeable share of planned non‑Chinese NdPr (neodymium‑praseodymium) magnet feedstock and lithium carbonate for batteries. Note: we use TREO to refer to total rare earth oxides and LCE to refer to lithium carbonate equivalent, terms which appear below when discussing volumes and sourcing.

Geopolitical and ESG-risk overview map (illustrative).

Mountain Pass: Legacy Environmental Liabilities Meet New Supply Imperatives

Mountain Pass remains a cornerstone of non‑Chinese rare earth oxide (TREO) production. Our dataset characterises current production near 40,000 tonnes per year of rare earth oxides, with medium‑term plans toward ~60,000 tpa. The project sits at an uncomfortable intersection of legacy liability and strategic indispensability.

Critical findings with direct continuity implications:

Water stress in a sensitive basin – Legal action by local tribes over groundwater extraction has previously interrupted expansion permitting for more than a year, placing debottlenecking plans in limbo.

Tailings seepage and regulatory fines – Historic seepage concerns have attracted significant penalties and made hydrological audits de facto gatekeepers for license renewal and expansion approvals.

Incomplete water recycling implementation – Management proposals for closed‑loop water circuits have not yet achieved full capture; tightening extraction limits could quickly constrain throughput.

Climate exposure – Heatwaves that curtail open‑pit operations create short‑term production swings that ripple through just‑in‑time magnet supply chains.

For market planners, Mountain Pass demonstrates that a single ESG incident can trigger policy debates at state and federal levels, elevating supply risk beyond the local operating horizon. When substitutes at comparable scale are scarce, even a modest output shortfall materially tightens upstream availability for magnet manufacturers and defense users.

Thacker Pass: Social Licence on the Critical Path for US Lithium Supply

Thacker Pass, envisaged to produce around 40,000 tpa LCE, has become a test case of how community opposition can extend timelines in OECD settings. Internal tracking showed slippage in first‑production guidance—driven mainly by permitting pauses rather than technical redesigns.

Water-and-tailings risk cross-section for battery metals projects.

Core risk elements:

Indigenous rights and sacred sites – Litigation by Paiute‑Shoshone groups over cultural heritage paused key Bureau of Land Management processes and disrupted construction sequencing.

Water use in an arid catchment – Hydrogeological assumptions about aquifer recharge have been challenged by local stakeholders, framing water competition as central to the dispute.

Ore and process complexity – Clay‑hosted lithium raises ongoing questions about grade consistency and impurity management; perceptions of under‑reported waste volumes have reinforced community scepticism.

National policy overlay – The project’s prominence in industrial policy and incentive frameworks has elevated local disputes to national‑level debate, slowing negotiated compromise.

Operationally, Thacker Pass underscores a risk inflection point common to long‑life projects in contested landscapes: social licence operates continuously. Downstream cathode and cell manufacturers have moved from a single “on‑time” sourcing case to a suite of scenarios—on‑time, slow‑ramp, stalled—each with different implications for blending strategies and compliance with domestic content rules.

High‑Risk Jurisdictions: Cobalt, Nickel and the ESG–Governance Nexus

Projects in the Democratic Republic of Congo (DRC), Papua New Guinea (PNG), Russia and Cuba illustrate a different dynamic: community incidents intersect with governance fragility and geopolitical stress to produce layered continuity risk.

Examples from the portfolio:

DRC copper–cobalt complexes – Interfaces with artisanal mining, resettlement disputes and river contamination led to logistical frictions—blocked roads, temporary export holds and curfews—that compressed effective deliveries even when nameplate figures looked intact.

PNG Ramu nickel–cobalt – Deep‑sea tailings placement and reported pipeline ruptures mobilised community blockades and government reassessments, turning single incidents into multi‑month access constraints exacerbated by cyclone exposure.

Russian Arctic operations – Chronic emissions and spills have prompted Indigenous protests and international scrutiny; when coupled with sanctions, these incidents restrict access to Western technology and financing, affecting maintenance and upgrade schedules.

Cuban nickel projects – Hurricanes and embargo‑related equipment constraints have combined to raise the operational and reputational cost of continued output in that jurisdiction.

Across these contexts, disruptions rarely manifest as permanent shutdowns. More commonly they increase delivery variance and raise compliance risk for ESG‑aware offtakers, who often reduce reliance on assets that migrate onto internal watch lists.

Community engagement flashpoint near a mining site.

Patterns and Monitoring Signals Across the Portfolio

Five recurring patterns matter for supply‑chain planning:

Water and tailings as primary flashpoints – Transparent, GISTM‑aligned designs and third‑party audits reduce disruption severity.

Indigenous/local equity participation – Shared‑value models convert conflict into negotiation more often than obstruction.

Climate impacts folded into community narratives – More frequent extremes increase scrutiny of “design storm” assumptions.

Governance risk amplifies incidents – Weak institutions can translate local disputes into license suspensions or royalty overhauls.

Downstream ESG screening as a demand‑side shock – Once a project is flagged for human‑rights or tailings failures, offtakers may diversify even while the mine remains operational.

Useful monitoring signals include: the tone and frequency of regulator communications; the presence of revenue‑sharing or equity structures with host communities; timing of tailings expansion or dam redesigns; renewal windows for water and emissions licences; and whether incidents become national political issues or remain local and resolvable.

Risk Inflection Points

Particular inflection points warrant close attention because they often trigger upstream re‑evaluations:

Transition phases for tailings capacity or tailings‑design changes.

Renewal or amendment periods for key water and emissions licences.

Revisions to Indigenous impact‑benefit agreements.

High‑profile environmental incidents that attract national media.

National elections or regulatory overhauls that reframe resource sovereignty debates.

Conclusion

Our review concludes that ESG and community factors are now core supply‑chain variables for strategic minerals. Projects that pair credible, independently verified tailings and water management with transparent benefit‑sharing and contingency planning demonstrate materially greater resilience. For market participants, durable access to critical feedstocks increasingly requires understanding both the geology and the governance surrounding production.

Materials Dispatch cares about this topic for a simple operational reason: in every missile-defense sourcing cycle examined over the last decade, the technical bill of materials led back to the same bottleneck – Chinese rare earth processing and magnet capacity. Export-control scares, supplier failures, and the scramble to qualify even small non-Chinese magnet volumes have turned that bottleneck from an abstract geopolitical trope into a daily procurement constraint. The current Israel-Iran missile dynamic exposes that constraint brutally: the same country underpins the magnets inside the Arrow interceptor defending Tel Aviv and the navigation architecture inside the Fattah-series missiles flying toward it, while also positioning itself as a diplomatic broker. That is not a paradox; it is supply chain design.

The underlying change is not a single law but the convergence of China’s roughly 90% control of rare earth processing, documented interceptor depletion in Israel, and slow-moving Western diversification efforts.

Covered scope includes neodymium and samarium-cobalt magnet dependence in Arrow, THAAD, Patriot and David’s Sling; BeiDou-3 use in Iranian missiles; and Chinese leverage via oil trade and rare earth chokepoints.

Operations are constrained by long magnet lead times, qualification cycles, and the reality that the US remains 100% net import dependent on finished rare earth magnets while EU and Japan only begin to scale alternatives.

Interpretation remains bounded by public data; quantified 2026 shortage and price scenarios derive from published modeling, not from Materials Dispatch forecasts.

The central asymmetry: China can influence both Israeli interceptor resupply and Iranian missile performance through materials and navigation supply chains in a way no other actor currently can.

FACTS: The Supply Chain Architecture Behind Sword, Shield, and Diplomacy

China’s Dominance in Rare Earth Processing and Finished Magnets

Open-source assessments converge on a central fact: China processes around 90% of the world’s rare earth oxides into usable materials and components. This includes the conversion of mined concentrates into separated oxides, metals, and high-performance magnets. The Australian Strategic Policy Institute (ASPI), in its work on strategic dependencies, has described US missile defense in particular as critically exposed to Chinese-controlled rare earth and magnet supply chains.

Rare earth permanent magnets – primarily neodymium–iron–boron (NdFeB) and samarium–cobalt (SmCo) – are mission-critical in modern missile defense systems. They appear in:

Actuators for aerodynamic control surfaces and thrust-vectoring in interceptors such as Arrow and Patriot.

Gimbal motors and guidance assemblies in seekers and radar systems used by THAAD and David’s Sling.

Electric drive systems inside radar arrays and fire-control systems supporting these batteries.

The United States is assessed by government and academic sources as being 100% net import dependent on finished rare earth magnets. The bulk of those finished magnets, even when sourced via intermediaries, originate from Chinese processing and manufacturing capacity.

ASPI’s analysis of US missile defense identifies Chinese-controlled rare earth supply and magnet manufacturing as chokepoints for critical systems, including Patriot and THAAD, where magnet substitution or redesign is either technically constrained or would take years to validate for combat use.

Interceptor Depletion: RUSI Data on Arrow and David’s Sling

The Royal United Services Institute (RUSI) has documented the pace at which Israel’s missile-defense interceptors have been consumed under sustained attack. One assessment reports approximately 122 of 150 Arrow-2/3 interceptors used, and 135 of 250 David’s Sling interceptors expended, in recent barrages. That translates into a significant drawdown of stockpiles for systems that depend heavily on rare earth magnet content throughout their guidance and actuation subsystems.

RUSI’s depletion figures do not themselves quantify magnet consumption. that said, given that each interceptor embodies multiple NdFeB and, in some high-temperature locations, SmCo components, these depletion rates map directly into magnet replacement requirements. Replacement is constrained not only by financial appropriations and assembly capacity, but by the availability of qualified magnet supply – overwhelmingly tied back to Chinese processing.

Iranian Missiles and BeiDou-3 Military-Grade Navigation

On the offensive side of the current regional dynamic, Iranian ballistic and cruise missiles – including advanced designs such as the Fattah family – have reportedly integrated China’s BeiDou-3 satellite navigation system. Open-source technical analyses describe the use of BeiDou-3 military-encrypted signals, which enhance accuracy and resilience relative to unencrypted civilian navigation feeds.

These missiles also rely on components and materials that run through Chinese supply lines more broadly, including electronics, machine tools, and precursors relevant to propellant and structural materials. While not all of these rely on rare earths, the navigation and guidance stack is directly tied into Chinese space-based infrastructure and related component ecosystems.

China is also reported to purchase roughly 80% of Iran’s oil exports, largely through channels that circumvent formal Western sanctions frameworks. That oil revenue underpins Tehran’s fiscal capacity for missile development and procurement. The same bilateral trade relationship that moves oil also provides a foundation for technology, component, and materials flows relevant to Iran’s missile programs.

Western Vulnerability: ASPI and West Point Modern War Institute Assessments

ASPI’s report on strategic rare earth dependence in US missile defense highlights two linked facts:

Chinese entities dominate the separation and processing stages for the specific rare earth elements required in high-coercivity NdFeB and SmCo magnets used in missile guidance and actuation.

US missile defense programs rely on these magnets with limited substitute materials or designs qualified to the same performance and reliability standards.

The Modern War Institute at West Point has framed China’s rare earth monopoly as a national security risk, warning that a disruption in Chinese rare earth or magnet exports could significantly degrade the US defense industrial base’s ability to sustain missile-defense sortie rates. The institute’s assessment emphasizes the time required – measured in years, not months – to stand up non-Chinese alternatives at every stage from oxide separation to finished magnet production and system-level qualification.

Regulatory and Strategic Responses: EU CRMA, Japan’s Stockpile, and 2026 Horizon Scenarios

Several jurisdictions have begun codifying responses to this structural dependence, with direct implications for defense supply chains:

European Union – Critical Raw Materials Act (CRMA): By the second quarter of 2025, the CRMA’s Phase 2 benchmarks include a target for 10% of certain critical raw materials, including rare earths, to be processed domestically within the EU. For defense contractors, non-compliance can trigger fines reportedly in excess of €10 million, creating a formal regulatory incentive to diversify away from Chinese processing.

Japan – Rare Earth Strategic Stockpile: By the fourth quarter of 2025, Japan’s rare earth strategy envisages doubling its strategic stockpile of NdFeB magnets to around 5,000 metric tonnes. This is particularly relevant given Japanese partnerships in missile-defense programs and co-production, where Japanese magnet capacity can act as a partial hedge against Chinese disruption.

2026 Horizon – Chinese Quota Scenarios: Bloomberg Intelligence has modeled potential Chinese quota tightening that could displace on the order of 13,000 metric tonnes of rare earth supply from global markets by 2026. In that scenario, Western buyers face modeled aggregate premiums of USD 2–3 billion, with dysprosium prices reaching around USD 1,200 per kilogram. These are scenario analyses, not certainties, but they illustrate the magnitude of financial and supply stress modeled under tighter export quotas.

These moves coexist with national-level programs in the US and elsewhere to seed domestic mining, separation, and magnet manufacturing, often through defense-focused industrial policy. However, the provided data do not specify exact volume or timing beyond the broad 2025–2026 horizons and the Japanese stockpile target.

China as Diplomatic Host and Supply Chain Gatekeeper

Parallel to its role as a materials and navigation supplier to both Israeli-aligned and Iranian-aligned systems, Beijing has positioned itself as a host for diplomatic initiatives and potential peace talks related to the conflict. This juxtaposition – Chinese-origin magnets inside interceptors defending Tel Aviv, Chinese navigation and trade flows enabling missiles targeting Israeli cities, and Chinese diplomats convening discussions – is grounded in the same structural fact: control over a set of industrial chokepoints that neither side can rapidly replace.

INTERPRETATION: How Structural Dependencies Translate into Leverage

From Monopoly to Leverage: The Asymmetry Embedded in Rare Earth Processing

To the extent that China maintains roughly 90% of rare earth processing and dominates finished magnet production, it holds a structural lever over both the pace and sustainability of missile-defense resupply in Israel, the US, and allied states. ASPI and West Point’s Modern War Institute are aligned on one core point: Western missile-defense architectures were built under an implicit assumption that cheap, reliable Chinese magnet supply would persist indefinitely. That assumption has already been challenged by Chinese export controls on other strategic materials such as gallium and germanium; magnets and rare earths sit one policy step away from similar treatment.

If Beijing were to tighten export licensing on specific magnet grades, prioritize domestic civil-industrial demand, or simply allow longer administrative delays for exports, interceptor production lead times in allied states would stretch. RUSI’s depletion figures show that Arrow and David’s Sling stocks can be drawn down quickly under sustained attack. In a scenario where interceptors are expended faster than they can be replaced and critical magnet components face longer or uncertain delivery, system-level readiness could erode even if funding and assembly capacity exist on paper.

The asymmetry is clear: even modest changes in Chinese export posture can ripple through Western defense industrial bases far more quickly than Western diversification efforts can come online. The multi-year timelines associated with new rare earth separation plants, alloying lines, and magnet factories put Western systems on the back foot in any short-notice crisis.

The “Sword and Shield” Feedback Loop: Iranian Missiles vs. Israeli Interceptors

The same industrial ecosystem that supports Western interceptors also underpins key capabilities on the Iranian side, albeit in different ways. BeiDou-3 integration into Iranian missiles ties guidance performance directly into Chinese space infrastructure and chipset ecosystems. Chinese demand for Iranian oil, reportedly around 80% of Tehran’s exports, provides fiscal oxygen for missile development programs. And Chinese-origin components and manufacturing know-how appear repeatedly in open-source missile forensics and supply chain mappings.

That said, there is an important structural difference. Iranian systems can tolerate cruder performance in some cases: larger circular error probable, more reliance on volume of fire rather than exquisite precision, and more flexible use of mid-tier electronics. Israeli and US missile-defense systems, by contrast, are engineered around high-precision intercepts that demand top-end guidance and control hardware. This makes magnet performance less fungible on the defensive side than on the offensive side.

If Chinese rare earth and magnet exports to Western-aligned defense industries were curtailed, Israeli interceptor production could face near-term constraints that would not automatically translate into equivalent constraints on Iranian missile output. Oil revenues can be redeployed into alternative components; guidance performance can be traded for volume; and lower-tech solutions can be fielded. The shield is more technologically brittle than the sword, and that brittleness runs straight through the magnet supply chain.

Regulation vs. Reality: Can EU, US, and Japan Close the Gap in Time?

On paper, measures like the EU CRMA’s 10% processing benchmark and Japan’s 5,000-tonne NdFeB stockpile are rational responses. They recognize that defense readiness is inseparable from critical materials security. However, these targets also underscore how small current non-Chinese capacities remain relative to global demand and to the concentration of processing in China.

If Bloomberg Intelligence’s 2026 quota scenario materializes – displacing roughly 13,000 tonnes of rare earth supply and driving modeled Western premiums and dysprosium price spikes – magnet availability for defense programs could become an explicit allocation problem rather than a background procurement concern. At that point, even well-intentioned regulatory benchmarks would be chasing a moving target: as China tightens supply or raises its own downstream consumption, the baseline against which “10% domestic processing” is measured may itself shrink in export-available terms.

In practice, Western defense primes and ministries have already begun multi-sourcing and pre-qualification of non-Chinese magnet suppliers. Yet, based on program-level audits Materials Dispatch has observed, qualification cycles often run several years, especially for high-reliability missile components. Even under optimistic scenarios, these efforts are unlikely to fully offset a determined Chinese tightening by 2026. The risk is a transitional window where stocks of interceptors – already partially depleted, as RUSI’s data shows – need fast replenishment, while the magnet supply base is still only partially diversified.

Diplomatic Hosting as an Extension of Industrial Power

Beijing’s role as a host for talks touching on Israel–Iran tensions is often framed purely in traditional diplomatic terms. From a materials and industrial perspective, it also reflects the reality that China sits at the junction of both parties’ critical supply chains. That positioning alters the geometry of any negotiation, even if it is never stated explicitly.

If Chinese policymakers perceive value in de-escalation, they have structural options – ranging from quiet tightening of certain export channels to technical “maintenance windows” in satellite navigation services – that could, in principle, alter the material conditions of the conflict. Conversely, neutral or permissive export behavior can allow both missile offense and missile defense to continue drawing on Chinese-enabled capabilities. The key point is not speculation about intent but recognition of capacity: no other state currently has comparable leverage over both sides’ material warfighting architectures at once.

This leverage does not automatically translate into overt coercion. It does, however, give Beijing a background influence over timelines: how fast interceptors can be replaced, how quickly certain missile capabilities can be iterated, and how credible long-war planning looks to capitals that remain magnet-dependent. In Materials Dispatch’s view, that quiet, structural power is underappreciated in mainstream assessments of the conflict.

WHAT TO WATCH: Signals of Shifting Leverage

Chinese export licensing for rare earth magnets: Any move to add specific NdFeB or SmCo grades to tighter dual-use control lists, extend processing times, or introduce end-use certification requirements directly affecting defense contractors.

MOFCOM quota announcements and commentary: Changes in annual or quarterly rare earth export quotas, especially language prioritizing domestic clean-tech or industrial upgrading over exports, which would squeeze available volumes for defense end-uses.

Implementation details of EU CRMA enforcement: Actual enforcement actions or fines against defense suppliers over critical raw materials sourcing, which would signal how seriously Brussels intends to push non-Chinese processing for strategic programs.

Japan’s strategic stockpile drawdowns: Evidence that Tokyo is tapping NdFeB stockpiles for defense co-production, particularly in missile or radar programs, would indicate that stress in global magnet markets is filtering into operational planning.

US magnet manufacturing milestones: Commissioning of full-value-chain facilities (from separated oxides to finished magnets) and, crucially, their qualification into specific missile-defense programs, not just commercial EV or wind applications.

BeiDou-3 service posture and chip export patterns: Any change in availability, signal characteristics, or export rules for high-grade BeiDou navigation modules to Middle Eastern buyers, particularly those linked to Iranian missile programs.

China–Iran oil trade volumes and terms: Sustained or rising Chinese intake of Iranian oil, especially under sanctions pressure, which continues to underpin missile development budgets and trade-based access to dual-use goods.

RUSI and similar analyses on interceptor stockpiles: Updated figures on Arrow, David’s Sling, Patriot, and THAAD inventories and usage rates under attack scenarios, as a real-time proxy for magnet-demand stress.

Public or leaked references to magnet shortages in defense contracting: Contract delays, program re-baselining, or formal notices citing rare earth or magnet availability as a schedule driver.

Beijing’s public framing of its mediation role: Shifts in Chinese official rhetoric that link peace initiatives with “stability in global supply chains”, which would indicate an explicit awareness of leverage at the intersection of materials and security.

Conclusion

The current missile confrontation around Israel reveals more than tactical interplay between interceptors and incoming missiles; it exposes the degree to which both offense and defense are wired into the same Chinese-centered materials and navigation infrastructure. Rare earth magnets and BeiDou-3 chips are not abstract strategic assets – they are the quiet components that determine how many salvos can be fired, how accurately, and for how long.

Regulatory moves in the EU, stockpiling in Japan, and nascent US magnet initiatives acknowledge the risk but do not erase the near- to medium-term asymmetry. As long as the United States remains fully import dependent on finished rare earth magnets and China dominates processing, Beijing holds structural leverage over the tempo and sustainability of Western missile-defense operations. For Materials Dispatch, active monitoring of regulatory and industrial weak signals around these chokepoints remains central to understanding how the next phase of this conflict – and any negotiated outcome – will be materially constrained.

Note on Materials Dispatch methodology Materials Dispatch builds its briefings by cross-referencing primary texts from relevant authorities and administrations with open-source defense analyses and specialist research on rare earth supply chains. These regulatory and technical readings are then mapped against observed market behavior and end-use specifications in systems such as missile interceptors and satellite-navigation-guided munitions, to link legal frameworks and industrial capabilities with concrete operational constraints.

The Pentagon is pivoting from buyer to equity investor across rare earths and missile propulsion, deploying roughly $9.5B in direct stakes and structured financing and becoming a dominant capital provider in U.S. critical minerals supply chains.

The Pentagon Becomes a Shareholder: Equity as Industrial Policy in Critical Minerals and Missile Propulsion

Executive Summary

Over the past 18 months, the U.S. Department of Defense (DoD) has shifted from a traditional buyer-supplier model toward direct equity and equity-like stakes in critical minerals and weapons manufacturers, committing approximately $9.5 billion across at least six major transactions, alongside a $9 billion expansion of Defense Production Act (DPA) Title III authority for broader industrial base investment [1][8][25]. This marks a structural pivot in U.S. industrial policy at the intersection of defense, critical minerals, and capital markets.

Flagship moves include an estimated $400 million equity-led package into MP Materials to scale U.S. rare earth magnet capacity [1][5], a $1.6 billion Commerce/DoD-backed package for USA Rare Earth combining a $1.3 billion senior secured loan with equity and warrants [1], and a $1 billion convertible preferred investment in L3Harris’s Missile Solutions business that will convert into common equity at a planned H2 2026 IPO, making DoD the anchor investor [2][9]. Parallel deals with Vulcan Elements/ReElement, Trilogy Metals, and Korea Zinc extend this model into recycling, copper, and other critical materials [8][12][13][20].

These interventions seek to counter China’s ~95% control of heavy rare earth output and the U.S. dependence on China for ~90% of its heavy rare earth imports [6], but they also embed the Pentagon deeply in corporate governance, capital structure, and long-term project risk. For defense OEMs, miners, and investors, the core question is no longer whether the state will back domestic supply chains, but on what terms and with what strategic and governance consequences.

Immediate actions (next 30 days)

Map exposure: Identify portfolio, JV, and supply-chain links to DoD-backed assets (MP Materials, USA Rare Earth, Vulcan/ReElement, Trilogy, L3Harris Missile Solutions) and flag governance interfaces where DoD is or could become a material shareholder [1][2][5][12][13][20].

Stress-test procurement strategies: For defense primes, model scenarios where DoD equity ownership influences source approval, volume allocations, and pricing in magnets, heavy rare earths, and solid rocket motors [2][5][6][11].

Engage early with Office of Strategic Capital (OSC): Mining and processing developers should align project milestones and financing structure to OSC/DPA Section 303 criteria before DPA Title III solicitations close in the current budget cycle [1][8][25].

Risk / Impact / Timing

Risk level: High – structural shift in state-industry relations, concentrated in few critical assets [1][5][6][8].

Impact: Multi‑billion‑dollar distortions in capital allocation; potential single‑asset dependencies in magnets and propulsion >$5 billion program exposure per major platform cluster [2][5][6].

Crisis timing: 2026–2030 – coinciding with H2 2026 L3Harris Missile Solutions IPO, MP/USA Rare Earth hydromet and magnet commissioning, and potential further Chinese export control moves [1][2][5][9][11].

The Problem

At the core of the Pentagon’s equity turn lies a hard constraint: the U.S. warfighting ecosystem depends on critical minerals and components largely controlled by geostrategic competitors. As of 2024, the United States was 100% net-import reliant for 12 critical minerals and at least 50% reliant for 29 more [10][24]. For heavy rare earths such as dysprosium and terbium-indispensable for high‑performance permanent magnets in fighter aircraft, missiles, radar, and naval propulsion-China controls around 95% of global output, and roughly 90% of U.S. heavy rare earth imports come from China [6].

While the U.S. is the world’s second‑largest producer of unprocessed rare earth oxides, it has historically lacked domestic processing and magnet manufacturing, forcing U.S. producers to export oxides to foreign refiners-predominantly in China—and reimport finished materials [10]. This structural weakness was weaponized in 2025 when Beijing imposed export controls on 12 rare earth elements and related technologies with direct application to permanent magnets and defense systems [11]. Subsequent trade data indicated that, even after a limited one‑year “truce” announced in mid‑2025, China restored exports of finished magnets but kept upstream rare earth metals and compounds below pre‑control baselines, underscoring its enduring leverage [11].

Traditional defense procurement tools—multi‑year purchase contracts and marginal capacity payments—have proven insufficient to change this risk calculus. Capital‑intensive rare earth separation, hydrometallurgy, and magnet plants face long lead times, technology risk, and the threat of Chinese price suppression. Without visible state risk‑sharing, private capital remained reluctant to fund U.S. projects at the necessary scale and speed [1][5][8][12].

From the Pentagon’s perspective, the result was an industrial base that could not be reshored by “writing bigger purchase orders” alone. The response has been to deploy DPA Section 303 and Industrial Base Assessment and Sustainment (IBAS) authorities in new ways, using the Office of Strategic Capital to structure loans, convertible preferred securities, warrants, and long‑term offtake and price‑floor commitments [1][5][8][12][25]. This transforms the DoD from a purchaser into a shareholder and co‑financier, embedding it in the capital stack of mines, refineries, and weapon‑system OEMs.

For operators and investors, the problem is two‑sided. On one hand, equity participation may be the only credible path to build magnet, hydrometallurgy, and propulsion capacity outside China within this decade. On the other, it creates new governance and execution risks: concentration of state support in a handful of firms; potential misalignment between national‑security objectives and minority shareholders; politicization of capital allocation; and the possibility that over‑reliance on a small portfolio of DoD‑backed assets simply re‑creates a different version of single‑source dependence.

Current State

The shift toward equity has unfolded through a compressed series of policy moves and transaction announcements since early 2025. Below we outline the key milestones and their implications for critical minerals and defense production.

Policy and Authority Build‑out (2025)

March 2025 – Executive Order on Minerals. A presidential order on “Immediate Measures to Increase American Mineral Production” directed agencies to identify mineral projects for expedited permitting, coordinate loans and capital assistance, and explicitly instructed the DoD and Department of Energy to develop a plan for a Defense Finance Corporation to create a dedicated fund for domestic mineral investments under DPA authority [25]. This provided direct presidential cover for equity and quasi‑equity tools in mining and processing.

April 2025 – Acquisition Modernization Order. A follow‑on executive order on “Modernizing Defense Acquisitions and Spurring Innovation in the Defense Industrial Base” adopted a more flexible toolkit: expanded Other Transactions Authority, rapid capabilities mechanisms, and direct lending or investment pathways outside the traditional Federal Acquisition Regulation (FAR) model [26]. The order framed private‑capital crowd‑in as a priority, foreshadowing OSC’s later structures combining loans, equity, and demand guarantees [1][8].

April & October 2025 – Chinese Export Controls. In parallel, Beijing imposed and then escalated export controls on 12 rare earth elements and related processing technologies with direct defense applications, including dysprosium, terbium, and several others critical to permanent magnets [11]. Even after a limited mid‑2025 easing, exports of rare earth metals and compounds remained depressed, while finished magnet exports normalized, reinforcing China’s ability to set terms in upstream segments [11]. These moves hardened views in Washington that reshoring required more than offtake contracts—it required ownership and governance influence.

Late 2025 – Acquisition Transformation Strategy. In November 2025, the Department released an Acquisition Transformation Strategy that formally endorsed “public‑private partnerships” with “stable demand signals and the correct incentives” and explicit “risk sharing with industry” via enhanced Department participation in governance and returns structures [8]. The document called for collaboration with private equity and venture capital, and instituted “routine monitoring of performance against milestones” and commercialization progress for supported firms [8]. This institutionalized the equity playbook that had been developing ad hoc.

From Buyer to Investor: Transaction Wave (Late 2025 – Early 2026)

MP Materials – “Mine to Magnet” Backbone. In December 2025, MP Materials announced a “transformational public‑private partnership” with the DoD involving a multi‑billion‑dollar package of convertible preferred equity, warrants, loans, and price‑floor and offtake commitments running more than a decade [5]. MP’s Mountain Pass mine in California supplies over 10% of global rare earth oxides and is one of the only non‑Chinese rare earth ore producers in operation [19]. The deal positions DoD as MP’s largest shareholder and underwrites construction of a second U.S. magnet plant—dubbed the “10X Facility”—to bring total company magnet capacity to roughly 10,000 t per year by around 2028 [5]. Industry reporting places DoD’s equity component near $400 million, though exact figures are not publicly disclosed [1][5].

Vulcan Elements & ReElement – Scale‑up from Pilot to Mass Production. Around the same window, Vulcan Elements announced a $1.4 billion strategic partnership with the U.S. Government and ReElement Technologies [12][20]. The Department committed a $620 million direct loan for Vulcan’s magnet facility expansion, plus $80 million for ReElement’s recycling and processing capacity, while the Department of Commerce took $50 million in equity stakes; warrants to DoD added further upside [12][20]. Vulcan currently operates a ~10 t per year magnet facility in Durham, North Carolina and plans to scale to 10,000 t annually through the new plant [20]. The deal leverages an earlier offtake agreement between Vulcan and ReElement for light and heavy rare earth oxides [12].

USA Rare Earth – Hydrometallurgy and Heavy REEs. In January 2026, USA Rare Earth announced a non‑binding letter of intent from the Commerce Department’s CHIPS Program for a proposed $1.6 billion package: a $1.3 billion senior secured loan and $277 million in federal funding, in exchange for 16.1 million shares and roughly 17.6 million warrants [1]. The financing is keyed to operation of a hydromet demonstration plant in Colorado in early 2026, running five solvent‑extraction circuits for 2,000–4,000 hours targeting heavy rare earths such as dysprosium and terbium [1]. Successful demonstration is required to accelerate commercial production into late 2028, compressing timelines by roughly two years versus earlier plans [1].

Trilogy Metals – Direct Equity and Governance Rights. Also in late 2025, Trilogy Metals secured a $35.6 million DoD investment structured as direct equity: $17.8 million for 8,215,570 units (each one share plus three‑quarters of a 10‑year warrant), giving DoD approximately 10% ownership and the right to appoint a director for three years [13]. The warrants, priced at $0.01 per share, are exercisable only if the Ambler Road access project is completed, directly linking equity upside to project execution [13].

L3Harris Missile Solutions – Propulsion as a Financial Asset. In January 2026, the Pentagon announced a $1 billion convertible preferred investment in L3Harris Technologies’ Missile Solutions business [2][9]. Missile Solutions, built on L3Harris’s 2023 acquisition of Aerojet Rocketdyne, is a key supplier of solid rocket motors for systems such as PAC‑3, THAAD, Tomahawk, and Standard Missile [2][36]. The security automatically converts into common equity upon a planned H2 2026 IPO of Missile Solutions, making DoD the anchor investor and largest shareholder while L3Harris retains control [2][9]. Proceeds are earmarked for capacity expansion, facility modernization, and throughput increases on backlogged missile programs, and are paired with multi‑year procurement arrangements to provide demand certainty [2].

Portfolio Scope. Taken together, these and related transactions across MP Materials, USA Rare Earth, Vulcan/ReElement, Trilogy Metals, Korea Zinc, and L3Harris Missile Solutions amount to at least six equity or equity‑convertible deals totaling roughly $9.5 billion as of early 2026 [1][8]. A separate $9 billion expansion of DPA Title III authorities further enlarges the pool available for future equity‑like interventions [25]. The state is now a central capital provider, not just a customer.

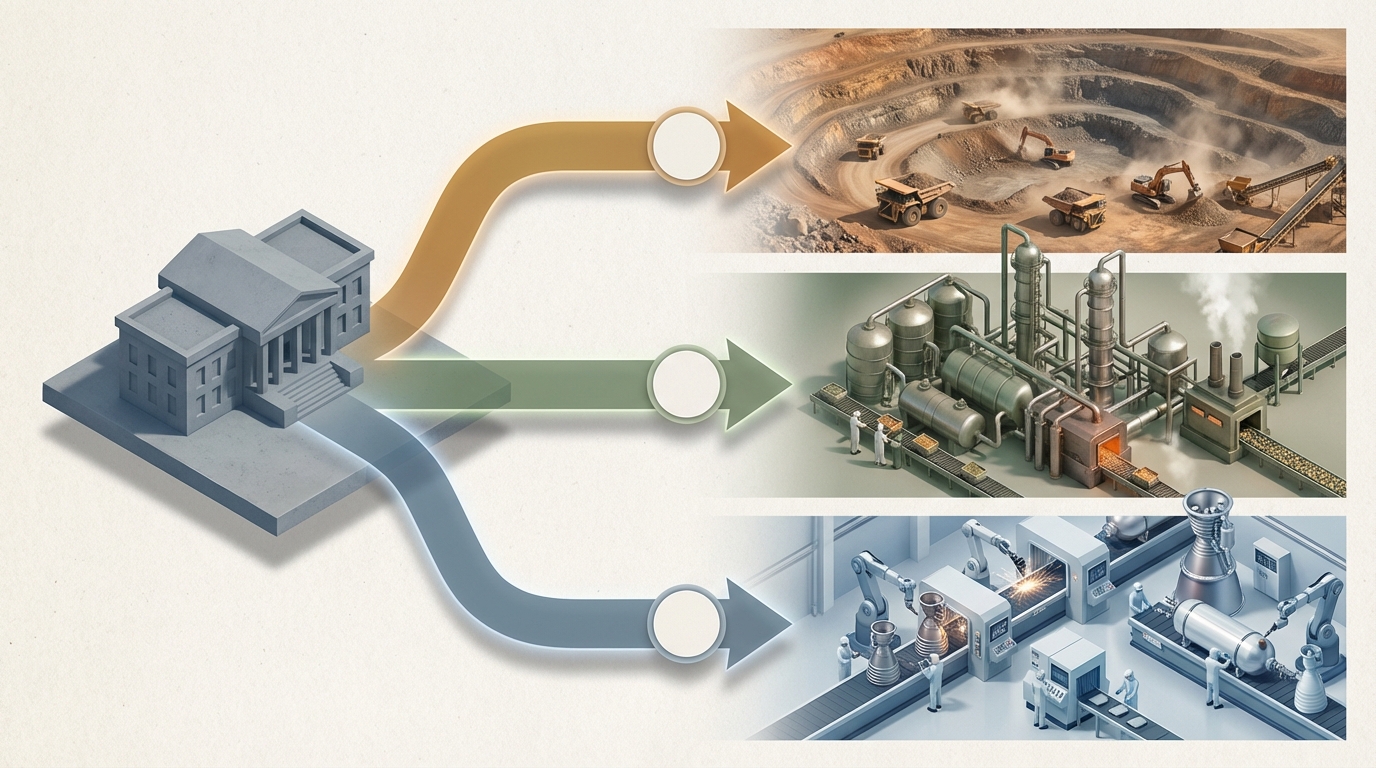

Isometric flow diagram showing government capital directed to mining, processing, and manufacturing sites.

Governance and Contracting Overlay (2026)

In January 2026, a new executive order titled “Prioritizing the Warfighter in Defense Contracting” directed DoD to incorporate performance triggers into future contracts, including restrictions on stock buybacks, dividends, and CEO compensation above $5 million during periods of under‑performance, non‑compliance, or insufficient production [3]. This reinforced the message that for mission‑critical suppliers—many now with DoD on the cap table—corporate governance and capital allocation are under closer scrutiny.

By March 2026, all major defense primes had raised 2026 capital expenditure guidance, several significantly so, a move contemporaneous with the new order’s implementation [3]. While causality is complex, the pattern suggests investors expect both higher demand and more active Pentagon involvement in investment decisions, especially where OSC and DPA funding are present.

Key Data & Trends

The emerging Pentagon equity portfolio is concentrated, strategic, and designed to close specific bottlenecks. Below we highlight quantitative patterns relevant for capital allocation and supply‑chain planning.

1. Federal Capital Concentration in a Few Critical Nodes

Federal equity and loan commitments are clustering in a small set of firms at the heart of rare earth magnets and missile propulsion [1][2][5][12][13][20].

Illustrative distribution of major DoD/Commerce commitments by company:

This concentration underscores why counterparties need detailed visibility into which suppliers have implicit or explicit government backstops. It also highlights crowding‑risk: private capital may be pulled toward DoD‑favored platforms, leaving other prospective projects capital constrained even if they are technically viable.

2. China’s Dominance in Heavy Rare Earths

DoD’s equity push is fundamentally a response to the scale of Chinese dominance in heavy rare earths [6].

With China controlling ~95% of global heavy rare earth output and supplying ~90% of U.S. heavy rare earth imports [6], any export restriction reverberates immediately through U.S. defense programs. The scale of this asymmetry explains why Washington is prepared to accept higher costs, increased state ownership, and governance entanglements to establish even partial domestic capacity.

3. U.S. Magnet Capacity: From Near‑Zero to Tens of Thousands of Tonnes

Domestic permanent magnet capacity is set for an order‑of‑magnitude expansion this decade if announced projects deliver [5][20].

Vulcan aims to move from a 10 tonne pilot to 10,000 tonnes annually; MP Materials’ 10X plan brings its U.S. magnet output toward a similar scale [5][20]. Even combined, this remains only a portion of total U.S. demand, but from a strategic perspective it creates a domestic floor of supply that cannot be sanctioned away. For OEMs, the key question is how much of this capacity will be reserved for defense versus commercial uses, and under what pricing structures.

4. From Capacity Payments to Equity and Convertible Structures

Transaction structures show a consistent pattern: blending senior debt with equity or equity‑linked instruments and long‑term offtake / price‑floor commitments [1][2][5][12][13]. USA Rare Earth’s package anchors a secured loan with shares and warrants; MP’s deal layers convertible preferred, warrants, and floor‑price offtake; Trilogy’s structure hard‑wires warrant value to project completion [1][5][13].

For procurement and finance teams, the “so what” is clear: government‑backed suppliers may have lower cost of capital and different risk appetites than peers. This can affect bidding behavior, willingness to invest ahead of contracts, and resilience under price pressure, reshaping competitive dynamics across mining, refining, and components.

5. Rapid Scaling of DPA/OSC Financial Deployment

The cumulative effect of the past 18 months is a step‑change in how much capital DoD deploys through financial channels rather than pure contracting [1][8][25].

Conceptual image of the Pentagon as an investor, combining the building with abstract shareholder motifs.

Between at least $9.5 billion in specific equity or equity‑convertible deals and a $9 billion DPA Title III expansion, total potential deployable capital exceeds $18 billion [1][8][25]. While not all of this will be drawn, the signal matters: for critical minerals developers and OEMs, alignment with DoD strategic priorities can now unlock quasi‑sovereign financing far beyond traditional cost‑sharing grants.

Risks & Scenarios

The Pentagon’s equity turn introduces a new risk landscape for defense and critical minerals stakeholders. Below we outline three scenarios with indicative probabilities and implications.

Scenario 1 – Managed Expansion (Base Case, ~60%)

Outline. DoD and partner agencies continue to deploy OSC and DPA authorities along the current trajectory. MP’s 10X facility, Vulcan’s expansion, and USA Rare Earth’s hydromet line reach mechanical completion broadly on schedule (2028±1 year) [1][5][20]. The L3Harris Missile Solutions IPO goes ahead in H2 2026 with DoD as a large but non‑controlling shareholder [2][9]. China maintains but does not dramatically escalate export controls [11].

Risks. Execution risk remains high: hydrometallurgy scale‑up failures, permitting delays (e.g., Ambler Road for Trilogy [13]), and cost overruns could force additional state capital or painful restructurings. Governance tensions may surface as DoD appointees push for mission‑driven decisions (e.g., prioritizing defense offtake at lower margins) that conflict with minority shareholders’ expectations. Yet systemic disruption is limited; procurement managers can rely on a growing, albeit still thin, domestic supplier base.

Implications. In this world, being inside the DoD equity “tent” is a durable advantage. Non‑backed projects face tougher capital markets and may become acquisition targets or adjuncts to the main DoD‑favored platforms. Price formation in magnets and certain missile systems will partially internalize state risk‑sharing—leading to more predictable but potentially structurally higher cost curves.

Scenario 2 – Stress and Politicization (Escalation, ~25%)

Outline. One or more major projects in the Pentagon portfolio misses technical or schedule milestones: hydromet demonstration underperforms at USA Rare Earth [1], magnet throughput at Vulcan lags nameplate [20], or L3Harris’s Missile Solutions faces IPO market pushback, delaying conversion of DoD’s preferred stake [2][9]. In parallel, Beijing tightens export controls further or introduces informal administrative barriers that squeeze non‑Chinese refiners [11]. Domestic political scrutiny of “industrial policy by equity stake” intensifies.

Risks. DoD is forced into visible capital calls, restructurings, or even de‑facto nationalizations of critical assets to preserve capacity, blurring the line between shareholder and regulator. Congressional oversight could respond with restrictive riders, slowing or freezing further OSC deployments. Private investors, seeing heightened political risk and uncertain exit pathways, price in higher required returns or shift capital elsewhere. Supply‑chain planners may face renewed fragility if a few over‑concentrated projects stumble.

Implications. This scenario amplifies governance risk. Counterparties to DoD‑backed firms must plan for scenarios where government priorities override commercial logic, including forced allocation of output to specific programs or price interventions. For firms outside the portfolio, opportunities may open to position as “politically neutral” alternatives—but without matching access to cheap capital.

Scenario 3 – Diversification and Normalization (Relief, ~15%)

Outline. Technological and market developments diffuse risk: successful hydromet processes at USA Rare Earth [1] and Trilogy’s project [13] are replicated by additional developers; allied producers in Europe and Asia expand capacity; recycling (e.g., ReElement) scales more rapidly than expected [12][20]. China adopts a more pragmatic posture, keeping export controls in place but administering them less aggressively [11]. Politically, a cross‑party consensus emerges favoring time‑limited, performance‑linked state equity stakes that sunset as projects mature.

Risks. The main risk here is complacency: policymakers could misread an improved short‑term supply picture as structural security and prematurely unwind support before a diverse supplier base is fully established. Private investors may demand clearer signals on state exit timelines before recommitting capital to the sector.

Implications. Equity stakes begin to look more like catalytic bridge financing than permanent governance arrangements. For operators, this would mean greater emphasis on meeting performance milestones that trigger state exit and a gradual reversion to more conventional supplier–buyer relationships. However, given the time horizons of mining and processing, any such normalization is unlikely before the early 2030s.

Risk Matrix (Qualitative)

Supply security risk: High now; moderate in Scenario 1; spikes in Scenario 2; moderates in Scenario 3.

Governance/political risk: Structural and rising under all scenarios, highest in Scenario 2.

The Pentagon’s equity play changes how defense suppliers, miners, and investors should plan. Below are concrete actions by time horizon.

Do Now (Next 4–6 Weeks)

Map portfolio and supply‑chain touchpoints.

Owner: Strategy / Supply Chain leads.

Action: Build an internal registry of exposure to MP Materials, USA Rare Earth, Vulcan/ReElement, Trilogy Metals, Korea Zinc, and L3Harris Missile Solutions—both as suppliers and as JV/portfolio positions [1][2][5][12][13][20]. Flag where DoD equity or board representation is present.

Review contract and governance clauses.

Owner: Legal / Contracts.

Action: For entities dealing with DoD‑backed firms, review change‑of‑control, state‑aid, and information‑sharing clauses. Where DoD has board rights (e.g., Trilogy [13]) or is expected to become a major shareholder (MP, L3Harris Missile Solutions [2][5][9]), assess whether contractual protections need updating.

Integrate OSC/DPA criteria into project design.

Owner: Mining and processing project developers.

Action: Align feasibility studies and investment cases with DPA Section 303 and OSC’s stated criteria: contribution to national security, technology readiness, co‑investment from private capital, and clear commercialization milestones [1][8][25]. Position projects for upcoming DPA Title III solicitations.

Do in the Next 2–3 Quarters

Scenario‑plan DoD as shareholder across tiers.

Owner: CFO / Corporate Development.

Action: For primes and major subsystem suppliers, model how DoD ownership in key upstream nodes (magnets, motors) could influence pricing, volume allocation, and technology roadmaps. Consider both favorable (stable offtake) and adverse (priority allocation away from you) scenarios.

Explore co‑investment or partnership structures.

Owner: Strategy / Business Development.

Action: For investors and industrials, evaluate minority positions alongside DoD/OSC in magnet, hydromet, or recycling projects, treating the state as an anchor LP. Focus on structures where governance rights and exit pathways are clearly defined to avoid being subordinated to non‑commercial priorities.

Re‑assess sourcing diversification strategy.

Owner: Supply Chain / Procurement.

Action: Rebalance sourcing matrices to include both DoD‑backed and independent suppliers where technically feasible. For critical inputs like high‑coercivity magnets and heavy rare earth oxides, identify at least one non‑DoD‑backed alternative per component if available, to mitigate concentration risk.

Positioning for 2026–2030

Design capital structure for policy durability.

Owner: CEOs / Boards of mining and processing firms.

Action: Structure future financings so that state equity stakes are either clearly time‑bounded or paired with sunset / buy‑back mechanisms tied to performance milestones. This mitigates the risk of permanent politicization and may make projects more attractive to institutional investors.

Build technology options beyond current DoD bets.

Owner: CTO / R&D.

Action: Invest in alternative technologies that could de‑risk current dependencies: magnet chemistries with reduced dysprosium/terbium content, motor designs less reliant on rare earths, or improved recycling yields [1][6][12][20]. Position to benefit if policy shifts away from today’s chosen assets or if those assets underperform.

Institutionalize political‑risk and governance monitoring.

Owner: Risk / Government Affairs.

Action: Treat DoD equity involvement as an ongoing political‑risk exposure. Establish regular reviews of executive orders, DPA/OSC guidance, and congressional oversight trends [3][8][25][26]. Integrate these into capital allocation and M&A decisions, particularly for assets in the Pentagon’s orbit.

Signals to Watch

Monitoring a few concrete indicators can provide early warning of shifts in the Pentagon’s equity strategy and its impact on critical minerals and defense supply chains.

L3Harris Missile Solutions IPO timing and structure.

Signal: Confirmation, delay, or downsizing of the planned H2 2026 IPO and any changes in DoD’s conversion terms [2][9].

Why it matters: A bellwether for investor appetite for DoD‑backed equity stories and for the durability of the convertible‑preferred model.

USA Rare Earth hydromet demonstration performance.

Signal: Public reporting on runtime hours achieved, throughput, and separation efficiencies at the Colorado demonstration facility [1].

Why it matters: Underpins the feasibility of U.S. heavy rare earth separation; under‑performance would ripple through supply plans and financing.

Progress on key enabling infrastructure (e.g., Ambler Road).

Signal: Regulatory and legal milestones on projects linked to Trilogy Metals’ assets [13].

Why it matters: Trilogy’s warrant structure only pays off if Ambler Road is completed, making it a test case for how DoD handles contingent equity tied to politically contentious infrastructure.

Chinese export control adjustments.

Signal: New or modified controls on rare earth elements, processing technologies, or magnet exports from China [11].

Why it matters: Any tightening will validate the Pentagon’s reshoring strategy and could trigger accelerated or expanded equity interventions.

DPA Title III and OSC solicitation cadence.

Signal: Frequency, size, and sector focus of new solicitations or awards under DPA Section 303 and OSC programs [8][25].

Why it matters: Indicates whether the current equity push will broaden beyond today’s portfolio or consolidate around existing champions.

Sources

[1] Public disclosures and company statements regarding USA Rare Earth CHIPS Program letter of intent and associated federal financing package.

[2] Department of Defense and L3Harris announcements detailing the $1 billion convertible preferred investment in Missile Solutions and planned IPO structure.

Geographic distribution of Pentagon equity investments across mining, processing, and manufacturing sites.

[3] Executive order “Prioritizing the Warfighter in Defense Contracting” and subsequent reporting on defense prime capital expenditure guidance.

[5] MP Materials corporate communications on the “transformational” public‑private partnership with DoD, including financing structure and 10X magnet facility plans.

[6] Assistant Secretary of War testimony on Chinese control of heavy rare earth output and U.S. import dependence.

[8] Department of Defense Acquisition Transformation Strategy and related Office of Strategic Capital materials describing investment frameworks and monitoring protocols.

[9] Investor presentations and filings outlining the L3Harris Missile Solutions spinoff, DoD’s anchor investor role, and H2 2026 IPO timing.

[10] U.S. government assessments quantifying net‑import reliance for critical minerals.

[11] Chinese government notices and trade data analyses on 2025 export controls covering rare earth elements, processing technologies, and related products.

[12] Vulcan Elements and ReElement Technologies announcements on the strategic partnership with DoD and Department of Commerce, including loan and warrant terms.

[13] Trilogy Metals news releases and filings on the $35.6 million DoD equity investment, warrant terms, and board appointment rights.

[16] MP Materials location announcement for the 10X magnet facility in Northlake, Texas, including planned investment and employment figures.

[19] MP Materials disclosures on Mountain Pass mine production and share of global rare earth oxide supply.

[20] Vulcan Elements materials describing current and planned magnet production capacities at the Durham facility and expansion project.

[24] U.S. geological and critical minerals strategy documents on import dependence across key commodities.

[25] Executive order on “Immediate Measures to Increase American Mineral Production” and documentation of the $9 billion Defense Production Act Title III expansion.

[26] Executive order on “Modernizing Defense Acquisitions and Spurring Innovation in the Defense Industrial Base.”

[36] L3Harris corporate filings and press releases related to the 2023 acquisition of Aerojet Rocketdyne and integration into Missile Solutions.

**Australia is coupling a price‑banded national critical minerals reserve with sovereign equity in projects like Arafura’s Nolans and the VHM-Shenghe break at Goschen, reshaping how rare earths, gallium, and antimony are financed, processed, and contracted outside China.**

Australia Breaks the Chinese Offtake Model: Critical Minerals Sovereignty as Industrial Infrastructure

Australia is moving from being a raw material supplier into building a tightly engineered sovereignty system for critical minerals. The emerging architecture combines three levers: a national reserve for rare earths, gallium, and antimony with guaranteed price bands; the termination of Chinese offtake exposure at assets like VHM’s Goschen project; and sovereign equity via the National Reconstruction Fund’s (NRF) reported $200 million commitment to Arafura Rare Earths’ Nolans project.

The operational question is straightforward but profound: can a state-backed price floor and ceiling regime, coupled with state equity in processing, deliver reliable, non‑Chinese supply without locking miners and end users into another form of structural dependence? The answer will be determined less by high‑level strategy statements than by the way contracts, plant designs, and logistics are being re‑engineered around this new model.

For mining companies, refiners, trade policymakers, and supply chain strategists, the critical detail is not that Australia is stockpiling metals. It is that Canberra is deliberately inserting itself into the offtake stack: as buyer of last resort, source of price stabilization, and co‑owner of midstream processing. That combination changes how projects are banked, how plants are configured, and which specification sheets ultimately dominate the non‑Chinese market.

The Architecture of Australia’s National Critical Minerals Reserve

Australia’s critical minerals strategy has moved from concept papers to an emerging operational structure in which a national reserve plays a central role. Public statements and policy documents indicate a clear focus on three groups of materials: rare earths (with an emphasis on magnet materials like NdPr), gallium, and antimony. All three are metals where China currently dominates processing and downstream trade, and where export controls or informal quotas have already been deployed as policy tools.

The reserve concept departs from traditional, passive stockpiling. Instead, it is being framed as an active stabilization mechanism: government entities stand ready to buy when prices fall below a defined floor and to release stock into the market when prices exceed a defined ceiling. In practice, that creates a band around a reference price, within which normal market trading is expected to occur with reduced volatility.

Administratively, the reserve is being woven into existing critical minerals institutions. The National Reconstruction Fund, with its multi‑billion‑dollar mandate for industrial transformation, is a core funding vehicle. Implementation touches the Critical Minerals Office and the Department of Industry, Science and Resources, which oversee project qualification, ESG criteria, and domestic value‑add thresholds. Rather than simply funding mines, the system targets projects that integrate extraction and refining within Australia or allied jurisdictions.

From a technical standpoint, this model turns the reserve into a quasi‑industrial customer. It will specify minimum product types and purity levels that can be accepted into the stockpile. For rare earths, that likely means separated oxides (particularly NdPr oxide and potentially didymium blends) rather than mixed concentrates. For gallium, high‑purity metal suitable for semiconductor precursor production. For antimony, refined metal or trioxide meeting alloy and flame‑retardant specifications. That technical granularity matters because it forces upstream projects to design flowsheets and quality control systems around the targeted reserve products.

Price Floors and Ceilings: How the Band Changes Project Risk

The price‑band mechanism is the real structural innovation. Traditional mining offtakes often embed discounts to volatile spot benchmarks, leaving projects heavily exposed to cyclical troughs. China’s ability to flood or constrict export volumes in rare earths, gallium, and antimony has historically turned that cyclicality into a strategic weapon. Australia’s reserve seeks to blunt that instrument by offering a transparent, rules‑based band in which sovereign purchases and releases smooth extremes.

In broad design, the floor is anchored to multi‑year average prices or cost‑based benchmarks, with an allowance for volatility. When market prices fall substantially below that anchor, reserve managers can offer to purchase qualifying material at or near the floor, subject to volume limits and compliance criteria. The ceiling works in mirror fashion: when prices materially overshoot the anchor, material from the reserve can be offered into the market, again under defined conditions, to relieve tightness.

Technically, this turns the sovereign into a large, rules‑driven counter‑cyclical trader. That role is operationally demanding. It requires:

Transparent reference pricing, derived from a mix of exchange data, published assessments, and bilateral contract benchmarks.

Robust assays and certification systems to ensure that purchased materials meet reserve specifications, particularly for multi‑element streams such as rare earth oxide mixes.

Storage infrastructure for corrosive or reactive materials (e.g., antimony trioxide) that complies with environmental and safety regulations over multi‑year horizons.

Mechanisms to rotate stock, reprocess where necessary, and avoid degradation or obsolescence against evolving downstream specifications.

From the project perspective, the presence of an accessible floor reduces the probability of “price‑floor‑breach” scenarios in loan models and internal risk cases. Life‑of‑mine plans can be calibrated around a narrower downside band. That does not eliminate market risk; it channels it. The trade‑off is clear: upside capture may be moderated when ceilings trigger, but catastrophic downside, especially from politically induced dumping, becomes less likely.