Why this debate matters for OEMs now

Materials Dispatch approaches critical materials not as an abstract geopolitical topic, but as a daily operational constraint for automotive, defense, electronics, and industrial OEMs. Over the last decade, the firm has watched multiple supply shocks – from the 2010 rare earths dispute and COVID-era logistics breakdowns to Russia-related disruptions in nickel, palladium, and neon – translate directly into halted production lines, emergency sourcing at any quality, and bruising internal audits on risk governance.

In that context, stockpiling has become the instinctive response. Boards ask for buffer days of inventory; procurement teams build “strategic reserves”; public agencies launch shared storage schemes. The reflex is understandable: inventories are visible, easy to explain, and can be booked as a concrete risk-management line item. Yet recent policy moves – Chinese export controls on gallium, germanium, and graphite, tightening sanctions regimes, emerging EU cyber and ESG rules on mining, and talk of new tariffs on refined metals – have made one conclusion inescapable for this publication: stockpiling alone is structurally misaligned with the way the next shock is likely to unfold.

The next materials crisis will be driven less by sheer tonnage scarcity and more by policy decisions on where refining happens, who is allowed to export, and which upstream assets can keep operating under regulatory and cyber pressure. Stockpiles can buy time; they cannot fix that geometry.

Key points

- Stockpiling provides a tactical buffer but does not address structural exposure to concentrated refining, export controls, and regulatory shutdown risks.

- Critical materials refining remains heavily centered in China for rare earths, battery inputs, and several strategic metals, limiting the effectiveness of any downstream inventory buffer.

- Public and private stockpile schemes increasingly intersect with tariffs, export controls, and cybersecurity rules, creating complex compliance and replenishment obligations.

- Diversified non-Chinese mining and refining projects, along with magnet, battery, and wiring redesign, could materially reshape exposure, but timelines are measured in years, not quarters.

- Interpreting upcoming policy milestones and project FIDs correctly is likely to matter more than any single warehouse volume in determining OEM resilience.

FACTS: Structural exposure, stockpiling responses, and the emerging project map

Concentrated refining and structural tightness

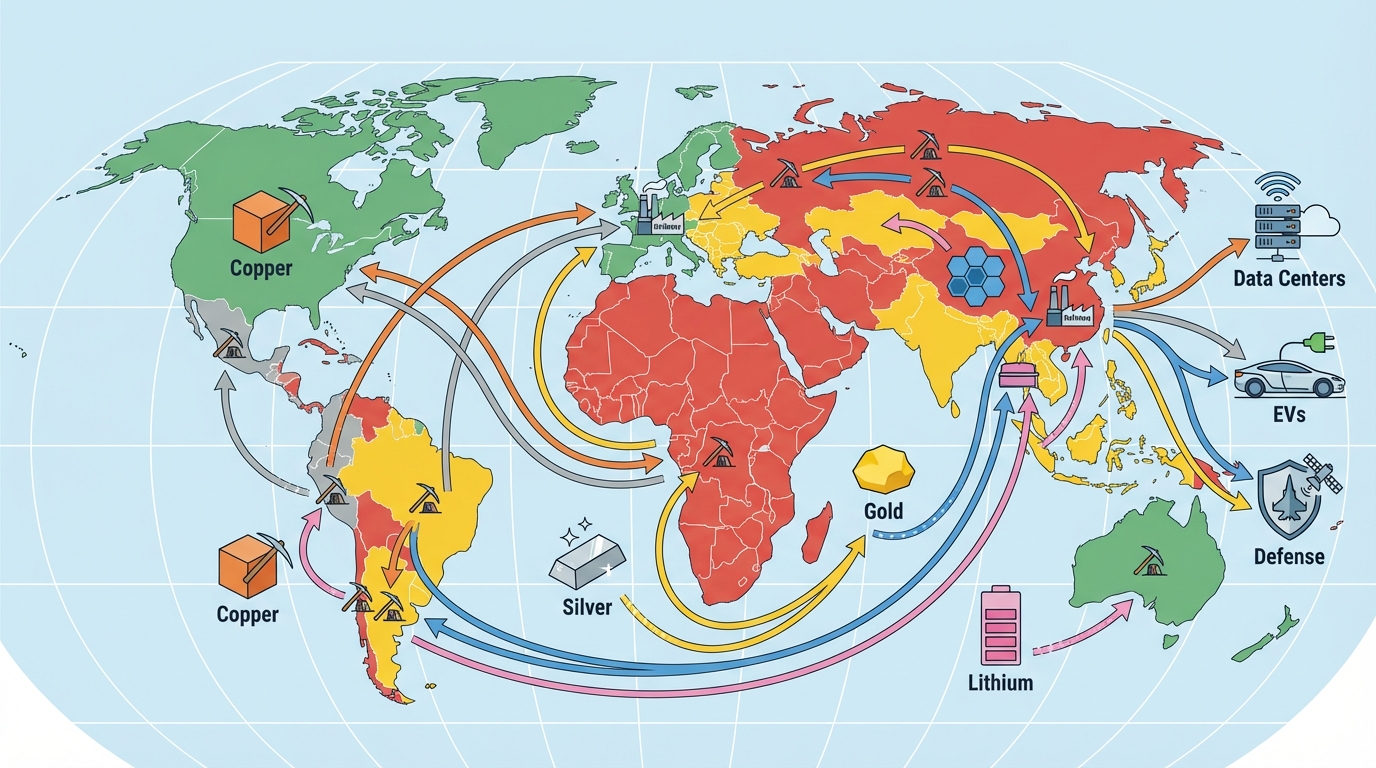

Several converging facts define the baseline. First, refining and separation for many strategic and energy-transition materials are geographically concentrated. For key rare earth oxides used in permanent magnets, China has controlled the dominant share of global separation capacity for years. Similar patterns hold for segments of the graphite, lithium chemicals, and cobalt refining chains. For OEMs that rely on neodymium-iron-boron magnets, high-purity graphite, or cobalt-bearing battery chemistries, the “single point of refining” problem is already visible in supplier mapping exercises.

Second, multiple technical agencies and industry groups have flagged potential medium-term deficits in refined copper and certain battery materials in North America and Europe, driven by electrification, data center buildout, and defense demand. In copper, projections for the mid-2020s point to a refined deficit in the United States measured in the hundreds of thousands of tonnes on an annual basis if new smelting and refining capacity does not accelerate. For rare earths, various analyses have highlighted a potential mismatch between projected demand for neodymium and dysprosium in EV motors and wind turbines and committed non-Chinese capacity.

Third, policy tools have shifted decisively from rhetoric to implementation. China has implemented export controls on gallium, germanium, and certain graphite products, explicitly linking export permissions to national security concerns. The United States, European Union, Japan, and others have deployed sanctions, tariffs, and industrial subsidies directly targeted at reshaping critical materials supply chains. EU rules such as the Carbon Border Adjustment Mechanism (CBAM) and the NIS2 Directive extend climate and cyber obligations upstream into metals and mining, including operators of rare earth and battery-metal facilities.

How stockpiling has been structured so far

Stockpiling is not new. The United States has operated some form of strategic materials stockpile since the mid-20th century, and Japan’s post-2010 rare earth strategy prominently featured government-coordinated inventories. OEMs in automotive and defense have, over the last decade, built their own refined metal and component buffers, typically measured in weeks or a few months of normal consumption.

Recent years have added new institutional forms. Public–private vehicles have emerged where commodity traders, OEMs, and export credit agencies co-finance shared pools of strategic metals. These schemes typically define a list of eligible materials (often aligned with national “critical minerals” lists), set trigger conditions for drawdowns (for example, formal export bans or sustained benchmark-price spikes), and allocate replenishment obligations among participating parties. From a governance standpoint, they sit somewhere between a traditional national stockpile and a syndicated revolving inventory facility.

On the corporate side, risk committees and procurement teams have pushed suppliers to hold more inventory, sometimes funded through prepayments or take-or-pay frameworks. In many OEMs observed by Materials Dispatch, this has led to parallel inventory chains: conventional just-in-time flows for routine operations, and a “shadow” layer of safety stock in warehouses, bonded facilities, or supplier premises, often in multiple jurisdictions to hedge customs and sanctions exposure.

Policy and regulatory context around the next shock

Several regulatory threads intersect with critical materials stockpiling:

- Export controls and sanctions. China’s moves on gallium, germanium, and graphite demonstrated that export permits can be turned into tactical levers. Western sanctions on Russian metals (including certain alumina, copper products, and PGMs) have likewise shown how quickly a product can shift from fungible to constrained in specific markets.

- Tariffs and trade remedies. The United States and European Union have used anti-dumping duties and targeted tariffs on aluminum, steel, and some downstream products. Discussions have expanded to refined copper and semi-finished goods, with some policy scenarios for the latter half of the decade contemplating higher tariffs on refined imports that could incentivize pre-emptive stockpiling.

- Cyber and operational resilience rules. The EU NIS2 Directive broadens cybersecurity obligations to a wide list of “essential and important entities”, including parts of the mining and metals value chain. This introduces mandatory risk assessments, incident reporting, and network segregation for operational technology (OT) in mines, refineries, and processing plants, with national transposition deadlines around 2024–2025.

- Climate and ESG-linked trade instruments. CBAM and similar mechanisms intend to reprice carbon-intensive imports, including some steel and potentially other metals, over time. ESG-focused taxonomies and due-diligence laws are pushing OEMs to map supply chains down to mine sites, raising the bar for any stockpile sourced from opaque or high-emission operations.

These instruments create an environment in which access to material is governed not only by mine output, but also by which jurisdictions are allowed to move which products, under what conditions, and with what data trails.

Key non-Chinese projects reshaping the landscape

Alongside stockpiling, a wave of projects outside China is attempting to rebalance supply for rare earths, lithium, and select strategic metals. As of late 2024, several clusters stand out:

- North American rare earths and magnet materials. MP Materials’ Mountain Pass operation in California has resumed large-scale rare earth production, with an ongoing build-out of separation and magnet-making capacity. In Canada and the United States, Energy Fuels (White Mesa), Texas Mineral Resources (Round Top), and other players are pursuing rare earth recovery from monazite, polymetallic deposits, and recycling streams, often with Department of Defense or Department of Energy support.

- Australian and Angolan rare earth chains. Lynas’ Mt Weld mine and Kalgoorlie processing plant, Iluka’s Eneabba rare earth refinery, Arafura’s Nolans project, Northern Minerals’ Browns Range, and Pensana’s Longonjo–Saltend combination form the core of a non-Chinese rare earth separation pathway spanning Australia, Angola, and the UK. Several of these projects focus on high-value magnet elements such as neodymium and dysprosium.

- Battery raw materials in the Americas. In lithium, Albemarle’s Silver Peak brine operations and Lithium Americas’ Thacker Pass project in Nevada have become focal points for U.S. supply, supported by loan guarantees and offtake commitments from major automakers. In parallel, recycling-focused facilities (for example, magnet and motor recycling in Canada and Europe) seek to recover neodymium and other critical inputs from end-of-life products.

- Recycling and circular flows. Neo Performance Materials and other specialized processors are building capacity to take scrap magnets, motors, and batteries from North America, Europe, and East Asia, converting them into separated rare earth oxides or alloys suitable for new magnet production. These facilities are typically smaller by tonnage than greenfield mines but can contribute disproportionately to supply security because they are located inside allied jurisdictions and rely on urban scrap rather than imported ore.

Public discourse around these projects generally emphasizes offtake agreements with OEMs, government-backed financing, and the link to national security or electrification goals. For Materials Dispatch, they also represent the practical limits of what stockpiling can achieve: no amount of warehouse inventory in Europe or North America can substitute for absent or underdeveloped refining and separation capacity in these regions.

INTERPRETATION: Why stockpiling alone will underperform in the next shock

Stockpiles merely delay the impact of policy and refining shocks

From Materials Dispatch’s standpoint, the core weakness of a stockpile-centric view is simple: it assumes that a future disruption will look like a temporary logistics issue or short-lived price spike. That assumption is increasingly out of step with reality. When a government introduces an export licensing regime for a critical input, or when a cyber incident disables a major refinery under tightened regulatory scrutiny, the disruption is not a two-week event. It is a structural regime change.

In that context, stockpiles function as a time-limited grace period. They allow OEMs to keep assembling vehicles, aircraft, or electronics for a few months while policy, legal, and technical teams scramble. But if refining capacity remains concentrated and alternative supply paths are not already qualified, the buffer simply postpones the moment when production has to slow or stop. This is what Materials Dispatch means when describing stockpiling as a band-aid on a hemorrhaging chain: it covers the wound, it does not address the underlying cause.

The 2023–2024 experience with gallium and germanium export controls already hinted at this dynamic. Downstream users with inventories were initially insulated; as export licenses tightened, the market split between those who had pre-qualified non-Chinese sources or could redesign components, and those who were left bidding within a shrinking, policy-constrained pool. The next shock in rare earths, graphite, or refined copper would likely follow a similar pattern.

The operational drag of parallel inventory chains

From a supply-chain operations perspective, large stockpiles introduce non-trivial friction. Maintaining separate inventories for steel, aluminum, copper, and rare earth–bearing components already results in duplicated freight, insurance, and warehousing flows. Layering strategic stockpiles on top of just-in-time operations effectively doubles quality-control regimes, audit trails, and ESG documentation requirements for the same tonne of material.

In audits observed by Materials Dispatch, OEMs that built extensive critical-minerals buffers often discovered that, in practice, the reserves were treated as untouchable except in extreme emergencies. Plant managers hesitated to draw them down because replenishment terms were uncertain, or because the materials had been procured under different specifications or ESG criteria than day-to-day supplies. In several cases, parallel inventory chains drove up working capital and complexity far more than they improved real-world resilience.

There is also a degradation dimension that stockpiling enthusiasts tend to downplay. For many metals, declining ore grades, evolving process technologies, and tighter product specifications mean that material produced today is not perfectly fungible with material that will be required five or ten years from now. Holding large volumes of undifferentiated raw oxides or concentrates can therefore lock OEMs into older specifications just as defense and EV platforms move to new magnet chemistries or higher-voltage battery designs.

Diversified projects and long-term agreements as structural mitigants

If stockpiles address timing, diversified projects address topology. Non-Chinese rare earth projects in Australia, North America, and Africa; lithium brine and hard-rock developments in the Americas; magnet and battery recycling plants in Europe and Canada – collectively, these assets reshape where physical and political bottlenecks sit in the chain. When separation and alloying occur under regulatory regimes aligned with downstream OEMs, export controls and sanctions have less leverage, and logistics rerouting becomes more feasible.

In practice, many of these projects hinge on long-term supply and processing agreements with OEMs or tier-one suppliers. These contracts often help secure project financing and underpin final investment decisions. They also lock in technical collaboration on specifications, quality-control regimes, and ESG reporting. From a resilience standpoint, the critical feature is not that offtake agreements exist, but that they connect physical assets in jurisdictions less prone to sudden export curbs with end-use platforms that can absorb that material at scale.

that said, such diversification comes with its own constraints. Project development timelines are long, permitting is politically contested, and ESG expectations are rising. Several of the flagship rare earth and lithium projects outside China have faced legal challenges from local communities, environmental groups, or competing land users. That means OEMs and policymakers trying to use project pipelines as a hedge against future shocks need to accept that delays, redesigns, and partial scale-backs are intrinsic features, not exceptions.

Design-led mitigation: material substitution and efficiency

Materials Dispatch’s analysis of procurement crises over the past decade repeatedly converges on one conclusion: the only truly durable hedge is design. The rare earth episode of 2010–2012 triggered a wave of motor and magnet redesign work, leading to lower dysprosium content in traction motors and increased use of ferrite or hybrid magnet configurations where performance allowed. Copper tightness has already pushed several EV and industrial platforms toward aluminum for certain busbars and wiring harnesses, trading conductivity and handling complexity for reduced dependence on copper smelting bottlenecks.

Similar dynamics are now emerging in batteries. Solid-state and high-manganese chemistries are being pursued partly to reduce reliance on cobalt and nickel. Even where these technologies remain in the pilot or pre-commercial phase, the direction of travel is significant for critical materials planning: if new designs can tolerate a wider range of input chemistries and specifications, they inherently weaken the grip of any single refining node or export regime.

The trade-off is time. Serious design changes – whether a new magnet recipe for an aircraft actuator or an aluminum-intensive harness for an EV platform – typically require 6–18 months of R&D, prototyping, supplier qualification, and regulatory or customer recertification. From the vantage point of mid-2020s policy risk, that is still faster than building a new refinery or mine from scratch, but far slower than ordering another tranche of stockpiled oxide. This time mismatch is precisely why stockpiles appear attractive politically and corporately, even as they leave the fundamental concentration risk untouched.

Policy-timed risk: why 2025–2027 matters

Many of the regulatory levers that affect critical materials are on staggered timelines clustered around the mid-2020s. EU member states are transposing NIS2 into national law, with enforcement likely to tighten around 2025–2026 for mining and processing assets. CBAM is moving from transitional reporting to actual financial adjustments. Trade authorities in the United States and Europe continue to investigate refined metal imports, with scenarios circulating in policy circles that include higher tariffs on refined copper and other semi-finished products later in the decade.

In parallel, resource-rich states are experimenting with their own levers, from export licensing on graphite in China to changing royalty and processing rules in countries such as Indonesia, Chile, or African jurisdictions hosting rare earth and battery-metal projects. Each such change can, in principle, trigger stockpile drawdowns if it crosses predefined thresholds in public–private “vault” schemes or corporate risk frameworks.

The uncomfortable implication is that stockpiles created under one tariff, sanction, and ESG regime may have to be replenished under a very different one. If a government or OEM releases inventory in response to an export ban, and the ban persists or is broadened, replenishment could occur at higher prices, under stricter ESG rules, and with fewer eligible suppliers. In that scenario, stockpiling has not removed risk; it has time-shifted and, in some cases, amplified it.

WHAT TO WATCH

- New or expanded export controls on refining-intensive inputs. Announcements from major producers on graphite, rare earths, gallium, germanium, or battery precursors are likely to determine how quickly existing stockpiles are drawn down and how tight replenishment windows become.

- Tariff and trade-remedy investigations on refined metals. Probes into refined copper, aluminum, or semi-finished products in the United States, EU, or key allies could trigger anticipatory stockpiling surges and reshape the economics of holding inventory versus backing new refining capacity.

- Final investment decisions and commissioning milestones for non-Chinese projects. The timing of FIDs and first production at rare earth projects such as Nolans, Eneabba, Browns Range, Round Top, and at lithium assets like Thacker Pass, will be critical signals for when diversification can move from slideware to physical tonnes.

- Implementation of NIS2 and similar cyber rules in mining and refining. Early enforcement actions, incident reports, or mandated shutdowns at mines and processing plants will reveal how much operational risk is added by new cybersecurity regimes, and how much that erodes the value of distant stockpiles.

- OEM design and platform announcements. Public commitments by automakers, aerospace primes, and defense contractors to shift magnet chemistries, wiring materials, or battery architectures away from constrained inputs will indicate how rapidly design-led mitigation is progressing relative to stockpiling.

- Terms and governance of any shared “vault” or strategic reserve schemes. The specific trigger conditions, replenishment rules, and ESG/cyber requirements written into multi-party stockpile vehicles will determine whether these function as stabilizers or as amplifiers of future shocks.

Note on Materials Dispatch methodology Materials Dispatch combines continuous text monitoring of government and regulatory announcements with project-level tracking of mines, refineries, and recycling plants, and close reading of OEM and tier-one technical specifications. The analysis above reflects that triangulation rather than reliance on any single dataset, and remains explicitly bounded by stated policy texts and publicly disclosed project status.

Conclusion

Stockpiles will remain part of the critical materials toolkit; boards, ministries, and procurement leaders are unlikely to abandon the psychological comfort of physical reserves. Yet the structure of current and emerging shocks – driven by refining concentration, export policy, cybersecurity obligations, and ESG-linked trade instruments – means that inventory buffers alone are poorly matched to the real risk profile.

In the reading of Materials Dispatch, the decisive fault lines in the next materials shock will run through where refining occurs, which jurisdictions control export valves, and how flexibly end-use designs can accommodate alternative materials and sources. Stockpiling can buy months; diversified projects and design changes can reshape decades. The coming period will reward close, active monitoring of regulatory and industrial weak signals that determine which of these pathways dominates.