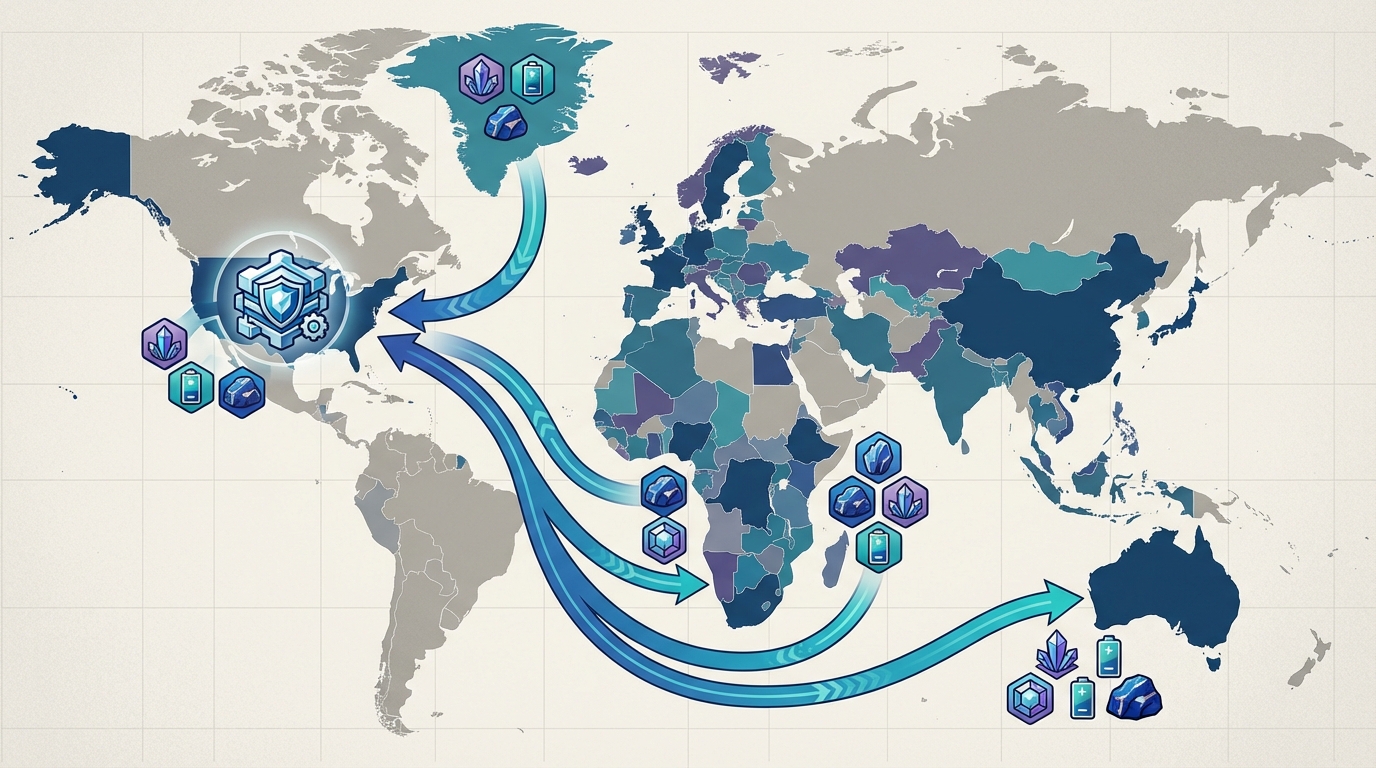

China accounts for ~98% of global low-purity gallium, creating a structural supply choke point.

Export licensing (from Aug 2023) and a U.S.-targeted ban (announced Dec 3, 2024; suspended Nov 2025–Nov 2026) drove spot prices from about $240/kg to roughly $575/kg.

Ongoing licensing discipline and technology controls are likely to keep supply risk elevated through at least 2027.

Producers and downstream operators should map exposure, lock multi-year offtakes from non-Chinese sources, and build strategic stockpiles where feasible.

The Gallium Shock: Market Dynamics and Strategic Imperatives

Executive Summary

Materials Dispatch assesses how China’s near-monopoly on gallium—a byproduct metal vital for gallium-arsenide (GaAs) and gallium-nitride (GaN) semiconductors—has been leveraged through export licensing and a targeted restriction on U.S. shipments. Licensing controls since August 2023 and a Dec. 3, 2024 ban (suspended Nov. 2025–Nov. 2026) helped push spot prices from about $240/kg in mid-2023 to roughly $575/kg by December 2024. Crucially, the measures did not only constrain trade flows; they also tightened access to extraction technologies (notably ion-exchange/resin pathways). That combination supports structurally high supply risk through at least 2027, forcing semiconductor, defense, and power-electronics supply chains to move from scenario discussion to operational resilience planning.

Market Context and Supply Concentration

Gallium is recovered as a minor stream from aluminum and zinc refining, yet it underpins key technologies: RF front-ends, power electronics, radar, optical sensors, and high-efficiency LEDs. China controls approximately 98% of global low-purity output, creating a single-point failure dynamic for anything that depends on refined gallium supply. The strategic implication is straightforward: even when end-market demand is stable, licensing and technology controls can abruptly alter availability of material that downstream firms cannot easily substitute in the short run.

Before restrictions, U.S. exposure was especially sensitive because the supply chain was narrowly sourced and inventory depth was thin relative to the scale of semiconductor and defense demand. In practice, that means “spot” availability is not only a function of production capacity—it reflects whether qualified sellers can ship and whether customs clearance and end-use declarations remain acceptable under the licensing regime.

Policy Timeline and Price Impact

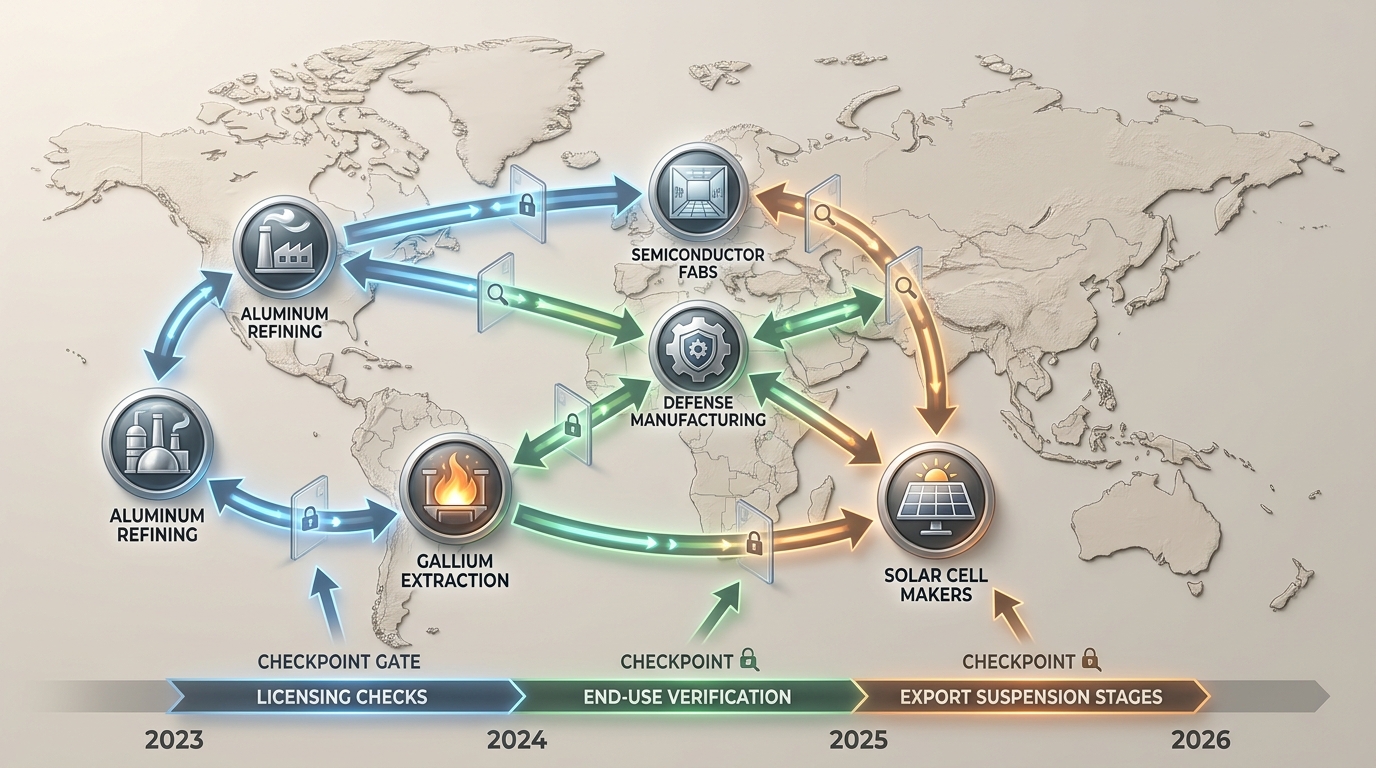

Licensing Shock (Aug 2023): Exports of gallium and germanium required MOFCOM licenses and end-use declarations (export licensing is a permit system where authorities review the exporter, end-user, and intended use). Chinese customs data indicated near-zero wrought gallium exports during the first months after controls tightened. Exports then reappeared at much lower volumes in October 2023—reflecting the compliance friction and discretionary nature of licensing. Spot markets responded quickly: prices moved higher by the October 2023 period, setting the tone for a prolonged repricing rather than a brief spike.

Global semiconductor supply chains rely heavily on Chinese gallium exports.

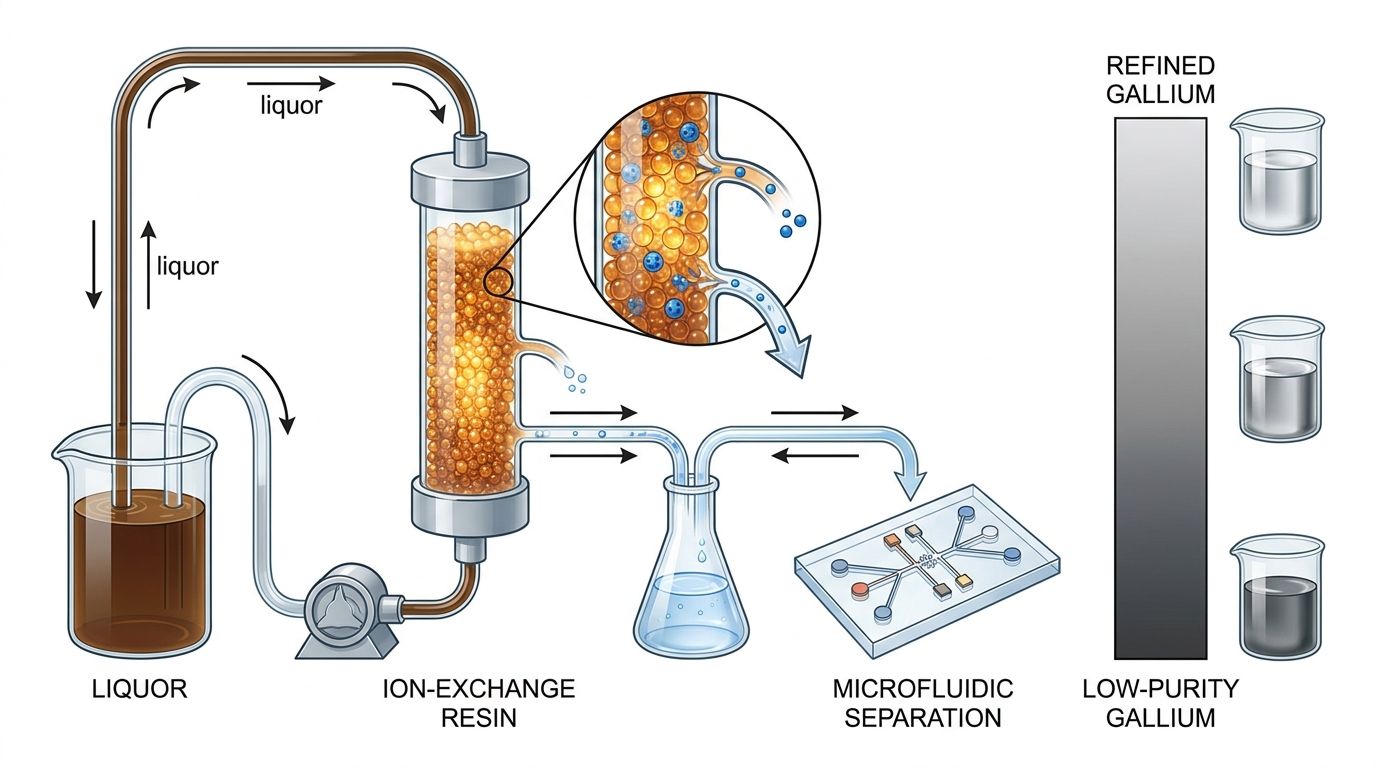

U.S. Ban & Technology Controls (Dec 3, 2024): MOFCOM escalated measures with a country-specific export ban on gallium, germanium, antimony, and superhard materials to the United States. At the same time, the export control catalogue was expanded to restrict gallium extraction technologies—specifically “technologies and processes to extract metallic gallium from alumina mother liquor using ion-exchange or resin methods.” That matters commercially because it targets the recovery pathway that supports conversion from feedstock streams into metal. Prices peaked at about $575/kg in December 2024 as buyers priced in both reduced trade access and reduced medium-term recovery optionality.

Partial Suspension (Nov 2025–Nov 2026): A temporary lift of the U.S. ban reduced political signalling risk but did not remove the underlying licensing and technology controls. As a result, downstream buyers should not interpret the suspension as a full return to “pre-shock” market normalcy; it primarily changes the risk of outright shipment prohibition to the U.S., while compliance requirements and technology restrictions continue to constrain the broader supply system.

Economic and Strategic Impacts

Gallium’s supply leverage becomes visible in how quickly disruptions propagate into manufacturing lead times. A gallium shortage is not like a commodity inventory issue that can be resolved through routine brokerage; it can interrupt component qualification cycles for GaAs/GaN RF and power devices, slow radar and sensor procurement timelines, and complicate substitution decisions across device architectures.

Regulatory attention also follows the supply logic. In Europe, gallium’s status as a strategic resource has been used to reinforce the policy focus on critical raw materials—an approach designed to support diversification, transparency, and stockholding where supply risk is concentrated. Taken together, these developments underline a market reality: the “real” constraint is not only mining or refining volumes, but the ability to legally and technically recover gallium into usable forms.

Gallium and gallium-based semiconductors are critical for power electronics and advanced communications.

Supply-Side Response

Global high-purity production and recycling are meaningful balancing factors, but the shock exposed how asymmetric the geography of upstream capability remains. Non-Chinese recovery projects have been announced across multiple jurisdictions, yet most are still at feasibility, engineering, or early implementation stages relative to the immediacy of downstream demand. That lag is economically important: even credible projects do not neutralize risk for lead times that can span quarters of device fabrication and qualification.

Recycling capacity outside China remains limited compared with the scale implied by global tightness. For industrial planners, that means the “supply response” is likely to be incremental rather than immediate—pushing the market toward a longer period of negotiated offtakes, careful quality management, and higher dependence on storage and contracted procurement.

Scenarios & Probabilities

Managed Constriction (Base Case, ~60%): Licensing remains discretionary and technology controls remain in place. Price premiums persist as buyers continue to source via contracted channels rather than pure spot purchasing, while non-Chinese capacity additions gradually improve medium-term availability toward the late 2020s.

Escalation & Crackdown (High Stress, ~25%): Renewed geopolitical tensions increase the likelihood of targeted enforcement, re-export scrutiny, and sharper shipment restrictions. The outcome is less about total global output and more about sudden loss of route access—driving acute shortages and episodic spikes.

Diversification Relief (Optimistic, ~15%): Alliances deepen and recovery pathways diversify. Alternative resin and processing compliance pathways, plus more robust upstream contracting, reduce reliance on Chinese-origin supply and gradually ease pricing pressure toward earlier baselines.

Actionable Intelligence

Materials Dispatch recommends a three-horizon response:

Immediate (Next 4 Weeks): Map gallium exposure to Tier-3 suppliers (not just cell or device assemblers). Stress-test inventories against a six-month cutoff scenario, and review force-majeure plus re-export clauses to ensure contractual compliance aligns with export licensing requirements and end-use documentation expectations.

Short-Term (Next Quarter): Secure multi-year offtake agreements with non-Chinese recovery/refining counterparties where quality and compliance can be validated. Align corporate stockpile targets with national or consortium initiatives (including programs referenced in U.S. and EU contexts, such as Project Vault and EU critical-material policy efforts), focusing on the material forms actually required by downstream processes.

Long-Term (Through 2027+): Co-invest in upstream recovery and recycling pathways, and integrate gallium risk into fab siting and product qualification planning. Codify critical-material playbooks for single-supplier and route-access scenarios to prevent procurement decisions from being driven solely by spot price movements.

Signals to Monitor

Price Levels: Track European and global spot markers closely, but treat large price prints as a sign of route-risk and licensing friction—not just supply scarcity.

Policy Updates: Monitor MOFCOM notices for changes in licensing mechanics, expansions or clarifications of extraction-technology controls, and any further updates to U.S. ban suspension timing after Nov 2026.

Re-export Flows: Watch for discrepancies between Chinese export reporting and U.S./EU import data, particularly when routing intermediates appear to increase.

Project Milestones: Prioritize announcements tied to FID and commissioning timelines for non-Chinese recovery capacity, since earlier-stage plans do not address near-term procurement constraints.

Stockpile Actions: Follow public procurement developments and strategic-reserve frameworks that attempt to translate policy intent into physical availability.

Conclusion

China’s export licensing and the U.S.-targeted ban have crystallized gallium’s role as a strategic lever in semiconductor and defense supply chains. With technology controls aimed at extraction pathways, tightness risk is likely to remain elevated through at least 2027 even when the U.S. shipment restriction is temporarily suspended. Operators should accelerate exposure mapping, diversify sourcing through credible non-Chinese projects, and institutionalise strategic stockpiling and contractual compliance to reduce vulnerability to future route disruptions.

China commands roughly 98–99% of primary low-purity gallium production, creating a “by-product trap” for global supply response.

Since July 2023, Beijing has sequenced licensing, embargoes, technology controls and tactical suspensions to toggle gallium exports on short notice.

Allied initiatives to develop alternative recovery capacity face economic and technological hurdles absent long-term offtake assurances.

Procurement, supply-chain and compliance teams must map indirect gallium exposure and plan for rapid policy reversals.

Executive Summary

China’s calibrated export and technology controls on gallium since mid-2023 reveal a deliberate playbook for exerting leverage over Western semiconductor, defense and clean-tech supply chains. Gallium is not scarce geologically—it is a minor by-product of bauxite and zinc refining—but China’s 98–99% share of primary low-purity gallium production and its proprietary extraction technologies empower Beijing to impose sudden restrictions. Even after the November 2025 suspension of the U.S. civilian export ban (extended through late 2026), the regulatory and technology choke points remain in place, posing persistent disruption risks for procurement and strategy teams.

Defining the “By-Product Trap”

The term “by-product trap” captures a structural constraint: non-Chinese producers cannot scale gallium output quickly because gallium is produced incidentally during large-scale aluminum and zinc operations. Re-establishing recovery circuits typically requires multi-year investments, qualified permitting, and process validation—meaning volumes cannot be toggled at the speed that policy can be toggled. In practice, this creates a reflexive market dynamic: when restrictions tighten, buyers face not only availability risk, but also the prospect that higher prices may be temporary if Chinese supply temporarily re-accelerates later, suppressing incentives to build outside capacity.

Export Control Timeline

July 2023: MOFCOM introduces licensing requirements for gallium and germanium exports, quickly reshaping pricing and export flows as end-use scrutiny tightens.

December 2024: Announcement No. 46 enacts a de facto embargo on U.S. gallium imports, halting civilian shipments and tightening the effective boundary for military end-use.

January–May 2025: Technology controls on extraction processes—specifically purification approaches that rely on ion-exchange and resin methodologies—alongside coordinated anti-smuggling enforcement deepen China’s chokehold on both volumes and know-how.

November 2025: Announcement No. 72 suspends the civilian embargo until late 2026 but preserves licensing authority, military restrictions and technology controls for rapid re-implementation.

Market and Price Dynamics

Gallium prices have behaved like a policy indicator rather than a pure supply-demand equilibrium. When licensing and enforcement tighten, buyers experience both immediate transactional friction (longer lead times, narrower sourcing channels, compliance overhead) and forward-looking uncertainty about whether volumes will be available in subsequent quarters. That uncertainty tends to flow through contracts, inventory strategies and safety-stock policies—raising effective demand even when end-user consumption has not changed.

USGS-based scenario analysis estimates that a sustained gallium and germanium cut-off could cost the U.S. economy $3.4 billion in GDP, with semiconductors bearing about half the impact. The key procurement implication is not merely “what happens if supply disappears,” but how quickly downstream plans can absorb upstream volatility when specifications, qualification testing and replacement approvals introduce friction.

Visual timeline of licensing → embargo → suspension and downstream impacts.

For market participants, the most important nuance is that gallium’s by-product origin means that alternative supply is not elastic. Even where material exists in scrap or industrial streams, converting it into usable gallium requires recovery pathways and quality certification—so short-term price signals do not automatically translate into rapid, fungible supply.

Fragmented Coverage and Strategic Blind Spots

Specialist commodity analysts and policy think tanks meticulously track gallium export measures, production quotas and price effects. Mainstream tech and gaming-oriented outlets, however, often focus on downstream semiconductor shortages—GPUs, AI chips and lithography capacity—without naming gallium as an upstream bottleneck. This siloed coverage risks underestimating how quickly a “hardware story” can become a “critical minerals story” when Beijing activates its regulatory switch.

Process diagram showing why extraction technology is a control point.

For institutional stakeholders, the practical problem is measurement: if gallium exposure is not mapped by end-application, then policy moves can be misread as isolated input disruptions rather than as repeatable sovereign-risk events. In turn, that misreading delays mitigation—such as qualification of alternative feedstocks, redesign of procurement specifications, and compliance controls that prevent sourcing from becoming a legal and operational liability.

Allied Responses and Alternative Supply Efforts

Governments and firms in the U.S., EU, Japan, South Korea and Australia have launched feasibility work aimed at recovering gallium from bauxite, zinc and industrial scrap. European refiners and industrial groups have explored recovery pathways, while Japanese and Korean players emphasize closed-loop recycling strategies to reduce reliance on fresh primary feedstock. Australia’s bauxite-linked pathways have also been examined, though many efforts remain constrained by pilot-stage scale-up and commercialization risk.

Illustrate semiconductor supply vulnerability under export restrictions.

Across these initiatives, two challenges recur. First, by-product recovery is capital intensive: it requires additional processing steps, quality control and integration into existing refinery or waste-treatment workflows. Second, absent credible protection against future Chinese market surges, investment returns can remain uncertain—especially if policy can be tightened or relaxed faster than alternative capacity can qualify and deliver on consistent specifications.

Implications for Industry Stakeholders

Procurement and Category Management

Map direct and indirect gallium exposure. Treat gallium as a cross-cutting input across RF and power electronics, LEDs/optics, and PV-linked bills of materials—then document where qualification and substitution are realistic versus where they are not.

Scrutinize provenance, not just geography. Move beyond “country of last transformation” labels. For by-product metals, feedstock integrity and process history materially affect compliance posture and technical acceptance.

Negotiate inventory buffers and contractual resilience. Build flexible delivery terms, and add contingency clauses that explicitly address export control events and compliance-driven shipment holds.

Plan for recycled gallium as a structured supply lever. Integrate recycling streams from scrap and end-of-life devices where possible, and treat recovery yield variability as a managed risk rather than an assumption of steady-state output.

Supply-Chain Strategy and Operations

Scenario-plan for rapid policy toggles. Treat licensing changes, enforcement campaigns and temporary suspensions as repeatable scenarios. Then assess the downstream ripple effects on production schedules and inventory consumption rates.

Engage early with recovery projects, but anchor risk allocation. Use consortia or anchor offtake discussions to clarify who bears commercialization, yield and compliance certification risk.

Coordinate with R&D on material substitutes where technically viable. Substitute materials—such as silicon carbide in power electronics contexts—should be evaluated as qualification programs, not as instantaneous substitutes.

Embed regulatory monitoring into S&OP cycles. Incorporate signal monitoring across MOFCOM-linked developments and Western critical minerals/export control frameworks so forecasting assumptions are updated before procurement commitments become irreversible.

Trading Desks and Risk Management

Anticipate policy-driven volatility. Calibrate hedging logic to scenario distributions shaped by regulatory timing, not only by observed spot price behavior.

Monitor basis risk across venues. Track differences between Chinese domestic pricing signals, Rotterdam-linked market references, and end-user procurement pricing to avoid assuming uniform pass-through.

Avoid overestimating “normalization” from downstream announcements. Materials constraints—especially for by-product metals—can remain binding even when consumer-facing production schedules appear stable.

Compliance and Legal Considerations

Operate under dual-jurisdiction risk. Track both Chinese export control lists and Western critical minerals frameworks to prevent misalignment between sourcing decisions and compliance obligations.

Strengthen due diligence on intermediaries. Enhanced screening is essential for intermediaries and re-export hubs, given the elevated risk of illicit diversion pathways during policy tightening.

Prepare for evolving “trusted source” expectations. Expect procurement systems to increasingly favor documentation-intensive sourcing, especially where end-use verification and process provenance become gating factors.

Conclusion

China’s gallium playbook demonstrates how targeted export and technology controls on a by-product metal can deliver outsized leverage over critical supply chains. The November 2025 civilian suspension does not remove the underlying choke points; it only changes the timing and the conditions under which restrictions may be activated. Decision-makers should treat gallium as an enduring vulnerability—using this window to diversify sourcing, reinforce recycling, and institutionalize policy-risk scenarios into strategic planning.

Dissecting Top 12 China-Independent Critical Mineral Narratives: Supply Risk vs Reality

Key Takeaways

China retains integrated control over 60–90% of rare earth mining and refining, including heavy rare earth elements (HREEs).

Non-Chinese projects face permitting delays, higher costs, and ESG constraints that extend timelines by 5–7 years.

Resource diversification alone does not equal processing independence; offtake contracts and mid-stream choke points matter.

Projects like Mountain Pass and Lynas Texas advance resilience but cover only fractional shares of global demand.

Robust mapping of financing, processing routes, and regulatory friction points is essential for genuine supply security.

Across defense, EV, wind, and advanced electronics supply chains, strategic planners hear promises of rapid transition to “China-independent” critical mineral supply. Rare earths encompass light rare earth elements (LREEs) such as neodymium (Nd) and praseodymium (Pr), and heavy rare earth elements (HREEs) including dysprosium (Dy) and terbium (Tb). Total rare earth oxides (TREO) denote the combined oxides of all 17 lanthanides plus yttrium. Materials Dispatch’s review of 2024-2025 project data, trade flows, and ownership structures reveals a harsher reality: China still controls roughly 60–90% of rare earth mining and refining capacity and dominates HREE supply.

This briefing ranks the top 12 “China-independent” narratives by their strategic distance from reality. We contrast public storylines with operational details—contract terms, logistics, processing routes, and observed failure modes. The goal is to calibrate expectations and highlight the real levers that move supply risk.

1. US Mountain Pass Mine as a Fully Domestic “Mine-to-Magnet” Solution

The Asset / Risk. Mountain Pass in California is often introduced in official speeches as the linchpin of a sovereign US rare earth supply chain: mine, refine, and manufacture NdFeB magnets on US soil. The mine produces 40,000–60,000 MT/year of TREO concentrate, heavily weighted to LREEs such as Nd and Pr.

Strategic Context. For US defense platforms and EV drive motors, Mountain Pass anchors domestic mining know-how and signals U.S. progress toward China’s magnet ecosystem. The plan to add domestic separation and magnet production is framed as the final step to full independence.

The Bottleneck. On the ground, nearly 100% of concentrate still ships to China for separation. HREE separation (Dy, Tb) remains a critical gap. Scaling solvent-extraction circuits under US environmental and labor constraints is slower and costlier than in China. Even at a planned 1,000 MT/year NdFeB capacity—<1% of China’s 138,000 MT in 2018—the facility depends on power, skilled labor, and steady capex. Permitting delays have stretched timelines beyond initial guidance, and any regulatory hiccup in waste or water management triggers fresh reviews.

The Verdict. Mountain Pass enhances upstream resilience for LREEs and provides a partial hedge against raw-material shocks. It does not deliver a closed-loop, China-independent chain in the 2025–2030 window. Risk assessments should track domestic separation commissioning, long-term power contracts, and residual reliance on Chinese reagents or offtake partners.

2. Australia’s Nolans Project as an Allied HREE Independence Engine

The Asset / Risk. The Nolans project in Australia’s Northern Territory is positioned as an “ally-only” source of RE oxides, with integrated mining and processing to bypass China. Public messaging often blurs its primary LREE focus (NdPr) with the scarcer HREEs needed for defense and offshore wind magnet temperature performance.

Strategic Context. For OEMs in Japan, Europe, and North America, a stable NdPr source in Australia supports diversification. Government support and offtake agreements with non-Chinese customers reinforce the impression of a clean break from China’s dominance.

The Bottleneck. By mid-2020s, Nolans remained in advanced development, with construction and commissioning repeatedly delayed by environmental approvals, workforce constraints, and cost inflation. HREE volumes are modest relative to global deficits. Remote logistics, port capacity limits, and minority-stake approaches from Chinese-linked entities underscore challenges in fully divorcing from China’s processing ecosystem.

The Verdict. Nolans adds medium-term value for LREE diversification but is not a turnkey HREE solution. Planners should monitor final financing, offtaker identities, and any toll-separation routing through Asian hubs.

3. Brazil’s Serra Verde as a Non-Asian Light + Heavy REE Powerhouse

The Asset / Risk. Serra Verde in Goiás, Brazil, is promoted as the first major ionic-clay REE mine outside Asia, offering both LREE and meaningful HREE output. Ionic clays can be leached at relatively low cost, with lower-carbon profiles versus Chinese or Myanmar clays.

Strategic Context. Multinational OEMs value jurisdictional diversification and mixed LREE/HREE output for EV motors, offshore wind, and industrial catalysts.

The Bottleneck. Early offtake deals defaulted to Chinese processors due to scale and installed capacity. Brazilian environmental regulations and tailings management add compliance costs and delays. Labor disputes and port congestion create unpredictable export flows.

The Verdict. Serra Verde diversifies the resource base but not processing control. Procurement teams should scrutinize offtake contracts, potential redirection to non-Chinese processors, and Brazilian regulatory shifts.

4. Aclara’s Latin American Projects as ESG-Perfect, Fully Western Chains

The Asset / Risk. Aclara’s ionic-clay projects in Chile and Latin America are marketed on strong ESG credentials—closed-loop water use and ion-exchange technology feeding a planned US separation hub.

Strategic Context. A low-impact Latin American resource plus US processing facility would showcase allied industrial cooperation for defense and EV magnet supply chains under ESG pressure.

Global overview diagram contrasting mining, refining, and recycling nodes across the 12 ‘China-independent’ narratives.

The Bottleneck. Scaling ion-exchange from pilot to commercial scale poses throughput, resin-degradation, and water-quality challenges. US separation permitting under NEPA and local zoning can extend to five–ten years. Financing must tolerate schedule creep and evolving regulatory requirements around PFAS and waste.

The Verdict. Aclara offers a credible late-decade HREE pathway but remains aspirational for the 2020s. Its value hinges on firm offtake contracts, social license in Latin America, and US regulatory progress.

5. US Recycling (Vulcan, ReElement and Peers) as a Leapfrog over Mining

The Asset / Risk. US recycling ventures backed by defense funding promise to recover several thousand tonnes per year of RE oxides from e-waste and industrial scrap, framed as a way to “skip” upstream mining.

Strategic Context. Onshore recycling aligns with security-of-supply mandates and ESG goals, offering potential to flatten HREE price volatility if mine development lags.

The Bottleneck. Limited and fragmented REE-bearing scrap streams, purity and consistency challenges, and pilot-scale facilities with 12–24 month ramp-ups restrict near-term impact. Recovered purity (high-80s to low-90s%) often falls short of virgin-like specs, necessitating additional purification.

The Verdict. Recycling can offset 10–20% of rare earth needs in niche segments, especially defense. It is not a structural replacement for mining this decade. Track scrap-supply agreements, military qualification of recycled materials, and hazardous-waste regulations.

6. Greenland’s Kvanefjeld and Tanbreez as an Arctic HREE Safety Valve

The Asset / Risk. Greenland’s Kvanefjeld and Tanbreez deposits are invoked as potential sources of 20–25% of global HREE needs under Danish oversight.

Strategic Context. NATO planners cite geopolitical alignment and Arctic shipping proximity as advantages for HREE supply.

The Bottleneck. Projects are stalled by uranium restrictions, permafrost engineering challenges, seasonal shipping windows, and local opposition. Arctic conditions triple logistics costs versus temperate ports.

The Verdict. Greenland remains a strategic option, not an active mid-decade contributor. Model it as upside contingent on regulatory shifts, waste-management innovation, and Arctic infrastructure progress.

7. Canada’s Nechalacho as an Ethical HREE Cornerstone for North America

The Asset / Risk. Nechalacho in Canada’s Northwest Territories is promoted for “ethical” REEs from a high-standards jurisdiction, with small open-pit production and nearby processing.

Strategic Context. Fits USMCA rules-of-origin and ESG reporting; validates modular mining and initial processing in remote environments.

The Bottleneck. Scale remains modest (hundreds of tonnes/year), with full separation via toll processing in Europe. Sub-arctic conditions limit operating days and raise logistics costs. Major expansion requires lengthy permitting and community consultation.

The Verdict. Nechalacho is a high-integrity, low-volume node in the North American REE network. Watch moves toward onshore separation, remote power solutions, and Indigenous royalty frameworks.

8. Tanzania’s Ngualla (Peak Rare Earths) as a “Western-Controlled” African Supply

The Asset / Risk. Ngualla was cited as a Western-developed African resource with high TREO grades, poised to supply magnet materials free of Chinese influence.

Strategic Context. African sourcing appeals to OEMs seeking diversification, with Tanzania courting foreign investment and value-addition.

The Bottleneck. Ownership shifted to a Chinese-linked company, undermining the “Western-controlled” narrative. Tanzanian local-content rules and export levies add fiscal complexity. Grid instability and infrastructure gaps drive up capex and schedule risk.

The Verdict. Ngualla remains geologically attractive but no longer advances Western supply security. Treat it as a contributor to global tonnage, not a diversification win. Monitor Tanzanian policy, offtake structures, and parallel non-Chinese processing lines.

9. Lynas’ Texas Facility as the End of US Processing Dependence

The Asset / Risk. The DoD-supported Lynas plant in Texas is presented as closing the US loop for NdPr and select HREE processing under US law.

Strategic Context. “Kalgoorlie → Texas” is marketed as a clean, ally-controlled chain for defense-critical components.

The Bottleneck. Stricter US emissions and wastewater rules, community engagement, and technical scale-up challenges have stretched schedules and costs. Initial capacity covers only a fraction of US demand; HREE capability phases in slowly.

The Verdict. The Texas facility is a concrete step toward non-Chinese mid-stream capability, but it addresses only a slice of US needs. Track recovery rates, residue handling, permitting challenges, and energy-water agreements.

10. South African PGMs as a Platinum/Palladium Buffer against China

The Asset / Risk. South African platinum group metals (PGMs) underpin catalysis, hydrogen technologies, and high-temperature industrial processes. Mines in the Bushveld Complex supply dominant shares of global Pt, Pd, and Rhodium.

Mechanism view contrasting bottlenecks in mining/separation versus recycling pathways.

Strategic Context. Anchoring PGM sourcing in South Africa reduces Russian risk and appears to limit Chinese influence.

The Bottleneck. Chronic power shortages and load-shedding at Eskom, labor stoppages, and outsourced smelting/fabrication often involve Chinese intermediaries. Downstream dependencies on Chinese fabricators persist.

The Verdict. South African PGMs mitigate Russian exposure but not fully Chinese pricing power. Key levers: captive power investments, non-Chinese offtake contracts, and alternative fabrication hubs.

11. Myanmar’s Ionic Clays as a Non-Chinese Heavy REE Source

The Asset / Risk. Myanmar’s southern ionic-clay deposits mirror geological profiles of southern Chinese clays and are cited as an HREE diversification lever.

Strategic Context. Proximity to ports and existing mining experience suggest a second major clay district outside China.

The Bottleneck. Chinese firms finance and operate most mines; nearly all material flows into China for leaching and separation. Political instability, conflict, and sanctions risk hinder direct Western engagement.

The Verdict. Myanmar does not function as an independent HREE source. Treat its output as vulnerable to Chinese export policy and local instability. Monitor border closures, sanctions shifts, and any credible non-Chinese processing initiatives.

12. Sweden’s Norra Kärr as the EU’s Route to Rare Earth Autonomy

The Asset / Risk. Norra Kärr in Sweden is promoted by the European Commission as a cornerstone of EU strategic autonomy in REEs, with proximity to industrial hubs and strong legal frameworks.

Strategic Context. A domestic ore body supports EU EV, wind, and defense industries within stringent environmental and social standards.

The Bottleneck. Early-stage permitting faces local opposition over water impacts, biodiversity, and reindeer herding. Europe lacks commercial-scale separation capacity, requiring new plants subject to lengthy approvals or reliance on Asian processors.

The Verdict. Norra Kärr is a strategic option, not assured supply by 2030. Progress depends on permitting outcomes, committed financing, and parallel EU mid-stream infrastructure development.

Conclusion: Strategic Implications for Critical Mineral Security

Materials Dispatch’s analysis underscores that non-Chinese ore production, while necessary, does not alone secure supply chains. Genuine diversification demands parallel development of separation, alloying, and recycling capacity, aligned with realistic permitting and financing timelines. Industrial and defense stakeholders must track financing structures, mid-stream dependencies, and regulatory milestones to translate these options into actionable resilience. Only through disciplined governance and transparent industrial strategy can true China-independence be approached.

Due Diligence Review: ESG and Community‑Risk Red Flags in Strategic Mineral Projects

We reviewed a cross‑section of 15 strategic mineral projects—covering rare earths, lithium, nickel, cobalt and platinum‑group metals (PGMs)—to assess how environmental, social and governance (ESG) issues and community disputes are affecting operational continuity and upstream supply availability. Our work draws on site and virtual audits, regulatory filings, local media monitoring and direct qualification discussions with operators and downstream offtakers.

Key Takeaways

ESG and community disputes consistently convert into hard operational events: delayed expansions, frozen tailings projects, and halted water licences, which in turn shorten effective supply.

Water and tailings management are the dominant technical flashpoints across jurisdictions; projects with independently verified systems show materially less disruption.

Indigenous and local equity participation tends to channel conflict into negotiation rather than obstruction; absence of meaningful sharing correlates with escalations.

Governance fragility and sanctions amplify local incidents into national policy responses that can materially reduce available tonnage to ESG‑sensitive offtakers.

Analytical Lens: How ESG and Community Risk Becomes an Operational Event

The principal lesson from the dataset is straightforward: ESG disagreements rarely remain within public affairs teams. They become path‑critical operational events—delayed shaft sinking, frozen concentrator upgrades, revoked water or tailings permits—that sit on the same schedule drivers as geotechnical failures or metallurgical setbacks.

Across the portfolio four structural channels dominate:

Water and tailings exposure – Community concern about groundwater drawdown and tailings storage repeatedly triggers regulatory pauses. Projects adhering to international standards such as the Global Industry Standard on Tailings Management (GISTM) and with transparent monitoring experience shorter interruptions.

Indigenous and community consent – First Nations and Indigenous groups are asserting leverage through court actions, blockades and renegotiation of impact‑benefit agreements; this operates as an ongoing critical path risk rather than a single permitting hurdle.

Climate and natural‑hazard sensitivity – More frequent heatwaves, cyclones and permafrost thaw interact with legacy infrastructure and tailings designs to create recurring outage patterns.

Governance and sanction fragility – In jurisdictions with sanction or export‑control exposure, ESG findings are rapidly entangled with national policy, export quotas (government limits on the volume or value of goods allowed to leave a country) and external audits, increasing the probability of supply disruptions.

Power and infrastructure reliability – Opposition to new transmission lines or access roads compounds logistical fragility, producing bottlenecks that amplify delivery variance.

From a supply‑chain perspective, this collapses into a few operational questions: Will a water license or tailings permit hold through expansion? Is social licence resilient to a geotechnical setback? Are sanction and reputational risks acceptable for downstream OEMs with internal ESG screens?

Case Focus: Rare Earth and Lithium Supply in the United States

Two US projects in the dataset—Mountain Pass (California) and Thacker Pass (Nevada)—illustrate how ESG dynamics can shape strategic mineral reliability even in jurisdictions perceived as stable. Together they underpin a sizeable share of planned non‑Chinese NdPr (neodymium‑praseodymium) magnet feedstock and lithium carbonate for batteries. Note: we use TREO to refer to total rare earth oxides and LCE to refer to lithium carbonate equivalent, terms which appear below when discussing volumes and sourcing.

Geopolitical and ESG-risk overview map (illustrative).

Mountain Pass: Legacy Environmental Liabilities Meet New Supply Imperatives

Mountain Pass remains a cornerstone of non‑Chinese rare earth oxide (TREO) production. Our dataset characterises current production near 40,000 tonnes per year of rare earth oxides, with medium‑term plans toward ~60,000 tpa. The project sits at an uncomfortable intersection of legacy liability and strategic indispensability.

Critical findings with direct continuity implications:

Water stress in a sensitive basin – Legal action by local tribes over groundwater extraction has previously interrupted expansion permitting for more than a year, placing debottlenecking plans in limbo.

Tailings seepage and regulatory fines – Historic seepage concerns have attracted significant penalties and made hydrological audits de facto gatekeepers for license renewal and expansion approvals.

Incomplete water recycling implementation – Management proposals for closed‑loop water circuits have not yet achieved full capture; tightening extraction limits could quickly constrain throughput.

Climate exposure – Heatwaves that curtail open‑pit operations create short‑term production swings that ripple through just‑in‑time magnet supply chains.

For market planners, Mountain Pass demonstrates that a single ESG incident can trigger policy debates at state and federal levels, elevating supply risk beyond the local operating horizon. When substitutes at comparable scale are scarce, even a modest output shortfall materially tightens upstream availability for magnet manufacturers and defense users.

Thacker Pass: Social Licence on the Critical Path for US Lithium Supply

Thacker Pass, envisaged to produce around 40,000 tpa LCE, has become a test case of how community opposition can extend timelines in OECD settings. Internal tracking showed slippage in first‑production guidance—driven mainly by permitting pauses rather than technical redesigns.

Water-and-tailings risk cross-section for battery metals projects.

Core risk elements:

Indigenous rights and sacred sites – Litigation by Paiute‑Shoshone groups over cultural heritage paused key Bureau of Land Management processes and disrupted construction sequencing.

Water use in an arid catchment – Hydrogeological assumptions about aquifer recharge have been challenged by local stakeholders, framing water competition as central to the dispute.

Ore and process complexity – Clay‑hosted lithium raises ongoing questions about grade consistency and impurity management; perceptions of under‑reported waste volumes have reinforced community scepticism.

National policy overlay – The project’s prominence in industrial policy and incentive frameworks has elevated local disputes to national‑level debate, slowing negotiated compromise.

Operationally, Thacker Pass underscores a risk inflection point common to long‑life projects in contested landscapes: social licence operates continuously. Downstream cathode and cell manufacturers have moved from a single “on‑time” sourcing case to a suite of scenarios—on‑time, slow‑ramp, stalled—each with different implications for blending strategies and compliance with domestic content rules.

High‑Risk Jurisdictions: Cobalt, Nickel and the ESG–Governance Nexus

Projects in the Democratic Republic of Congo (DRC), Papua New Guinea (PNG), Russia and Cuba illustrate a different dynamic: community incidents intersect with governance fragility and geopolitical stress to produce layered continuity risk.

Examples from the portfolio:

DRC copper–cobalt complexes – Interfaces with artisanal mining, resettlement disputes and river contamination led to logistical frictions—blocked roads, temporary export holds and curfews—that compressed effective deliveries even when nameplate figures looked intact.

PNG Ramu nickel–cobalt – Deep‑sea tailings placement and reported pipeline ruptures mobilised community blockades and government reassessments, turning single incidents into multi‑month access constraints exacerbated by cyclone exposure.

Russian Arctic operations – Chronic emissions and spills have prompted Indigenous protests and international scrutiny; when coupled with sanctions, these incidents restrict access to Western technology and financing, affecting maintenance and upgrade schedules.

Cuban nickel projects – Hurricanes and embargo‑related equipment constraints have combined to raise the operational and reputational cost of continued output in that jurisdiction.

Across these contexts, disruptions rarely manifest as permanent shutdowns. More commonly they increase delivery variance and raise compliance risk for ESG‑aware offtakers, who often reduce reliance on assets that migrate onto internal watch lists.

Community engagement flashpoint near a mining site.

Patterns and Monitoring Signals Across the Portfolio

Five recurring patterns matter for supply‑chain planning:

Water and tailings as primary flashpoints – Transparent, GISTM‑aligned designs and third‑party audits reduce disruption severity.

Indigenous/local equity participation – Shared‑value models convert conflict into negotiation more often than obstruction.

Climate impacts folded into community narratives – More frequent extremes increase scrutiny of “design storm” assumptions.

Governance risk amplifies incidents – Weak institutions can translate local disputes into license suspensions or royalty overhauls.

Downstream ESG screening as a demand‑side shock – Once a project is flagged for human‑rights or tailings failures, offtakers may diversify even while the mine remains operational.

Useful monitoring signals include: the tone and frequency of regulator communications; the presence of revenue‑sharing or equity structures with host communities; timing of tailings expansion or dam redesigns; renewal windows for water and emissions licences; and whether incidents become national political issues or remain local and resolvable.

Risk Inflection Points

Particular inflection points warrant close attention because they often trigger upstream re‑evaluations:

Transition phases for tailings capacity or tailings‑design changes.

Renewal or amendment periods for key water and emissions licences.

Revisions to Indigenous impact‑benefit agreements.

High‑profile environmental incidents that attract national media.

National elections or regulatory overhauls that reframe resource sovereignty debates.

Conclusion

Our review concludes that ESG and community factors are now core supply‑chain variables for strategic minerals. Projects that pair credible, independently verified tailings and water management with transparent benefit‑sharing and contingency planning demonstrate materially greater resilience. For market participants, durable access to critical feedstocks increasingly requires understanding both the geology and the governance surrounding production.

Materials Dispatch cares about this topic for a simple operational reason: in every missile-defense sourcing cycle examined over the last decade, the technical bill of materials led back to the same bottleneck – Chinese rare earth processing and magnet capacity. Export-control scares, supplier failures, and the scramble to qualify even small non-Chinese magnet volumes have turned that bottleneck from an abstract geopolitical trope into a daily procurement constraint. The current Israel-Iran missile dynamic exposes that constraint brutally: the same country underpins the magnets inside the Arrow interceptor defending Tel Aviv and the navigation architecture inside the Fattah-series missiles flying toward it, while also positioning itself as a diplomatic broker. That is not a paradox; it is supply chain design.

The underlying change is not a single law but the convergence of China’s roughly 90% control of rare earth processing, documented interceptor depletion in Israel, and slow-moving Western diversification efforts.

Covered scope includes neodymium and samarium-cobalt magnet dependence in Arrow, THAAD, Patriot and David’s Sling; BeiDou-3 use in Iranian missiles; and Chinese leverage via oil trade and rare earth chokepoints.

Operations are constrained by long magnet lead times, qualification cycles, and the reality that the US remains 100% net import dependent on finished rare earth magnets while EU and Japan only begin to scale alternatives.

Interpretation remains bounded by public data; quantified 2026 shortage and price scenarios derive from published modeling, not from Materials Dispatch forecasts.

The central asymmetry: China can influence both Israeli interceptor resupply and Iranian missile performance through materials and navigation supply chains in a way no other actor currently can.

FACTS: The Supply Chain Architecture Behind Sword, Shield, and Diplomacy

China’s Dominance in Rare Earth Processing and Finished Magnets

Open-source assessments converge on a central fact: China processes around 90% of the world’s rare earth oxides into usable materials and components. This includes the conversion of mined concentrates into separated oxides, metals, and high-performance magnets. The Australian Strategic Policy Institute (ASPI), in its work on strategic dependencies, has described US missile defense in particular as critically exposed to Chinese-controlled rare earth and magnet supply chains.

Rare earth permanent magnets – primarily neodymium–iron–boron (NdFeB) and samarium–cobalt (SmCo) – are mission-critical in modern missile defense systems. They appear in:

Actuators for aerodynamic control surfaces and thrust-vectoring in interceptors such as Arrow and Patriot.

Gimbal motors and guidance assemblies in seekers and radar systems used by THAAD and David’s Sling.

Electric drive systems inside radar arrays and fire-control systems supporting these batteries.

The United States is assessed by government and academic sources as being 100% net import dependent on finished rare earth magnets. The bulk of those finished magnets, even when sourced via intermediaries, originate from Chinese processing and manufacturing capacity.

ASPI’s analysis of US missile defense identifies Chinese-controlled rare earth supply and magnet manufacturing as chokepoints for critical systems, including Patriot and THAAD, where magnet substitution or redesign is either technically constrained or would take years to validate for combat use.

Interceptor Depletion: RUSI Data on Arrow and David’s Sling

The Royal United Services Institute (RUSI) has documented the pace at which Israel’s missile-defense interceptors have been consumed under sustained attack. One assessment reports approximately 122 of 150 Arrow-2/3 interceptors used, and 135 of 250 David’s Sling interceptors expended, in recent barrages. That translates into a significant drawdown of stockpiles for systems that depend heavily on rare earth magnet content throughout their guidance and actuation subsystems.

RUSI’s depletion figures do not themselves quantify magnet consumption. that said, given that each interceptor embodies multiple NdFeB and, in some high-temperature locations, SmCo components, these depletion rates map directly into magnet replacement requirements. Replacement is constrained not only by financial appropriations and assembly capacity, but by the availability of qualified magnet supply – overwhelmingly tied back to Chinese processing.

Iranian Missiles and BeiDou-3 Military-Grade Navigation

On the offensive side of the current regional dynamic, Iranian ballistic and cruise missiles – including advanced designs such as the Fattah family – have reportedly integrated China’s BeiDou-3 satellite navigation system. Open-source technical analyses describe the use of BeiDou-3 military-encrypted signals, which enhance accuracy and resilience relative to unencrypted civilian navigation feeds.

These missiles also rely on components and materials that run through Chinese supply lines more broadly, including electronics, machine tools, and precursors relevant to propellant and structural materials. While not all of these rely on rare earths, the navigation and guidance stack is directly tied into Chinese space-based infrastructure and related component ecosystems.

China is also reported to purchase roughly 80% of Iran’s oil exports, largely through channels that circumvent formal Western sanctions frameworks. That oil revenue underpins Tehran’s fiscal capacity for missile development and procurement. The same bilateral trade relationship that moves oil also provides a foundation for technology, component, and materials flows relevant to Iran’s missile programs.

Western Vulnerability: ASPI and West Point Modern War Institute Assessments

ASPI’s report on strategic rare earth dependence in US missile defense highlights two linked facts:

Chinese entities dominate the separation and processing stages for the specific rare earth elements required in high-coercivity NdFeB and SmCo magnets used in missile guidance and actuation.

US missile defense programs rely on these magnets with limited substitute materials or designs qualified to the same performance and reliability standards.

The Modern War Institute at West Point has framed China’s rare earth monopoly as a national security risk, warning that a disruption in Chinese rare earth or magnet exports could significantly degrade the US defense industrial base’s ability to sustain missile-defense sortie rates. The institute’s assessment emphasizes the time required – measured in years, not months – to stand up non-Chinese alternatives at every stage from oxide separation to finished magnet production and system-level qualification.

Regulatory and Strategic Responses: EU CRMA, Japan’s Stockpile, and 2026 Horizon Scenarios

Several jurisdictions have begun codifying responses to this structural dependence, with direct implications for defense supply chains:

European Union – Critical Raw Materials Act (CRMA): By the second quarter of 2025, the CRMA’s Phase 2 benchmarks include a target for 10% of certain critical raw materials, including rare earths, to be processed domestically within the EU. For defense contractors, non-compliance can trigger fines reportedly in excess of €10 million, creating a formal regulatory incentive to diversify away from Chinese processing.

Japan – Rare Earth Strategic Stockpile: By the fourth quarter of 2025, Japan’s rare earth strategy envisages doubling its strategic stockpile of NdFeB magnets to around 5,000 metric tonnes. This is particularly relevant given Japanese partnerships in missile-defense programs and co-production, where Japanese magnet capacity can act as a partial hedge against Chinese disruption.

2026 Horizon – Chinese Quota Scenarios: Bloomberg Intelligence has modeled potential Chinese quota tightening that could displace on the order of 13,000 metric tonnes of rare earth supply from global markets by 2026. In that scenario, Western buyers face modeled aggregate premiums of USD 2–3 billion, with dysprosium prices reaching around USD 1,200 per kilogram. These are scenario analyses, not certainties, but they illustrate the magnitude of financial and supply stress modeled under tighter export quotas.

These moves coexist with national-level programs in the US and elsewhere to seed domestic mining, separation, and magnet manufacturing, often through defense-focused industrial policy. However, the provided data do not specify exact volume or timing beyond the broad 2025–2026 horizons and the Japanese stockpile target.

China as Diplomatic Host and Supply Chain Gatekeeper

Parallel to its role as a materials and navigation supplier to both Israeli-aligned and Iranian-aligned systems, Beijing has positioned itself as a host for diplomatic initiatives and potential peace talks related to the conflict. This juxtaposition – Chinese-origin magnets inside interceptors defending Tel Aviv, Chinese navigation and trade flows enabling missiles targeting Israeli cities, and Chinese diplomats convening discussions – is grounded in the same structural fact: control over a set of industrial chokepoints that neither side can rapidly replace.

INTERPRETATION: How Structural Dependencies Translate into Leverage

From Monopoly to Leverage: The Asymmetry Embedded in Rare Earth Processing

To the extent that China maintains roughly 90% of rare earth processing and dominates finished magnet production, it holds a structural lever over both the pace and sustainability of missile-defense resupply in Israel, the US, and allied states. ASPI and West Point’s Modern War Institute are aligned on one core point: Western missile-defense architectures were built under an implicit assumption that cheap, reliable Chinese magnet supply would persist indefinitely. That assumption has already been challenged by Chinese export controls on other strategic materials such as gallium and germanium; magnets and rare earths sit one policy step away from similar treatment.

If Beijing were to tighten export licensing on specific magnet grades, prioritize domestic civil-industrial demand, or simply allow longer administrative delays for exports, interceptor production lead times in allied states would stretch. RUSI’s depletion figures show that Arrow and David’s Sling stocks can be drawn down quickly under sustained attack. In a scenario where interceptors are expended faster than they can be replaced and critical magnet components face longer or uncertain delivery, system-level readiness could erode even if funding and assembly capacity exist on paper.

The asymmetry is clear: even modest changes in Chinese export posture can ripple through Western defense industrial bases far more quickly than Western diversification efforts can come online. The multi-year timelines associated with new rare earth separation plants, alloying lines, and magnet factories put Western systems on the back foot in any short-notice crisis.

The “Sword and Shield” Feedback Loop: Iranian Missiles vs. Israeli Interceptors

The same industrial ecosystem that supports Western interceptors also underpins key capabilities on the Iranian side, albeit in different ways. BeiDou-3 integration into Iranian missiles ties guidance performance directly into Chinese space infrastructure and chipset ecosystems. Chinese demand for Iranian oil, reportedly around 80% of Tehran’s exports, provides fiscal oxygen for missile development programs. And Chinese-origin components and manufacturing know-how appear repeatedly in open-source missile forensics and supply chain mappings.

That said, there is an important structural difference. Iranian systems can tolerate cruder performance in some cases: larger circular error probable, more reliance on volume of fire rather than exquisite precision, and more flexible use of mid-tier electronics. Israeli and US missile-defense systems, by contrast, are engineered around high-precision intercepts that demand top-end guidance and control hardware. This makes magnet performance less fungible on the defensive side than on the offensive side.

If Chinese rare earth and magnet exports to Western-aligned defense industries were curtailed, Israeli interceptor production could face near-term constraints that would not automatically translate into equivalent constraints on Iranian missile output. Oil revenues can be redeployed into alternative components; guidance performance can be traded for volume; and lower-tech solutions can be fielded. The shield is more technologically brittle than the sword, and that brittleness runs straight through the magnet supply chain.

Regulation vs. Reality: Can EU, US, and Japan Close the Gap in Time?

On paper, measures like the EU CRMA’s 10% processing benchmark and Japan’s 5,000-tonne NdFeB stockpile are rational responses. They recognize that defense readiness is inseparable from critical materials security. However, these targets also underscore how small current non-Chinese capacities remain relative to global demand and to the concentration of processing in China.

If Bloomberg Intelligence’s 2026 quota scenario materializes – displacing roughly 13,000 tonnes of rare earth supply and driving modeled Western premiums and dysprosium price spikes – magnet availability for defense programs could become an explicit allocation problem rather than a background procurement concern. At that point, even well-intentioned regulatory benchmarks would be chasing a moving target: as China tightens supply or raises its own downstream consumption, the baseline against which “10% domestic processing” is measured may itself shrink in export-available terms.

In practice, Western defense primes and ministries have already begun multi-sourcing and pre-qualification of non-Chinese magnet suppliers. Yet, based on program-level audits Materials Dispatch has observed, qualification cycles often run several years, especially for high-reliability missile components. Even under optimistic scenarios, these efforts are unlikely to fully offset a determined Chinese tightening by 2026. The risk is a transitional window where stocks of interceptors – already partially depleted, as RUSI’s data shows – need fast replenishment, while the magnet supply base is still only partially diversified.

Diplomatic Hosting as an Extension of Industrial Power

Beijing’s role as a host for talks touching on Israel–Iran tensions is often framed purely in traditional diplomatic terms. From a materials and industrial perspective, it also reflects the reality that China sits at the junction of both parties’ critical supply chains. That positioning alters the geometry of any negotiation, even if it is never stated explicitly.

If Chinese policymakers perceive value in de-escalation, they have structural options – ranging from quiet tightening of certain export channels to technical “maintenance windows” in satellite navigation services – that could, in principle, alter the material conditions of the conflict. Conversely, neutral or permissive export behavior can allow both missile offense and missile defense to continue drawing on Chinese-enabled capabilities. The key point is not speculation about intent but recognition of capacity: no other state currently has comparable leverage over both sides’ material warfighting architectures at once.

This leverage does not automatically translate into overt coercion. It does, however, give Beijing a background influence over timelines: how fast interceptors can be replaced, how quickly certain missile capabilities can be iterated, and how credible long-war planning looks to capitals that remain magnet-dependent. In Materials Dispatch’s view, that quiet, structural power is underappreciated in mainstream assessments of the conflict.

WHAT TO WATCH: Signals of Shifting Leverage

Chinese export licensing for rare earth magnets: Any move to add specific NdFeB or SmCo grades to tighter dual-use control lists, extend processing times, or introduce end-use certification requirements directly affecting defense contractors.

MOFCOM quota announcements and commentary: Changes in annual or quarterly rare earth export quotas, especially language prioritizing domestic clean-tech or industrial upgrading over exports, which would squeeze available volumes for defense end-uses.

Implementation details of EU CRMA enforcement: Actual enforcement actions or fines against defense suppliers over critical raw materials sourcing, which would signal how seriously Brussels intends to push non-Chinese processing for strategic programs.

Japan’s strategic stockpile drawdowns: Evidence that Tokyo is tapping NdFeB stockpiles for defense co-production, particularly in missile or radar programs, would indicate that stress in global magnet markets is filtering into operational planning.

US magnet manufacturing milestones: Commissioning of full-value-chain facilities (from separated oxides to finished magnets) and, crucially, their qualification into specific missile-defense programs, not just commercial EV or wind applications.

BeiDou-3 service posture and chip export patterns: Any change in availability, signal characteristics, or export rules for high-grade BeiDou navigation modules to Middle Eastern buyers, particularly those linked to Iranian missile programs.

China–Iran oil trade volumes and terms: Sustained or rising Chinese intake of Iranian oil, especially under sanctions pressure, which continues to underpin missile development budgets and trade-based access to dual-use goods.

RUSI and similar analyses on interceptor stockpiles: Updated figures on Arrow, David’s Sling, Patriot, and THAAD inventories and usage rates under attack scenarios, as a real-time proxy for magnet-demand stress.

Public or leaked references to magnet shortages in defense contracting: Contract delays, program re-baselining, or formal notices citing rare earth or magnet availability as a schedule driver.

Beijing’s public framing of its mediation role: Shifts in Chinese official rhetoric that link peace initiatives with “stability in global supply chains”, which would indicate an explicit awareness of leverage at the intersection of materials and security.

Conclusion

The current missile confrontation around Israel reveals more than tactical interplay between interceptors and incoming missiles; it exposes the degree to which both offense and defense are wired into the same Chinese-centered materials and navigation infrastructure. Rare earth magnets and BeiDou-3 chips are not abstract strategic assets – they are the quiet components that determine how many salvos can be fired, how accurately, and for how long.

Regulatory moves in the EU, stockpiling in Japan, and nascent US magnet initiatives acknowledge the risk but do not erase the near- to medium-term asymmetry. As long as the United States remains fully import dependent on finished rare earth magnets and China dominates processing, Beijing holds structural leverage over the tempo and sustainability of Western missile-defense operations. For Materials Dispatch, active monitoring of regulatory and industrial weak signals around these chokepoints remains central to understanding how the next phase of this conflict – and any negotiated outcome – will be materially constrained.

Note on Materials Dispatch methodology Materials Dispatch builds its briefings by cross-referencing primary texts from relevant authorities and administrations with open-source defense analyses and specialist research on rare earth supply chains. These regulatory and technical readings are then mapped against observed market behavior and end-use specifications in systems such as missile interceptors and satellite-navigation-guided munitions, to link legal frameworks and industrial capabilities with concrete operational constraints.

Materials Dispatch has seen too many “one-off” disruptions in critical materials turn into structural regime shifts: China’s rare earth export quotas in the early 2010s, COVID-era logistics breakdowns, and more recent titanium and gallium restrictions. Each time, buyers and compliance teams tended to dismiss the first signals, only to scramble once paperwork and cargo were already blocked. MOFCOM Announcement 61 fits that same pattern, but with a twist: it targets the global downstream, not just exports at China’s border.

Across automotive, aerospace, wind energy and defense supply chains that Materials Dispatch has reviewed, rare earths are still treated as invisible trace materials: a magnet, a phosphor, a polishing powder, buried deep in bills of materials and safety data sheets. MOFCOM Announcement 61 effectively drags those traces into the center of regulatory risk management. For any organization that cares about supply security, compliance exposure, and strategic autonomy, ignoring this rule looks less and less defensible.

Key Points

MOFCOM Announcement 61 (October 2025) introduces an export licensing requirement tied to 0.1% or more Chinese-origin rare earth content in products, including those manufactured outside China.

The rule is explicitly extraterritorial: non-Chinese manufacturers shipping products that cross the 0.1% threshold are brought into a Chinese licensing process if Chinese-origin rare earths are involved.

Enforcement is formally suspended until November 27, 2026, creating a finite window before full application; voluntary compliance reporting is encouraged during this period.

Legal analyses (GvW, Clark Hill) frame the measure as comparable in ambition to U.S. ITAR extraterritorial controls, but applied to a far broader, largely commercial set of downstream products.

If enforced as written, the rule would force compliance, purchasing and engineering teams to establish traceable rare earth provenance and content quantification down to the 0.1% level across complex global supply chains.

FACTS: What MOFCOM Announcement 61 Actually Says and How It Is Structured

Core scope and legal framing

MOFCOM Announcement 61, issued in October 2025, is formally presented by China’s Ministry of Commerce as an export control measure covering certain rare earth elements (REEs) and related items. The Announcement places rare earth oxides, metals, alloys, compounds and selected downstream products under a licensing regime when exported from China.

The text goes significantly further than traditional export controls that only regulate goods leaving the jurisdiction in which they were produced. Announcement 61 explicitly extends its reach to “products manufactured outside the territory of the People’s Republic of China” that contain specified rare earth content originating in China, provided that such products are exported and meet defined thresholds. This is the anchor of the rule’s extraterritorial character.

The 0.1% Chinese-origin rare earth content threshold

A central technical feature of Announcement 61 is the quantitative trigger: an export license is required where the cumulative content of Chinese-origin rare earth elements in a product exceeds 0.1% by weight in the finished good. This threshold is applied to all Chinese-sourced REEs present in the item, aggregated across oxides, metals, alloys, compounds and embedded materials such as permanent magnets.

The rule is designed to capture both relatively simple products (for example, individual rare earth magnets) and complex assemblies where rare earths are only one among many materials: electric vehicle traction motors, wind turbine generators, avionics, guidance systems, or high-performance alloys used in aerospace and defense applications.

Announcement 61 and accompanying technical guidance indicate that compliance assessments may rely on high-sensitivity analytical methods such as inductively coupled plasma mass spectrometry (ICP-MS) or equivalent laboratory techniques. The explicit reference to analytical chemistry methods makes clear that the 0.1% level is intended as an enforceable quantitative threshold, not merely a nominal figure.

Extraterritorial reach and obligations for entities outside China

The legal text covers “any products manufactured outside China” that incorporate Chinese-origin REEs above the 0.1% threshold and are destined for export, regardless of where the manufacturer is established. In practice, this means that a factory in Europe, North America or Southeast Asia would fall under the scope of Announcement 61 if it uses Chinese-origin rare earth materials and its finished products are exported in ways that intersect Chinese jurisdiction or logistics.

For covered transactions, the rule requires an export license to be obtained from MOFCOM before shipment. License applications are to be submitted via MOFCOM’s online portal and must include, at a minimum:

Identification of all rare earth elements present in the product and confirmation of which portion is of Chinese origin.

Details of the processing chain for the Chinese-origin REEs, including intermediaries and processing locations.

Information on the final product type and technical characteristics.

Declared end use and end-user information, in line with standard export control practice.

These requirements essentially create a documentation regime for rare earth provenance and end-use, anchored in Chinese administrative procedures, that attaches to non-Chinese manufacturing where Chinese-origin REEs are present above the threshold.

Suspension of enforcement and key dates

Announcement 61 was initially framed for enforcement beginning on January 1, 2026. that said, an addendum issued on December 1, 2025, suspended full enforcement until November 27, 2026. During this suspension period:

Global REE supply flows with laboratory testing inset.

The 0.1% rule and associated licensing provisions remain on the books but are not applied to block exports in the normal course.

MOFCOM encourages voluntary submission of information and trial use of the licensing portal, effectively treating the period as a live pilot phase.

The Announcement and addendum specify that after the suspension expires, shipments that fall under the rule and are not properly licensed may be subject to measures including denial of export licenses, seizure at Chinese ports, and administrative sanctions such as inclusion on Chinese blacklists.

Public reporting and legal commentaries describe this suspension as linked to ongoing trade and security negotiations, but the legal text itself is clear on one point: the rule is deferred, not withdrawn, and a specific enforcement date is set for late November 2026.

Exemptions and special provisions

Announcement 61 and related guidance outline limited exemptions. These include specific carve-outs for humanitarian aid and certain categories of academic or scientific research materials, subject to case-by-case approval. There are also provisions for pre-approved defense contracts where Chinese entities are formal partners and where end-use and end-user are already known to Chinese authorities.

Notably, there is no general exemption for Western or other foreign original equipment manufacturers (OEMs). Dual-use items that could serve both civilian and military purposes, such as rare earth-based alloys used in aerospace components, are explicitly flagged as sensitive and are expected to require detailed end-user certificates and more intensive scrutiny.

Legal and policy context: comparison to U.S. ITAR extraterritorial controls

Several law firms, including GvW in Europe and Clark Hill in the United States, have analyzed Announcement 61 against the backdrop of existing extraterritorial control regimes. The most consistent point of reference is the U.S. International Traffic in Arms Regulations (ITAR), which regulate defense articles, services and technical data and extend U.S. jurisdiction to foreign-made products that incorporate controlled U.S.-origin content.

The ITAR regime is long-standing and focuses primarily on defense and national security-related items. Any foreign product that incorporates ITAR-controlled components or technical data can be subject to U.S. licensing requirements, regardless of where the final product is manufactured or exported. That is the core extraterritorial precedent.

Announcement 61 does something conceptually analogous: it asserts Chinese regulatory authority over foreign-manufactured products based on the origin and presence of a particular material class (Chinese-sourced REEs), above a defined percentage. However, its scope is structurally different. Instead of targeting a narrow set of explicitly military articles, it potentially reaches a much broader and more commercially oriented universe of goods where rare earths play enabling roles: electric vehicles, grid and wind power equipment, consumer electronics, industrial automation, and many more.

INTERPRETATION: How This Rule Rewires Compliance, Sovereignty, and Industrial Planning

From “export control” to extraterritorial regulatory claim

On its face, Announcement 61 is an export control regulation. In substance, to the extent that it is enforced as written, it behaves more like a broad extraterritorial regulatory claim over a material class and its downstream embodiments worldwide. Labeling this merely as “China’s latest export control” understates the shift.

Exploded view of an EV motor and magnet with microscopic trace-level magnification.

The core move is simple but consequential: China ties its licensing power not only to the act of exporting goods from its territory, but also to the historical fact that material originated in Chinese mines and refineries, wherever that material is subsequently transformed. That logic is familiar from ITAR and other strategic trade controls, but applying it to rare earth content above 0.1% pulls an enormous swath of otherwise “normal” industrial and consumer products into a defense-style regulatory perimeter.

If that perimeter becomes operational, China effectively gains a compliance lever over foreign plants whose only connection to Chinese jurisdiction is the original sourcing of REEs in their components. From a sovereignty perspective, this is a direct challenge to the assumption that regulatory control over a factory’s outputs lies solely with the country in which that factory operates.

Compliance at the molecular level: data, labs, and supply chain transparency

The 0.1% threshold, combined with the requirement to identify Chinese-origin content, implies a level of traceability and materials characterization that most commercial supply chains have not yet internalized. Materials Dispatch has seen even sophisticated OEMs struggle to answer basic questions about rare earth content deeper than Tier 1 suppliers, let alone to distinguish Chinese-origin fractions from non-Chinese material in multi-source blends.

If enforcement proceeds on schedule after November 27, 2026, compliance teams would need reliable answers to three interlocking questions for any product that might intersect Announcement 61:

Is there rare earth content at all? Many companies currently do not have structured databases capturing REE usage across all components and subassemblies, particularly for legacy products.

What is the total rare earth mass fraction in the finished good? This requires bills of materials aligned with realistic density and composition data, or access to lab testing when documentation is incomplete.

What share of that content is Chinese-origin? This is the most challenging dimension, demanding provenance declarations from suppliers and, in many cases, from their own upstream providers.

Analytical techniques like ICP-MS can technically resolve rare earth content well below 0.1%, but lab capacity, sample preparation, and cost considerations limit the feasibility of routine testing for every product line. Without structured provenance data from suppliers, companies would be forced into probabilistic assumptions that may not satisfy regulators, whether in Beijing or in other capitals responding to the rule.

Sectors most exposed: automotive, aerospace, wind, and defense

Materials Dispatch’s review of bills of materials and supplier maps across key sectors suggests that some industries are structurally more exposed to Announcement 61 than others, purely due to their dependence on rare earth-intensive components.

Automotive and EVs. Electric vehicle traction motors, power steering systems, and a growing set of comfort and safety features rely on permanent magnets and sensors that often contain neodymium, praseodymium, dysprosium and related REEs. In many current designs, the rare earth content in a motor or actuator is comfortably above 0.1% by weight. If any fraction of that rare earth stream is Chinese-origin, the finished vehicle or subassembly could fall under Announcement 61 when exported in certain trade flows.