Australia Breaks the Chinese Offtake Model: Critical Minerals Sovereignty as Industrial Infrastructure

Australia is moving from being a raw material supplier into building a tightly engineered sovereignty system for critical minerals. The emerging architecture combines three levers: a national reserve for rare earths, gallium, and antimony with guaranteed price bands; the termination of Chinese offtake exposure at assets like VHM’s Goschen project; and sovereign equity via the National Reconstruction Fund’s (NRF) reported $200 million commitment to Arafura Rare Earths’ Nolans project.

The operational question is straightforward but profound: can a state-backed price floor and ceiling regime, coupled with state equity in processing, deliver reliable, non‑Chinese supply without locking miners and end users into another form of structural dependence? The answer will be determined less by high‑level strategy statements than by the way contracts, plant designs, and logistics are being re‑engineered around this new model.

For mining companies, refiners, trade policymakers, and supply chain strategists, the critical detail is not that Australia is stockpiling metals. It is that Canberra is deliberately inserting itself into the offtake stack: as buyer of last resort, source of price stabilization, and co‑owner of midstream processing. That combination changes how projects are banked, how plants are configured, and which specification sheets ultimately dominate the non‑Chinese market.

The Architecture of Australia’s National Critical Minerals Reserve

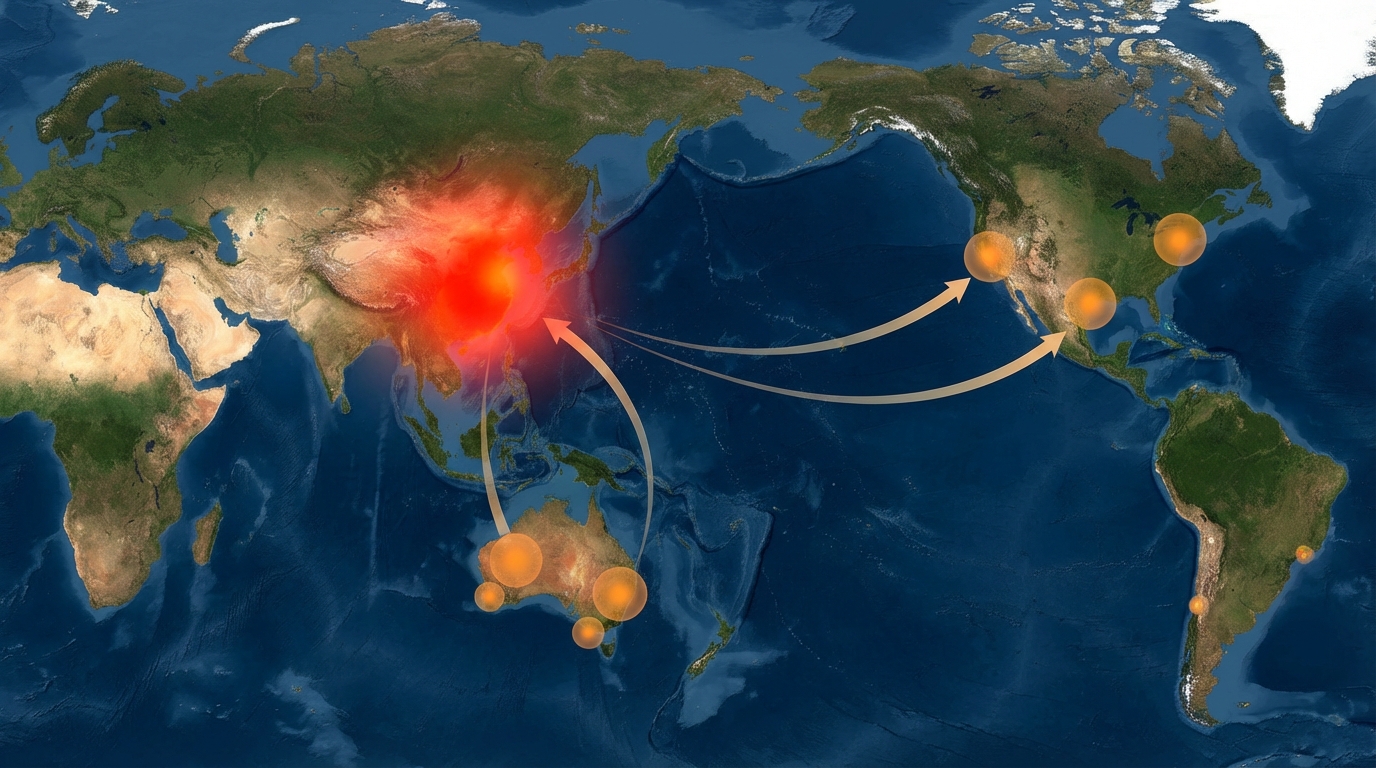

Australia’s critical minerals strategy has moved from concept papers to an emerging operational structure in which a national reserve plays a central role. Public statements and policy documents indicate a clear focus on three groups of materials: rare earths (with an emphasis on magnet materials like NdPr), gallium, and antimony. All three are metals where China currently dominates processing and downstream trade, and where export controls or informal quotas have already been deployed as policy tools.

The reserve concept departs from traditional, passive stockpiling. Instead, it is being framed as an active stabilization mechanism: government entities stand ready to buy when prices fall below a defined floor and to release stock into the market when prices exceed a defined ceiling. In practice, that creates a band around a reference price, within which normal market trading is expected to occur with reduced volatility.

Administratively, the reserve is being woven into existing critical minerals institutions. The National Reconstruction Fund, with its multi‑billion‑dollar mandate for industrial transformation, is a core funding vehicle. Implementation touches the Critical Minerals Office and the Department of Industry, Science and Resources, which oversee project qualification, ESG criteria, and domestic value‑add thresholds. Rather than simply funding mines, the system targets projects that integrate extraction and refining within Australia or allied jurisdictions.

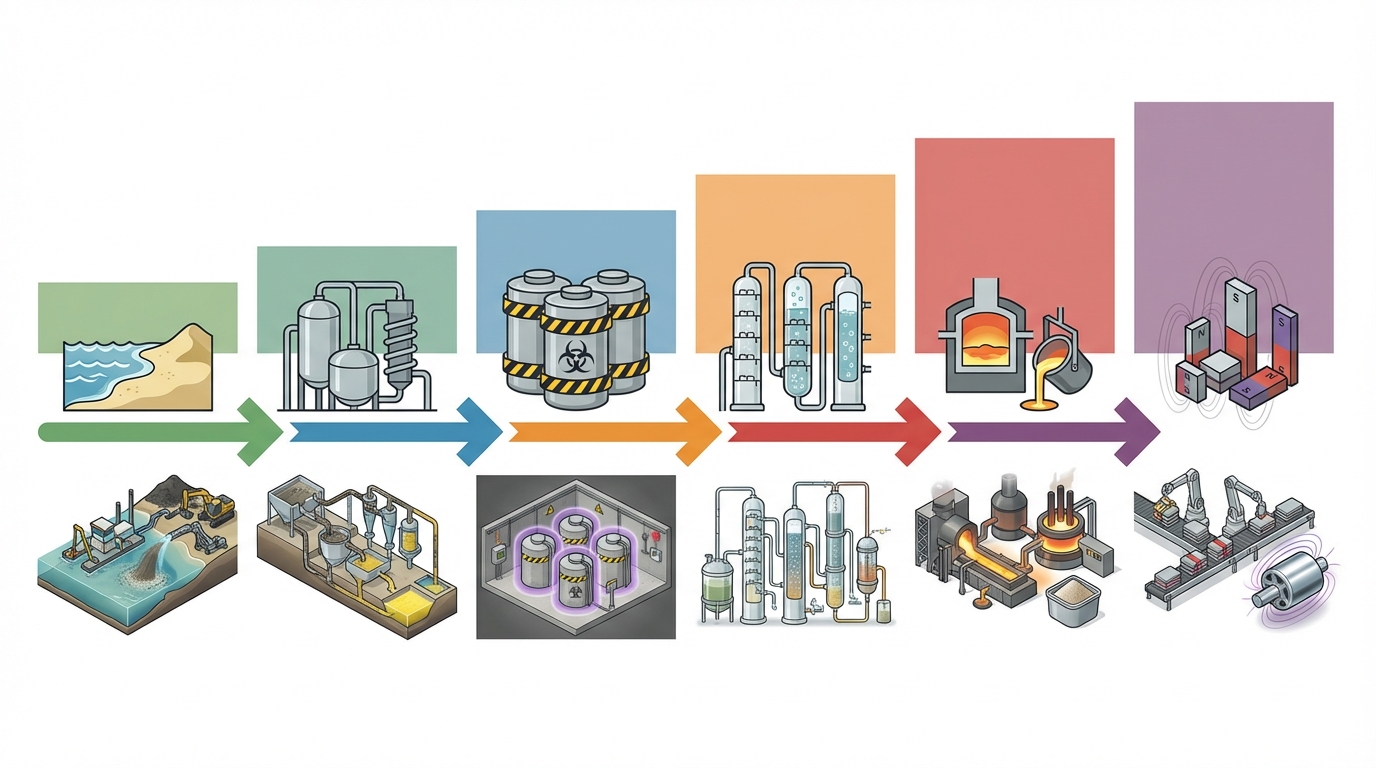

From a technical standpoint, this model turns the reserve into a quasi‑industrial customer. It will specify minimum product types and purity levels that can be accepted into the stockpile. For rare earths, that likely means separated oxides (particularly NdPr oxide and potentially didymium blends) rather than mixed concentrates. For gallium, high‑purity metal suitable for semiconductor precursor production. For antimony, refined metal or trioxide meeting alloy and flame‑retardant specifications. That technical granularity matters because it forces upstream projects to design flowsheets and quality control systems around the targeted reserve products.

Price Floors and Ceilings: How the Band Changes Project Risk

The price‑band mechanism is the real structural innovation. Traditional mining offtakes often embed discounts to volatile spot benchmarks, leaving projects heavily exposed to cyclical troughs. China’s ability to flood or constrict export volumes in rare earths, gallium, and antimony has historically turned that cyclicality into a strategic weapon. Australia’s reserve seeks to blunt that instrument by offering a transparent, rules‑based band in which sovereign purchases and releases smooth extremes.

In broad design, the floor is anchored to multi‑year average prices or cost‑based benchmarks, with an allowance for volatility. When market prices fall substantially below that anchor, reserve managers can offer to purchase qualifying material at or near the floor, subject to volume limits and compliance criteria. The ceiling works in mirror fashion: when prices materially overshoot the anchor, material from the reserve can be offered into the market, again under defined conditions, to relieve tightness.

Technically, this turns the sovereign into a large, rules‑driven counter‑cyclical trader. That role is operationally demanding. It requires:

- Transparent reference pricing, derived from a mix of exchange data, published assessments, and bilateral contract benchmarks.

- Robust assays and certification systems to ensure that purchased materials meet reserve specifications, particularly for multi‑element streams such as rare earth oxide mixes.

- Storage infrastructure for corrosive or reactive materials (e.g., antimony trioxide) that complies with environmental and safety regulations over multi‑year horizons.

- Mechanisms to rotate stock, reprocess where necessary, and avoid degradation or obsolescence against evolving downstream specifications.

From the project perspective, the presence of an accessible floor reduces the probability of “price‑floor‑breach” scenarios in loan models and internal risk cases. Life‑of‑mine plans can be calibrated around a narrower downside band. That does not eliminate market risk; it channels it. The trade‑off is clear: upside capture may be moderated when ceilings trigger, but catastrophic downside, especially from politically induced dumping, becomes less likely.

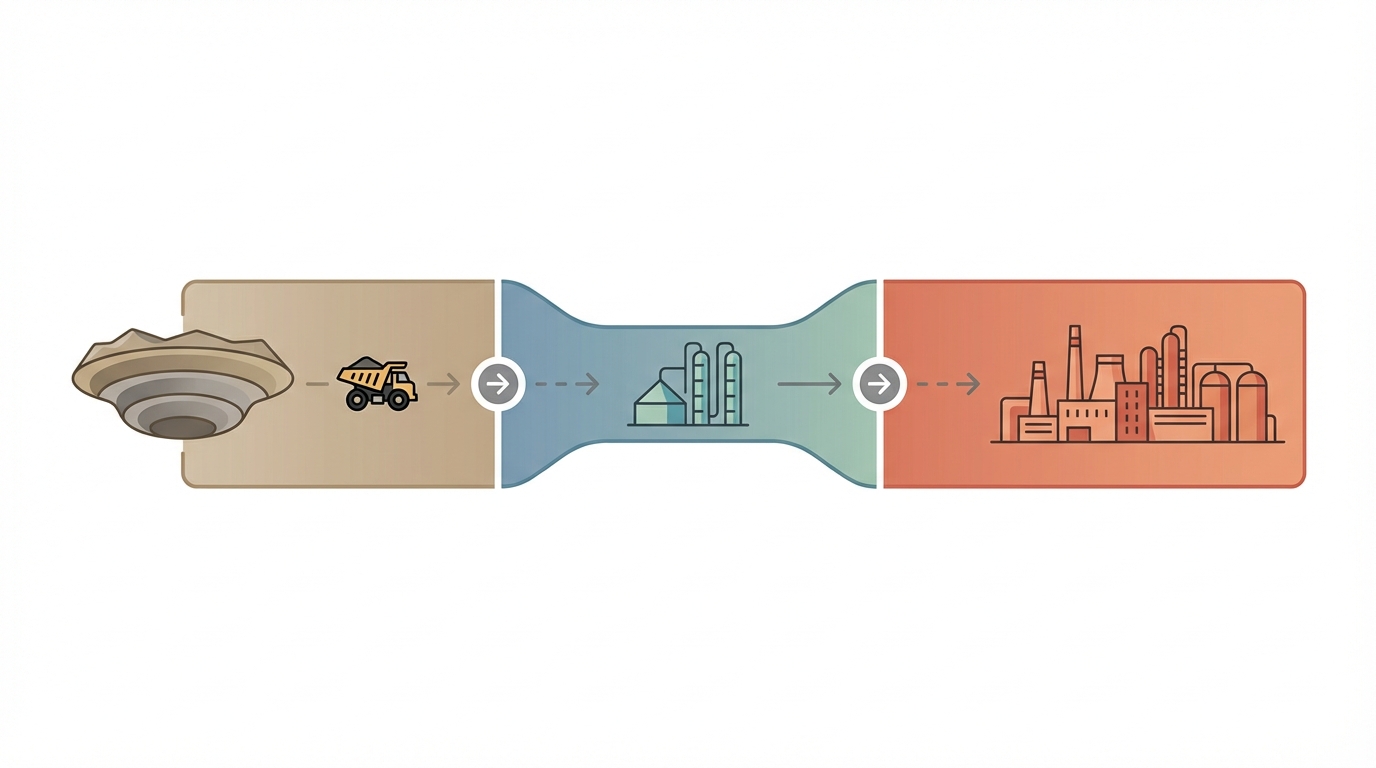

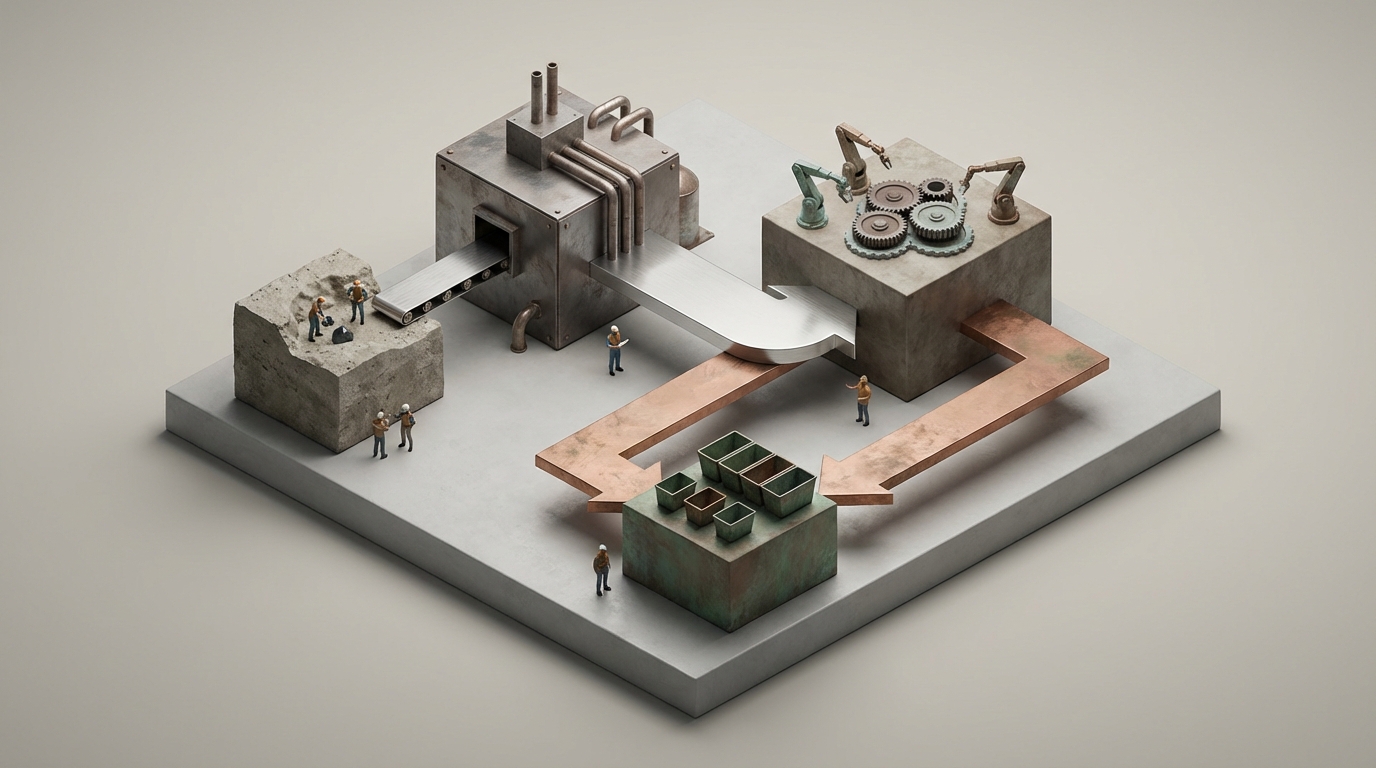

One of the more subtle implications is on flowsheet selection. With a sovereign reserve paying for material that meets defined oxide or metal specifications-even during market stress-projects have a stronger incentive to build integrated hydrometallurgical and separation capacity domestically, rather than exporting intermediate concentrates for Chinese refineries to upgrade. The price band effectively underwrites the additional OPEX and CAPEX friction that comes with building and running complex SX (solvent extraction), ion exchange, calcination, and reduction circuits in high‑cost jurisdictions.

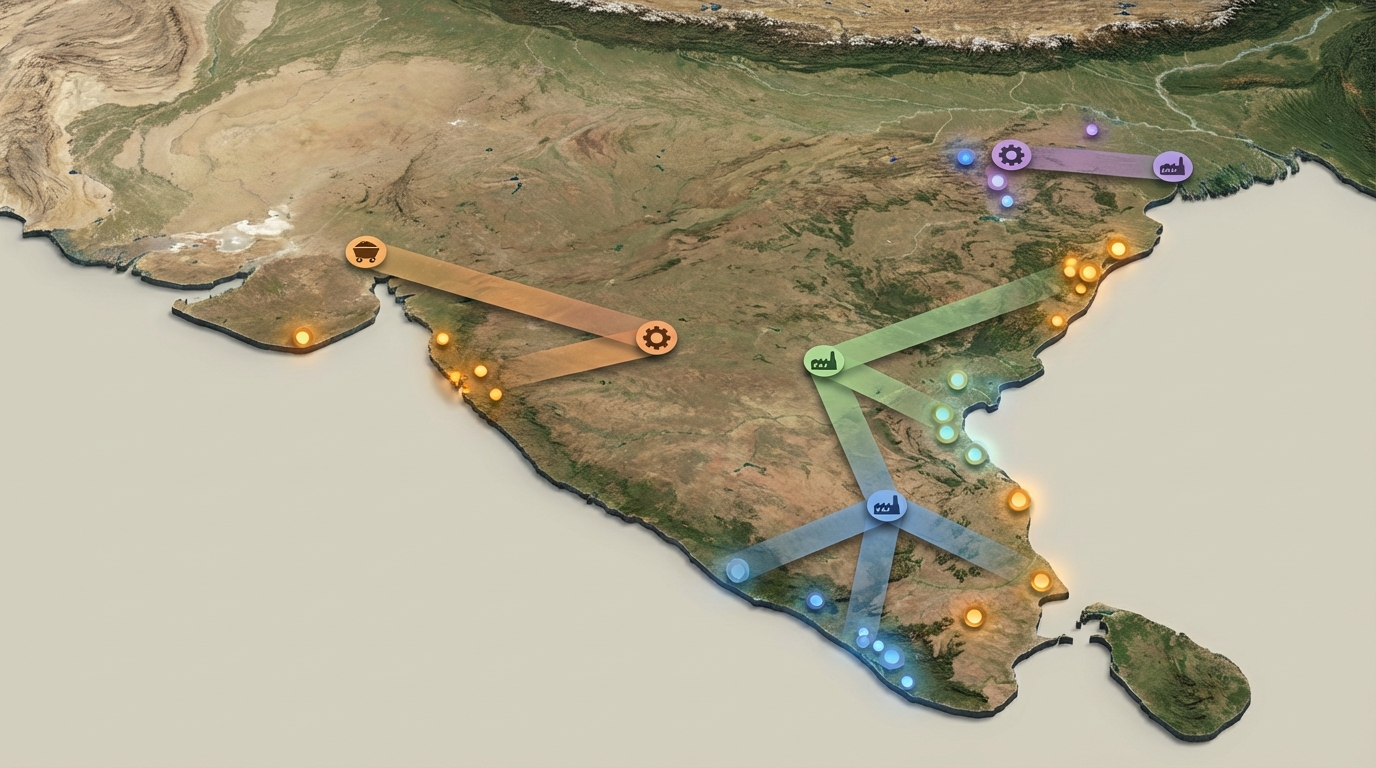

Case Study: VHM’s Goschen Project and the Shenghe Offtake Termination

The VHM-Shenghe episode is the first visible break point where Australia’s sovereignty architecture has collided with the legacy Chinese offtake model. VHM’s Goschen project in Victoria is a multi‑commodity mineral sands and critical minerals development that had previously been advancing under an offtake understanding with China’s Shenghe Resources-a company deeply embedded in the global rare earth refining system.

The termination of that offtake agreement signalled more than a bilateral commercial dispute. It reflected a deliberate strategic pivot: willingness by an Australian developer to forego the perceived security of a Chinese refinery buyer in favour of alignment with domestic policy and allied demand. For antimony and other critical elements associated with Goschen’s flowsheet, this is a non‑trivial decision. Shenghe’s ecosystem offers large installed processing capacity, established impurity‑tolerant flowsheets, and global marketing channels. Stepping away from that infrastructure forces Goschen’s developers to build or access alternative midstream solutions.

In practical terms, the termination reshapes the technical and logistical planning envelope for Goschen:

- Product specification path: Instead of targeting specifications optimised for Chinese refineries (which can accommodate certain impurity profiles and deliver further separation in‑country), Goschen must now match the needs of Western refineries or end‑use alloy and magnet producers. That can change the design of beneficiation, leaching, and impurity removal steps.

- Process selection: If antimony and other critical by‑products are to be sold into a reserve or to allied industrial customers, the plant may need additional roasting, leaching, and refining steps to deliver higher‑purity outputs locally, rather than shipping complex concentrates.

- Logistics and port strategy: Where a single Chinese offtaker could have taken mixed streams to a few large refineries, a diversified offtake and reserve strategy creates a more complex outbound logistics pattern, with different bagging, containerisation, and certification requirements per product.

- Permitting and ESG alignment: A shift away from China‑bound concentrates toward refined products made in Australia exposes the project more intensively to domestic scrutiny on emissions, waste, and reagent use, especially for high‑temperature or acid‑intensive circuits.

The national reserve is not a direct replacement for Shenghe’s role, but it changes the calculus for Goschen’s sponsors and lenders. The presence of a credible sovereign buyer of last resort for certain antimony or rare earth streams can underpin offtake diversification away from a single Chinese counterparty. However, it also introduces policy risk: eligibility criteria, ESG conditions, and price band parameters are subject to political and regulatory evolution over the project life.

This is where the Goschen case becomes emblematic. It shows that decoupling from Chinese offtakers is not only a geopolitical statement. It is a commitment to re‑engineering the entire value chain—from ore sorting and tailings handling to SX circuit design and port logistics—to be compatible with Western specifications and sovereign buyer frameworks, rather than Chinese refiner requirements.

Case Study: Arafura’s Nolans Project and the $200 Million National Reconstruction Fund Stake

If VHM’s Goschen illustrates the break with the old model, Arafura Rare Earths’ Nolans project demonstrates what the new model looks like when sovereign capital steps in. The NRF’s reported $200 million commitment to Nolans is more than a balance‑sheet boost. It effectively binds the project’s midstream to Australia, aligning it with the national reserve, allied offtakers, and domestic industrial policy.

Nolans, located in the Northern Territory, is designed as an integrated mine‑and‑refinery operation focused on magnet rare earths, particularly neodymium and praseodymium (NdPr). Unlike projects that ship concentrates offshore, its flowsheet encompasses beneficiation, cracking, leaching, impurity removal, solvent extraction separation, and final oxide production. That depth of processing is technically demanding, energy‑intensive, and capital hungry—precisely the type of infrastructure that is difficult to finance on conventional terms when the market is dominated by Chinese refineries with lower operating costs and deeply amortised plants.

With NRF equity and associated policy backing, Nolans is being positioned as a cornerstone of non‑Chinese NdPr supply. That has several operational consequences:

- Product quality targets: Nolans is oriented toward high‑purity NdPr oxide suitable for sintered and bonded permanent magnet production. That implies tight control of deleterious elements such as thorium, uranium, and certain transition metals. SX circuit design must achieve high separation factors while maintaining acceptable reagent consumption.

- Energy and reagent logistics: The integrated flowsheet requires sustained supplies of acid, base, extractants, and power in a remote setting. Grid extensions, on‑site generation (potentially gas‑hybrid or renewable‑hybrid), and dedicated chemical supply chains are all part of the underlying infrastructure challenge.

- ESG and waste handling: Domestic processing means that all residues, including mildly radioactive tailings and neutralised process liquors, fall under Australian regulatory regimes. That drives design choices around lined tailings storage, zero‑liquid‑discharge or high‑recovery water circuits, and long‑term monitoring obligations.

- Offtake structure: With sovereign equity involved, offtake negotiations are naturally influenced by policy objectives. Contracts with allied magnet makers or automotive OEMs may need to align with the reserve’s price‑band logic and with broader industrial strategies (for instance, commitments to local magnet manufacturing over time).

From a resilience perspective, Nolans offers something that Chinese‑centred supply cannot: deep transparency on ore provenance, environmental performance, and labor standards, combined with contractual access to a sovereign‑backed price and volume framework. The trade‑off is higher operating cost and more complex operational risk. Australia’s wager is that for defense, automotive, and grid‑scale applications, end users will value predictable, policy‑aligned supply over the marginal cost advantage of Chinese material.

Gallium and Antimony: From By‑Products to Strategic Reserve Metals

Gallium and antimony are often treated as minor by‑products in mining project narratives, but they sit at the core of Australia’s reserve strategy. Both are emblematic of the vulnerabilities exposed by China’s export control and quota playbook.

Gallium is predominantly recovered as a by‑product of bauxite/alumina and zinc processing. Its strategic value lies in compound semiconductors (GaAs, GaN) for radio‑frequency electronics, power electronics, and optoelectronics. China currently dominates both primary production and high‑purity refining. When Beijing moved to restrict exports of gallium‑related products, it highlighted how dependent advanced semiconductor and defense applications had become on a small number of refineries.

Australia’s response targets two levers. First, improving by‑product recovery from existing alumina and base metals operations, potentially through retrofit of solvent extraction or electrolytic recovery stages. Second, building high‑purity refining capability to reach semiconductor‑grade gallium (multiple “nines” purity). Both steps are technically non‑trivial: gallium occurs in low concentrations, and upgrading to ultra‑high purity involves repeated refining, tight contamination control, and specialised equipment.

The reserve gives operators an anchor customer for these upgraded streams. Instead of relying solely on volatile niche demand from a handful of overseas gallium processors, Australian facilities can supply a portion of output into the national stockpile at the agreed floor. That changes the business case for installing and running high‑purity circuits on relatively modest tonnages, where unit costs can otherwise be prohibitive.

Antimony has a different profile but an equally strategic role. It is used in flame retardants, lead‑acid batteries, certain alloys, and military applications ranging from munitions to specialty solders. Supply has been heavily concentrated in China and, more recently, in Myanmar and a small number of other jurisdictions subject to political instability and regulatory risk.

Production routes for antimony typically involve mining stibnite (Sb2S3), followed by roasting and smelting to produce metal or trioxide. These steps are energy‑ and emissions‑intensive, generating SO2 and other pollutants that are increasingly difficult to permit in high‑regulation jurisdictions. Australian projects that can co‑produce antimony with gold or other metals—such as those around Victoria—therefore face a familiar challenge: export concentrates to existing Asian smelters, or invest in cleaner domestic processing solutions that comply with strict local standards.

The reserve’s antimony target is intended to anchor domestic refining. The availability of a sovereign outlet for refined antimony or antimony trioxide at a known floor price strengthens the case for incorporating modern roasting, gas scrubbing, and hydrometallurgical refining onshore. Over time, that can support allied supply chains for munitions, flame retardant manufacturers, and specialized alloy producers who are under pressure to decouple from inputs tied to unstable or non‑aligned jurisdictions.

How Australia’s Model Compares with US and EU Critical Minerals Approaches

Australia is not the only jurisdiction seeking to reduce dependence on Chinese critical mineral supply, but its chosen instruments differ in important ways from US and EU approaches. The contrast is less about rhetoric and more about the plumbing of support mechanisms.

In the United States, the toolkit has centred on Defense Production Act authorities, the Defense Logistics Agency (DLA) stockpile, and tax or grant support via legislation such as the Inflation Reduction Act. The DLA acquires materials for defense needs, but generally does not operate a formal price‑band regime. Instead, offtake agreements and purchase contracts are used to support specific projects (for example, rare earth operations) at agreed pricing structures, often with emphasis on availability rather than explicit market stabilization.

The European Union, through the Critical Raw Materials Act and related initiatives, has emphasised accelerated permitting, designation of strategic projects, and co‑funding of processing and recycling infrastructure. EU work on strategic stocks is ongoing, but again, the focus has been more on ensuring the existence of stockpiles and diversified suppliers than on inserting the state as a continuous price‑band operator.

Australia’s emerging framework can be contrasted along several dimensions:

| Dimension | Australia | United States | European Union |

|---|---|---|---|

| Core Instrument | National reserve with explicit price floor/ceiling band; sovereign equity and debt via NRF | DLA stockpile; project‑specific offtakes; grants and loans under DPA/IRA | Critical Raw Materials Act; strategic project status; co‑funding of processing and recycling |

| State Role in Pricing | Active counter‑cyclical buyer and seller within a defined band | Contractual support; limited explicit market‑wide price targeting | Focus on volumes and capacity; less emphasis on price bands |

| Processing Mandate | Strong emphasis on domestic or allied midstream refining, linked to NRF support | Preference for North American processing but with broader geographic flexibility | Priority for EU‑based processing and recycling, with recognition of allied supply |

| Key Metals Targeted | Rare earths, gallium, antimony, plus broader critical minerals list | Rare earths, battery materials (lithium, nickel, cobalt, graphite), others | Broad CRM list with specific benchmarks for extraction, processing, recycling |

| Decoupling Mechanism | Explicit reduction of Chinese offtake exposure; support for alternative offtakes and reserve intake | Diversified projects and offtakes; restrictions on Chinese‑linked entities in some segments | Supplier diversification; scrutiny of strategic Chinese investments; emphasis on permitting and ESG |

The quotable difference is this: Australia is not just subsidizing capacity; it is attempting to rewrite the reference contract for critical minerals by embedding the state inside the pricing mechanism itself. That approach creates a clearer path for mines like Nolans or Goschen to proceed with domestic processing, but it also concentrates price‑setting risk in Canberra’s hands.

Operational Trade‑Offs, Failure Modes, and Compliance Risks

Any system that offers guaranteed price support carries inherent risk of miscalibration. For the Australian reserve, there are three critical failure modes to monitor.

1. Structural Floor Dependence. If floors are set too generously or remain in place for prolonged periods, mines and refiners can become structurally dependent on sovereign purchases rather than competitive commercial offtakes. That creates a quasi‑permanent subsidy, complicating WTO compliance debates and potentially slowing the development of robust, diversified private demand. It also exposes public finances to extended support for operations that may struggle to achieve global cost competitiveness.

2. Ceiling‑Induced Opportunity Loss. If ceilings are set too low relative to bull‑market conditions, producers may be constrained in capturing high‑price periods that are important for recouping capital. For rare earths, gallium, and antimony, where price spikes can be short but pronounced in response to geopolitical shocks, the ability to harvest those spikes can materially affect corporate resilience. A misaligned ceiling risks undercutting that flex while still leaving producers exposed to input‑cost inflation.

3. Specification and ESG Mismatch. The reserve’s acceptance criteria will reflect stringent Australian ESG and quality standards. Projects designed around historical Chinese offtakes may need significant retrofits—additional impurity removal, emissions controls, water‑treatment capacity—to deliver acceptable material. If these retrofits are underestimated, projects may technically qualify for the reserve on paper but struggle in practice to produce sufficient compliant tonnage, undermining both project economics and reserve stocking goals.

There are also non‑trivial regulatory and trade policy risks. Other producers or trading partners could argue that price‑band interventions constitute trade‑distorting subsidies if they materially influence export prices. Careful design—such as limiting reserve purchases to domestic consumption or allied strategic uses, and ensuring transparent, rules‑based operations—will be central to mitigating these challenges.

On the operational side, the technical demands of managing physical stockpiles at scale should not be underestimated. Rare earth oxides can absorb moisture and CO2, altering properties over long storage periods if packaging and warehouse conditions are inadequate. Gallium’s low melting point and reactivity require specific containment and handling protocols. Antimony compounds pose toxicity risks and demand robust ventilation and dust‑control in storage facilities. Failures here would translate into quality downgrades, write‑offs, or environmental incidents that could erode public and industrial support for the reserve mechanism.

Strategic Scenarios and Signals to Watch

The intersection of the national reserve, the VHM-Shenghe offtake termination, and the NRF‑backed Nolans build‑out creates a new operating environment for critical minerals in Australia. Several structural scenarios are emerging.

Consolidation into an Australian‑Centric Supply Hub. In this scenario, Nolans and Goschen succeed in commissioning robust domestic processing, gallium recovery expands at alumina and base‑metal facilities, and antimony refining achieves environmentally compliant scale. The reserve operates as intended, smoothing volatility without crowding out private offtakes. Allied industrial users—particularly in Japan, Korea, Europe, and North America—lock in long‑term contracts linked to the Australian price band, using it as a reference benchmark alternative to Chinese sources.

Reserve Overreach and Distorted Signals. A more problematic scenario sees price bands routinely triggered, with the reserve absorbing large volumes in downturns and struggling to release them without depressing future prices. Projects lean on the sovereign outlet rather than building out diversified customer bases. Chinese suppliers respond tactically, undercutting the floor for key customers in third countries, leaving Australian material heavily reliant on government support. The model achieves short‑term survival but not true strategic autonomy.

Partial Decoupling and Dual‑Track Markets. A more nuanced outcome has Australia and its allies establishing a parallel, policy‑aligned market channel with higher transparency and ESG standards, while a China‑centred channel continues to operate at lower costs and higher volatility. Material from projects like Nolans flows predominantly into the allied channel, sometimes at a premium, while parts of the global market remain linked to Chinese refiners’ pricing and offtake practices.

Across these scenarios, several weak signals deserve close monitoring:

- The number and scale of further terminations or renegotiations of Chinese‑linked offtakes by Australian critical minerals projects, following the VHM–Shenghe example.

- The detailed rulebooks governing how price floors and ceilings are set, adjusted, and communicated for rare earths, gallium, and antimony.

- The specific product specifications (purity, form, packaging) adopted by the reserve for each metal, which will cascade back into mine and refinery design decisions.

- Announcements of allied industrial offtakes explicitly referencing Australian reserve‑linked pricing or NRF‑backed projects as anchor supply sources.

- Any early operational or environmental incidents at domestic processing plants handling complex rare earth, gallium, or antimony streams, which could tighten regulatory constraints.

Conclusion: A New Reference Contract for Critical Minerals

Australia’s critical minerals strategy is transitioning from policy language to a concrete operating framework centred on three pillars: a price‑banded national reserve, deliberate decoupling from Chinese offtakers as exemplified by the VHM–Shenghe Goschen break, and sovereign equity in midstream processing through moves like the NRF’s $200 million Arafura stake at Nolans. Together, these measures redefine not just where rare earths, gallium, and antimony are mined and refined, but how they are priced, contracted, and stockpiled across the non‑Chinese ecosystem.

The trade‑off is clear. Australian material backed by this architecture is unlikely to be the absolute lowest‑cost in the market. However, it can offer a different value: transparent provenance, policy‑aligned reliability, and a state‑engineered buffer against the most violent forms of price and volume coercion. For industrial users where failure to secure inputs would disrupt national security or critical infrastructure, that value proposition is non‑trivial.

Materials Dispatch’s assessment is that Australia is effectively attempting to write a new reference contract for critical minerals supply—one in which the state is not an occasional supporter but a permanent, rule‑bound participant in both pricing and processing. Whether that contract becomes the template for allied jurisdictions, or a uniquely Australian experiment, will hinge on how the first tranche of projects and reserve operations handle the inevitable shocks of the coming decade. Our team is actively monitoring weak signals in offtake renegotiations, reserve rule‑making, and allied procurement standards that will indicate which way this experiment is breaking.

Note on Materials Dispatch methodology Materials Dispatch integrates close monitoring of official policy releases (such as Australia’s Critical Minerals Strategy), trade and export control bulletins from agencies including MOFCOM and allied regulators, and market data from specialized critical minerals price reporting. This is cross‑checked against the technical requirements of end‑use sectors—from magnet performance specifications to semiconductor purity thresholds—to assess how policy instruments like price‑banded reserves translate into real‑world operational resilience.