Dissecting Top 12 China-Independent Critical Mineral Narratives: Supply Risk vs Reality

Key Takeaways

- China retains integrated control over 60–90% of rare earth mining and refining, including heavy rare earth elements (HREEs).

- Non-Chinese projects face permitting delays, higher costs, and ESG constraints that extend timelines by 5–7 years.

- Resource diversification alone does not equal processing independence; offtake contracts and mid-stream choke points matter.

- Projects like Mountain Pass and Lynas Texas advance resilience but cover only fractional shares of global demand.

- Robust mapping of financing, processing routes, and regulatory friction points is essential for genuine supply security.

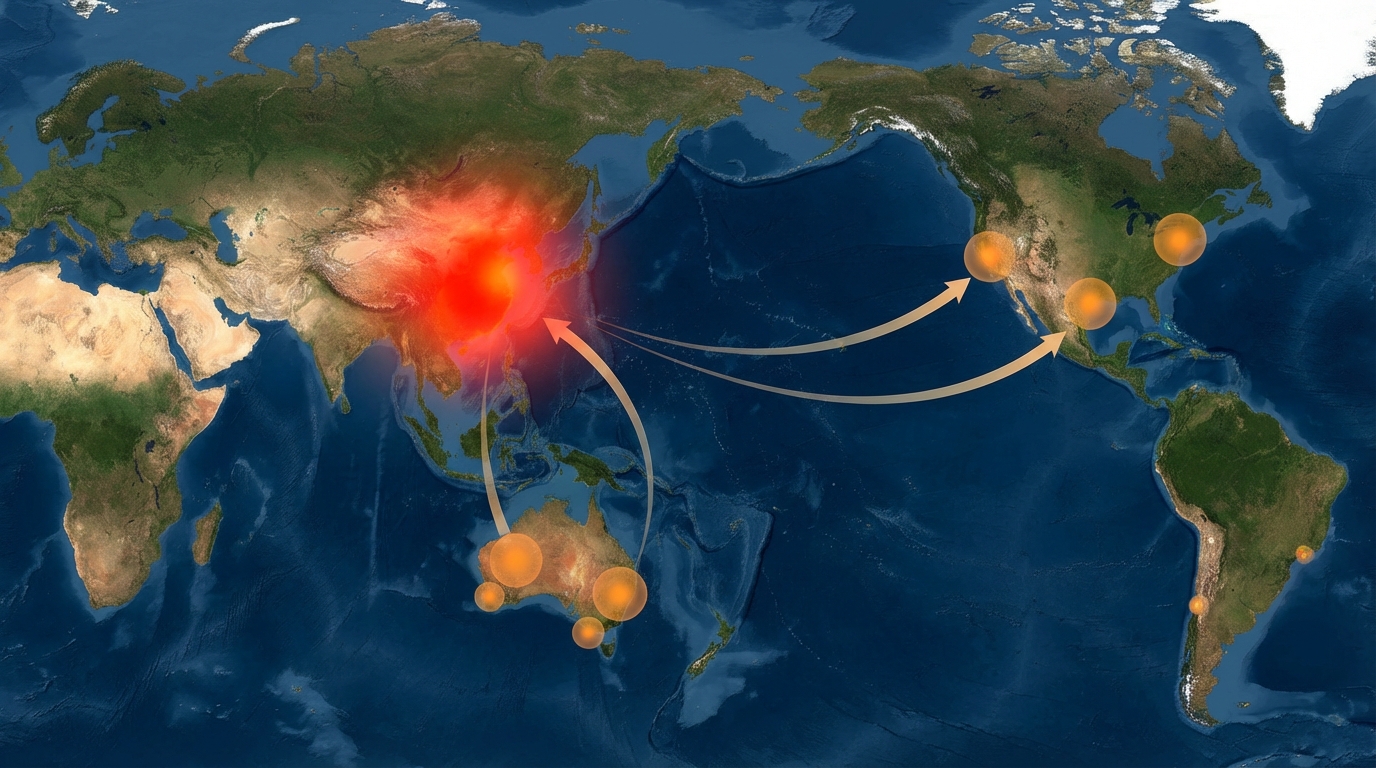

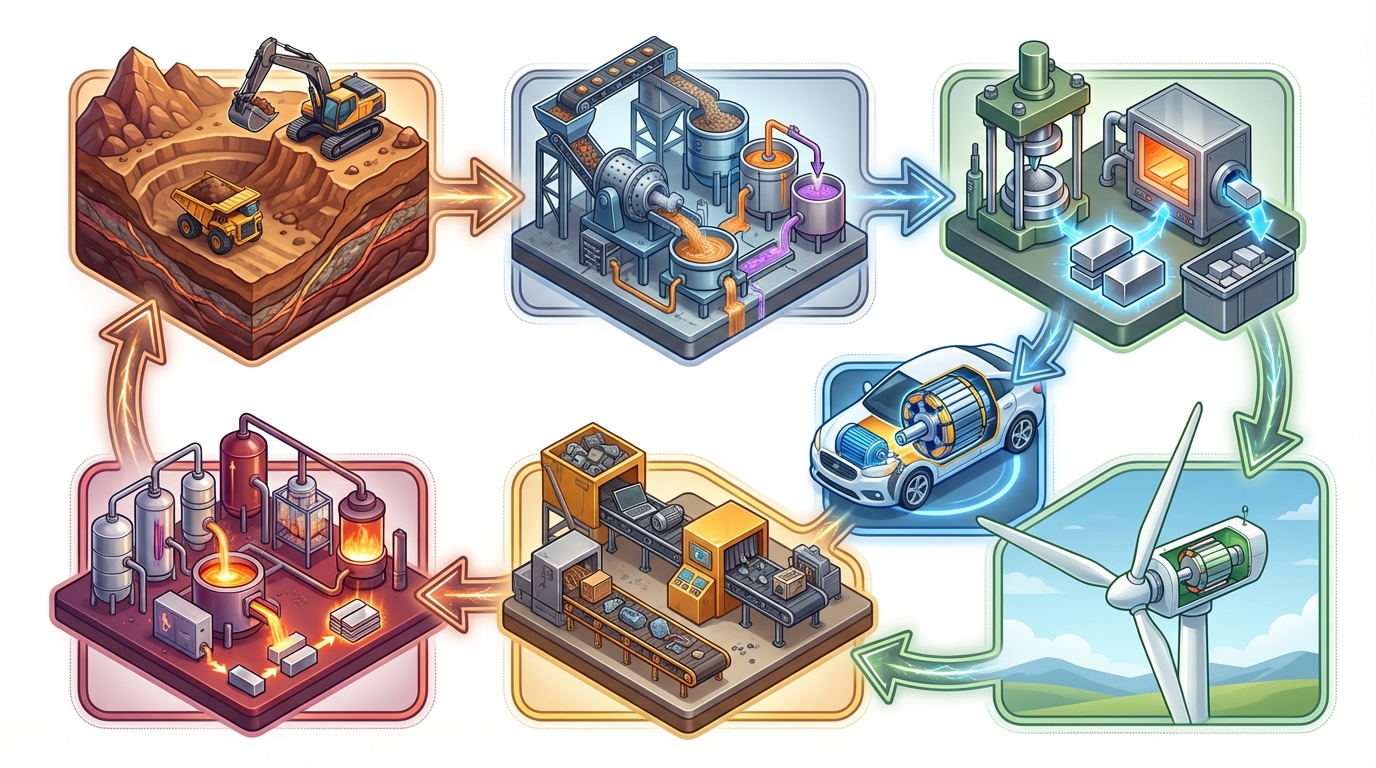

Across defense, EV, wind, and advanced electronics supply chains, strategic planners hear promises of rapid transition to “China-independent” critical mineral supply. Rare earths encompass light rare earth elements (LREEs) such as neodymium (Nd) and praseodymium (Pr), and heavy rare earth elements (HREEs) including dysprosium (Dy) and terbium (Tb). Total rare earth oxides (TREO) denote the combined oxides of all 17 lanthanides plus yttrium. Materials Dispatch’s review of 2024-2025 project data, trade flows, and ownership structures reveals a harsher reality: China still controls roughly 60–90% of rare earth mining and refining capacity and dominates HREE supply.

This briefing ranks the top 12 “China-independent” narratives by their strategic distance from reality. We contrast public storylines with operational details—contract terms, logistics, processing routes, and observed failure modes. The goal is to calibrate expectations and highlight the real levers that move supply risk.

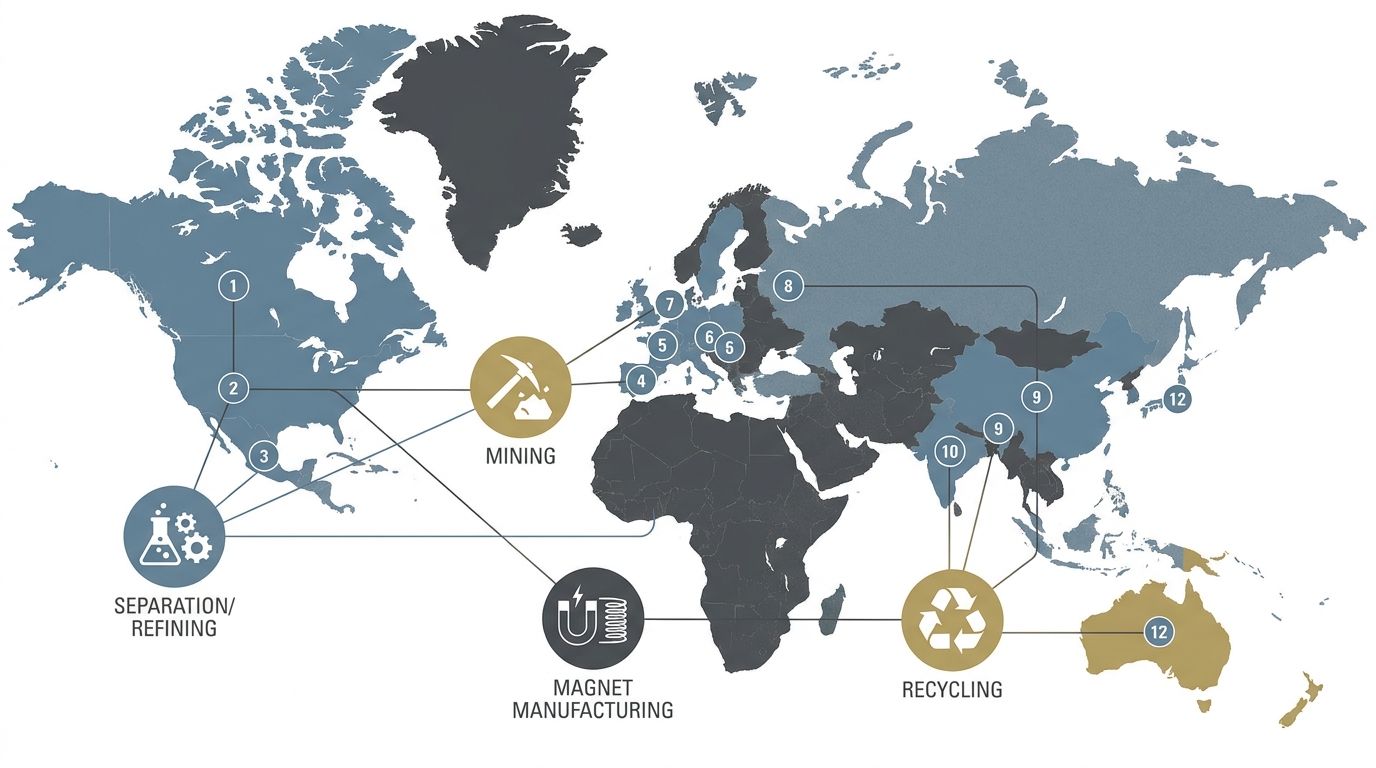

1. US Mountain Pass Mine as a Fully Domestic “Mine-to-Magnet” Solution

The Asset / Risk. Mountain Pass in California is often introduced in official speeches as the linchpin of a sovereign US rare earth supply chain: mine, refine, and manufacture NdFeB magnets on US soil. The mine produces 40,000–60,000 MT/year of TREO concentrate, heavily weighted to LREEs such as Nd and Pr.

Strategic Context. For US defense platforms and EV drive motors, Mountain Pass anchors domestic mining know-how and signals U.S. progress toward China’s magnet ecosystem. The plan to add domestic separation and magnet production is framed as the final step to full independence.

The Bottleneck. On the ground, nearly 100% of concentrate still ships to China for separation. HREE separation (Dy, Tb) remains a critical gap. Scaling solvent-extraction circuits under US environmental and labor constraints is slower and costlier than in China. Even at a planned 1,000 MT/year NdFeB capacity—<1% of China’s 138,000 MT in 2018—the facility depends on power, skilled labor, and steady capex. Permitting delays have stretched timelines beyond initial guidance, and any regulatory hiccup in waste or water management triggers fresh reviews.

The Verdict. Mountain Pass enhances upstream resilience for LREEs and provides a partial hedge against raw-material shocks. It does not deliver a closed-loop, China-independent chain in the 2025–2030 window. Risk assessments should track domestic separation commissioning, long-term power contracts, and residual reliance on Chinese reagents or offtake partners.

2. Australia’s Nolans Project as an Allied HREE Independence Engine

The Asset / Risk. The Nolans project in Australia’s Northern Territory is positioned as an “ally-only” source of RE oxides, with integrated mining and processing to bypass China. Public messaging often blurs its primary LREE focus (NdPr) with the scarcer HREEs needed for defense and offshore wind magnet temperature performance.

Strategic Context. For OEMs in Japan, Europe, and North America, a stable NdPr source in Australia supports diversification. Government support and offtake agreements with non-Chinese customers reinforce the impression of a clean break from China’s dominance.

The Bottleneck. By mid-2020s, Nolans remained in advanced development, with construction and commissioning repeatedly delayed by environmental approvals, workforce constraints, and cost inflation. HREE volumes are modest relative to global deficits. Remote logistics, port capacity limits, and minority-stake approaches from Chinese-linked entities underscore challenges in fully divorcing from China’s processing ecosystem.

The Verdict. Nolans adds medium-term value for LREE diversification but is not a turnkey HREE solution. Planners should monitor final financing, offtaker identities, and any toll-separation routing through Asian hubs.

3. Brazil’s Serra Verde as a Non-Asian Light + Heavy REE Powerhouse

The Asset / Risk. Serra Verde in Goiás, Brazil, is promoted as the first major ionic-clay REE mine outside Asia, offering both LREE and meaningful HREE output. Ionic clays can be leached at relatively low cost, with lower-carbon profiles versus Chinese or Myanmar clays.

Strategic Context. Multinational OEMs value jurisdictional diversification and mixed LREE/HREE output for EV motors, offshore wind, and industrial catalysts.

The Bottleneck. Early offtake deals defaulted to Chinese processors due to scale and installed capacity. Brazilian environmental regulations and tailings management add compliance costs and delays. Labor disputes and port congestion create unpredictable export flows.

The Verdict. Serra Verde diversifies the resource base but not processing control. Procurement teams should scrutinize offtake contracts, potential redirection to non-Chinese processors, and Brazilian regulatory shifts.

4. Aclara’s Latin American Projects as ESG-Perfect, Fully Western Chains

The Asset / Risk. Aclara’s ionic-clay projects in Chile and Latin America are marketed on strong ESG credentials—closed-loop water use and ion-exchange technology feeding a planned US separation hub.

Strategic Context. A low-impact Latin American resource plus US processing facility would showcase allied industrial cooperation for defense and EV magnet supply chains under ESG pressure.

The Bottleneck. Scaling ion-exchange from pilot to commercial scale poses throughput, resin-degradation, and water-quality challenges. US separation permitting under NEPA and local zoning can extend to five–ten years. Financing must tolerate schedule creep and evolving regulatory requirements around PFAS and waste.

The Verdict. Aclara offers a credible late-decade HREE pathway but remains aspirational for the 2020s. Its value hinges on firm offtake contracts, social license in Latin America, and US regulatory progress.

5. US Recycling (Vulcan, ReElement and Peers) as a Leapfrog over Mining

The Asset / Risk. US recycling ventures backed by defense funding promise to recover several thousand tonnes per year of RE oxides from e-waste and industrial scrap, framed as a way to “skip” upstream mining.

Strategic Context. Onshore recycling aligns with security-of-supply mandates and ESG goals, offering potential to flatten HREE price volatility if mine development lags.

The Bottleneck. Limited and fragmented REE-bearing scrap streams, purity and consistency challenges, and pilot-scale facilities with 12–24 month ramp-ups restrict near-term impact. Recovered purity (high-80s to low-90s%) often falls short of virgin-like specs, necessitating additional purification.

The Verdict. Recycling can offset 10–20% of rare earth needs in niche segments, especially defense. It is not a structural replacement for mining this decade. Track scrap-supply agreements, military qualification of recycled materials, and hazardous-waste regulations.

6. Greenland’s Kvanefjeld and Tanbreez as an Arctic HREE Safety Valve

The Asset / Risk. Greenland’s Kvanefjeld and Tanbreez deposits are invoked as potential sources of 20–25% of global HREE needs under Danish oversight.

Strategic Context. NATO planners cite geopolitical alignment and Arctic shipping proximity as advantages for HREE supply.

The Bottleneck. Projects are stalled by uranium restrictions, permafrost engineering challenges, seasonal shipping windows, and local opposition. Arctic conditions triple logistics costs versus temperate ports.

The Verdict. Greenland remains a strategic option, not an active mid-decade contributor. Model it as upside contingent on regulatory shifts, waste-management innovation, and Arctic infrastructure progress.

7. Canada’s Nechalacho as an Ethical HREE Cornerstone for North America

The Asset / Risk. Nechalacho in Canada’s Northwest Territories is promoted for “ethical” REEs from a high-standards jurisdiction, with small open-pit production and nearby processing.

Strategic Context. Fits USMCA rules-of-origin and ESG reporting; validates modular mining and initial processing in remote environments.

The Bottleneck. Scale remains modest (hundreds of tonnes/year), with full separation via toll processing in Europe. Sub-arctic conditions limit operating days and raise logistics costs. Major expansion requires lengthy permitting and community consultation.

The Verdict. Nechalacho is a high-integrity, low-volume node in the North American REE network. Watch moves toward onshore separation, remote power solutions, and Indigenous royalty frameworks.

8. Tanzania’s Ngualla (Peak Rare Earths) as a “Western-Controlled” African Supply

The Asset / Risk. Ngualla was cited as a Western-developed African resource with high TREO grades, poised to supply magnet materials free of Chinese influence.

Strategic Context. African sourcing appeals to OEMs seeking diversification, with Tanzania courting foreign investment and value-addition.

The Bottleneck. Ownership shifted to a Chinese-linked company, undermining the “Western-controlled” narrative. Tanzanian local-content rules and export levies add fiscal complexity. Grid instability and infrastructure gaps drive up capex and schedule risk.

The Verdict. Ngualla remains geologically attractive but no longer advances Western supply security. Treat it as a contributor to global tonnage, not a diversification win. Monitor Tanzanian policy, offtake structures, and parallel non-Chinese processing lines.

9. Lynas’ Texas Facility as the End of US Processing Dependence

The Asset / Risk. The DoD-supported Lynas plant in Texas is presented as closing the US loop for NdPr and select HREE processing under US law.

Strategic Context. “Kalgoorlie → Texas” is marketed as a clean, ally-controlled chain for defense-critical components.

The Bottleneck. Stricter US emissions and wastewater rules, community engagement, and technical scale-up challenges have stretched schedules and costs. Initial capacity covers only a fraction of US demand; HREE capability phases in slowly.

The Verdict. The Texas facility is a concrete step toward non-Chinese mid-stream capability, but it addresses only a slice of US needs. Track recovery rates, residue handling, permitting challenges, and energy-water agreements.

10. South African PGMs as a Platinum/Palladium Buffer against China

The Asset / Risk. South African platinum group metals (PGMs) underpin catalysis, hydrogen technologies, and high-temperature industrial processes. Mines in the Bushveld Complex supply dominant shares of global Pt, Pd, and Rhodium.

Strategic Context. Anchoring PGM sourcing in South Africa reduces Russian risk and appears to limit Chinese influence.

The Bottleneck. Chronic power shortages and load-shedding at Eskom, labor stoppages, and outsourced smelting/fabrication often involve Chinese intermediaries. Downstream dependencies on Chinese fabricators persist.

The Verdict. South African PGMs mitigate Russian exposure but not fully Chinese pricing power. Key levers: captive power investments, non-Chinese offtake contracts, and alternative fabrication hubs.

11. Myanmar’s Ionic Clays as a Non-Chinese Heavy REE Source

The Asset / Risk. Myanmar’s southern ionic-clay deposits mirror geological profiles of southern Chinese clays and are cited as an HREE diversification lever.

Strategic Context. Proximity to ports and existing mining experience suggest a second major clay district outside China.

The Bottleneck. Chinese firms finance and operate most mines; nearly all material flows into China for leaching and separation. Political instability, conflict, and sanctions risk hinder direct Western engagement.

The Verdict. Myanmar does not function as an independent HREE source. Treat its output as vulnerable to Chinese export policy and local instability. Monitor border closures, sanctions shifts, and any credible non-Chinese processing initiatives.

12. Sweden’s Norra Kärr as the EU’s Route to Rare Earth Autonomy

The Asset / Risk. Norra Kärr in Sweden is promoted by the European Commission as a cornerstone of EU strategic autonomy in REEs, with proximity to industrial hubs and strong legal frameworks.

Strategic Context. A domestic ore body supports EU EV, wind, and defense industries within stringent environmental and social standards.

The Bottleneck. Early-stage permitting faces local opposition over water impacts, biodiversity, and reindeer herding. Europe lacks commercial-scale separation capacity, requiring new plants subject to lengthy approvals or reliance on Asian processors.

The Verdict. Norra Kärr is a strategic option, not assured supply by 2030. Progress depends on permitting outcomes, committed financing, and parallel EU mid-stream infrastructure development.

Conclusion: Strategic Implications for Critical Mineral Security

Materials Dispatch’s analysis underscores that non-Chinese ore production, while necessary, does not alone secure supply chains. Genuine diversification demands parallel development of separation, alloying, and recycling capacity, aligned with realistic permitting and financing timelines. Industrial and defense stakeholders must track financing structures, mid-stream dependencies, and regulatory milestones to translate these options into actionable resilience. Only through disciplined governance and transparent industrial strategy can true China-independence be approached.