Tech Deep Dive: The Role of Hafnium, Tantalum, and Other ‘Niche’ Tech Metals

Hafnium, tantalum and a small group of “niche” tech metals sit awkwardly in critical minerals debates. They are often mentioned in footnotes, yet they define the temperature limits of jet engines, the reliability of defense electronics, and the neutron control of naval reactors. Market narratives usually track mine output and country shares. The technical reality is more specific: availability is governed by a handful of complex, hazardous refining flowsheets and by‑product relationships that do not respond quickly to price signals.

This article takes a process‑first view. It examines how hafnium and tantalum are actually produced, what equipment and reagents are required, and where the true bottlenecks form along the upstream-midstream-downstream chain. It also situates them alongside other niche metals such as niobium, rhenium, scandium and yttrium, which share similar execution risks: small volumes, technically demanding separations, and tight coupling to other commodities. In effect, this is a tech deep dive: the role of hafnium, tantalum, and other ‘niche’ tech metals seen through separation chemistry, operational constraints and regulatory pressure.

1. Why These Metals Matter Technically

Across aerospace, semiconductors and defense, performance breakthroughs often come from trace elements measured in tenths of a percent. Hafnium and tantalum sit precisely in that category: volume is small, but design windows are narrow and specifications are unforgiving. Substitution is technically possible in some applications, but it is neither fast nor risk‑free.

1.1 Hafnium: Grain Boundaries, Neutrons and Gate Dielectrics

Hafnium is a classic by‑product metal. It occurs as a few percent within zircon (ZrSiO4), substituting for zirconium in the crystal lattice. Its industrial importance stems from three properties:

- High temperature performance in superalloys: In nickel‑based and cobalt‑based superalloys, small additions of hafnium strengthen grain boundaries and improve creep resistance and oxidation behaviour at turbine inlet temperatures. This is especially important in single‑crystal and directionally solidified blades used in advanced jet engines and industrial gas turbines.

- Exceptional neutron‑capture cross section: Hafnium’s nuclear cross section makes its alloys natural candidates for control rods in reactors, including naval propulsion systems. That use requires extremely tight control of impurities, particularly zirconium, which has very different neutron behaviour.

- High‑k dielectric oxides: Hafnium oxide (HfO2) became the workhorse “high‑k” material in advanced CMOS gate stacks. Thin HfO2 films allow lower leakage currents at small node sizes. This use is volume‑relevant but heavily dependent on ultra‑high purity precursors.

Across these applications, volumes are modest but quality thresholds are extreme. Superalloy producers require tight control of oxygen, nitrogen and zirconium content; nuclear‑grade hafnium requires a different impurity profile than alloy‑grade; semiconductor fabs need parts‑per‑billion level control of metallic contaminants in hafnium precursors. That combination of low tonnage and high purity is structurally difficult to manage.

1.2 Tantalum: Charge Density and Corrosion Resistance

Tantalum’s industrial profile is defined by two main roles: high‑reliability capacitors and corrosion‑proof components in aggressive chemical environments. It also contributes meaningfully to high‑temperature alloys, but in a somewhat more substitutable fashion than hafnium.

- Capacitors: Tantalum powder sintered into porous pellets, anodized to form a thin Ta2O5 dielectric, delivers extremely high capacitance per volume. This is critical for space‑constrained, high‑reliability electronics in defense, aerospace, medical implants and certain automotive systems. While ceramic and aluminium electrolytic capacitors compete in many applications, tantalum remains preferred where long‑term stability and surge resistance matter.

- Superalloys and hardmetals: Tantalum additions increase high‑temperature strength and phase stability in nickel, cobalt and iron‑based alloys. Tantalum carbides form some of the hardest known materials, blended into cutting tools and wear parts.

- Chemical equipment: Tantalum’s resistance to most acids (especially at elevated temperature) makes it valuable for heat exchangers, reactor linings and fittings in the chemical and pharmaceutical industries.

The critical point is reliability: for many defense and aerospace electronics, tantalum is selected less for performance on day one than for predictable behaviour on day 5,000. That makes simple material substitution much more complex than theoretical performance tables suggest.

1.3 Other “Niche” Tech Metals in the Same Risk Family

Hafnium and tantalum are part of a broader family of low‑volume, high‑impact metals which share similar industrial behaviour:

- Niobium (Nb): Co‑occurs with tantalum in columbite‑tantalite ores; used in high‑strength low‑alloy steels, superconducting magnets and superalloys.

- Rhenium (Re): Critical for some of the highest‑temperature single‑crystal turbine alloys; mainly recovered as a by‑product of molybdenum refining.

- Scandium (Sc): Used in aluminium‑scandium alloys for aerospace and additive manufacturing; typically recovered as a by‑product from laterite or uranium streams.

- Yttrium and other heavy rare earths: Essential in lasers, phosphors and some ceramic matrix composites.

What unites these is not periodic table position but industrial structure: small global flows, heavy reliance on by‑products, high capital intensity in midstream refining, and significant regulatory scrutiny around either radiation or conflict sourcing.

2. Upstream Geology and Mining Constraints

Geology is rarely the binding constraint for these metals. Resources are relatively widespread. Instead, the binding constraints are technology, co‑product economics and governance in mining jurisdictions.

2.1 Tantalum Ores: Pegmatites, Coltan and Artisanal Flows

Tantalum occurs mainly in complex oxide minerals such as columbite‑tantalite (“coltan”), tapiolite and various tungsten‑bearing phases. Broadly, two upstream paradigms dominate:

- Hard‑rock pegmatites: Operations in Australia (for example, Greenbushes and Bald Hill) and parts of Brazil exploit granitic pegmatites where tantalum is either a primary target or a by‑product of lithium and tin. These mines are typically open‑pit or shallow underground operations using drill‑and‑blast, followed by crushing and dense media separation or spirals.

- Alluvial and eluvial deposits: In the Great Lakes region of Africa (DRC, Rwanda, Burundi and neighbouring countries), tantalum is often produced from weathered pegmatites as alluvial or eluvial concentrates. A significant share has historically come from artisanal and small‑scale mining (ASM), with simple tools and minimal mechanisation.

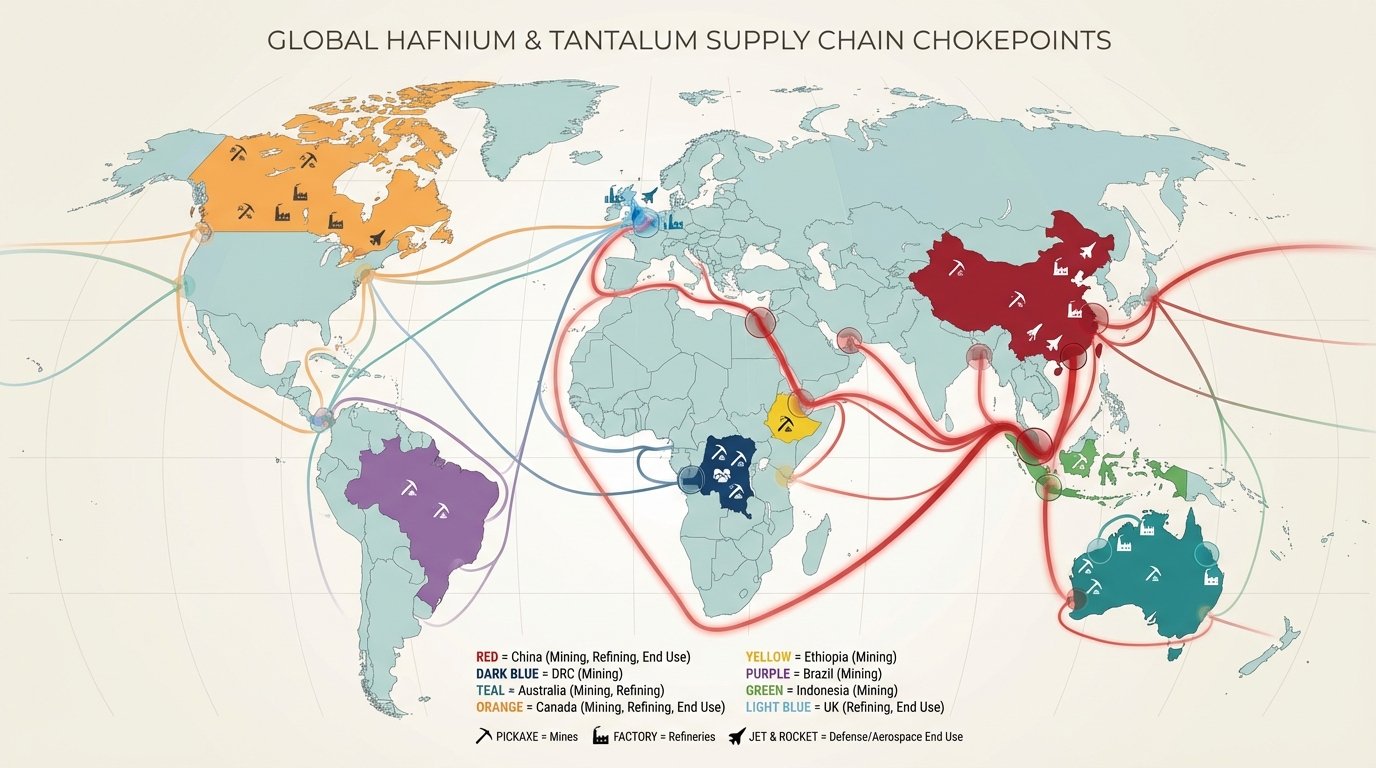

Hard‑rock operations tend to offer better grade control, more predictable production and easier integration with industrial ESG frameworks. ASM‑dominated supply, by contrast, brings acute compliance challenges. Conflict‑affected and high‑risk areas require supply chain due diligence under OECD guidance, and both U.S. Dodd‑Frank and EU conflict minerals regulations have tightened disclosure obligations for tantalum sourcing.

An additional structural feature is co‑product dependence. In many pegmatite systems, tantalum is a by‑product of lithium or tin. When lithium prices drive mine planning, tantalum output becomes a secondary consideration. That decouples tantalum availability from tantalum pricing and makes forecasting supply more complex.

2.2 Hafnium: Locked into Zirconium and Heavy Mineral Sands

Hafnium is not mined as a standalone commodity. It is derived almost entirely from zircon, a heavy mineral found in coastal placer deposits and some inland paleoshoreline systems. These same deposits also host ilmenite, rutile and leucoxene, which are feedstocks for titanium dioxide and titanium metal.

Upstream, heavy mineral sand operations in Australia, South Africa, Mozambique, China and a few other jurisdictions dredge or dry‑mine sand, concentrate heavy minerals by gravity and magnetic separation, and produce zircon and ilmenite concentrates. The zircon is sold into ceramics, refractories and foundry markets, or routed into zirconium chemical plants. Hafnium availability is thus structurally coupled to demand and pricing for zirconium and titanium products, not to hafnium demand itself.

This coupling creates an important non‑linearity. If construction cycles or pigment markets dampen zircon demand, zircon production may fall even if hafnium prices rise. Conversely, a boom in zircon demand can generate more hafnium feedstock than midstream separation circuits are sized to handle. That is why hafnium discussions that focus purely on “ore reserves” ignore the true constraint: separation capacity and willingness to invest in small, technically demanding side‑streams.

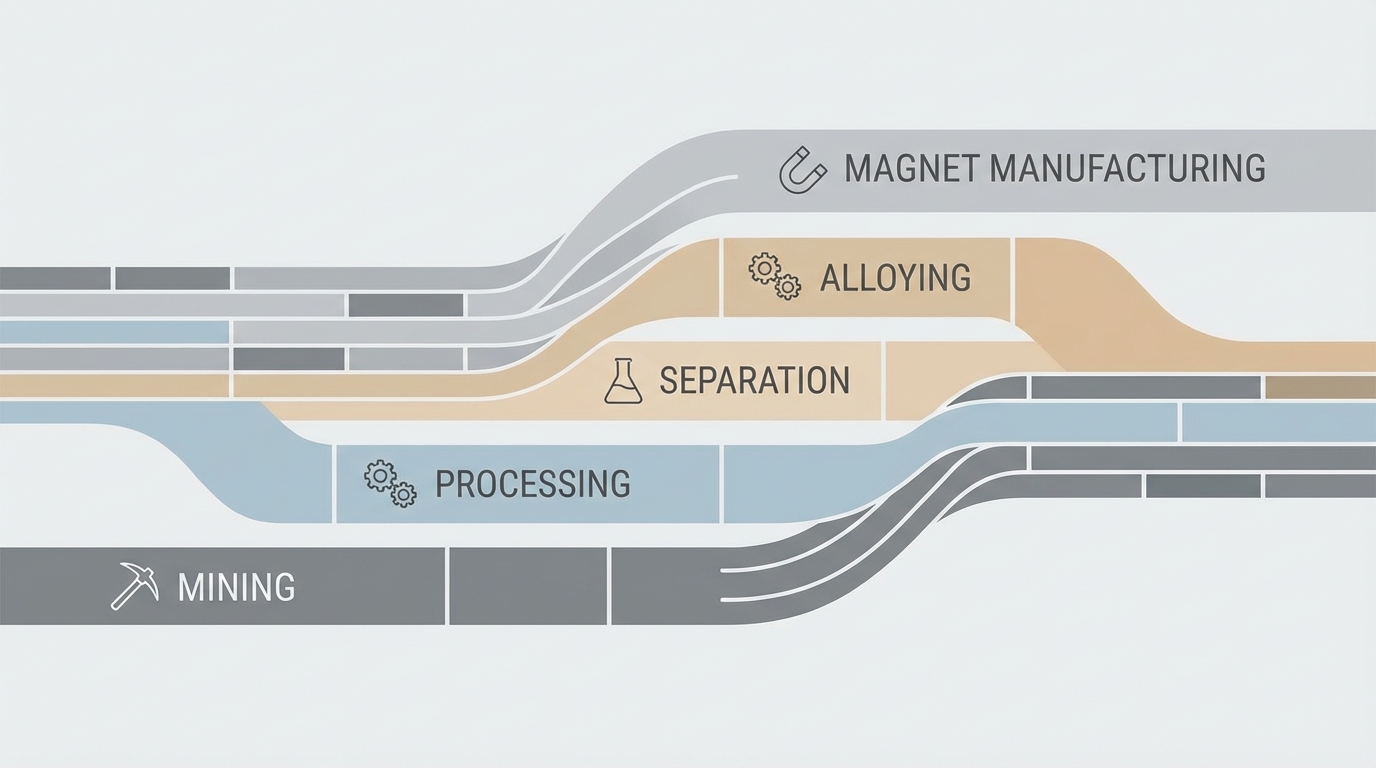

3. Refining and Separation Technologies: Where the Real Bottlenecks Sit

Both hafnium and tantalum owe their supply risk profile to midstream chemistry. Their primary ores are complex, refractory oxides. Extracting a saleable metal requires multiple stages of digestion, separation and reduction, often involving hazardous reagents. These flowsheets are capital‑intensive and heavily regulated, which naturally concentrates capacity into a small number of specialized plants.

3.1 Tantalum and Niobium: Gravity, HF Chemistry and Solvent Extraction

Industrial tantalum production can be broken into three broad stages: mineral processing, chemical separation, and metal production.

- Mineral processing: Crushed ore or alluvial concentrate is upgraded using gravity separation (spirals, shaking tables, multi‑gravity separators) and magnetic or electrostatic separation. The goal is to produce a concentrate with elevated Ta2O5/Nb2O5 content and reject as much silica and iron as possible. Typical circuits handle throughputs from a few tonnes per hour in small hard‑rock plants to significantly higher volumes in integrated lithium‑tantalum operations.

- Chemical digestion: The tantalum‑niobium concentrate is digested using hydrofluoric acid (HF) alone or in combination with sulphuric or hydrochloric acid. This stage produces complex fluoride species such as H2TaF7 and H2NbF7. The digestion step is highly exothermic and handled in corrosion‑resistant reactors (e.g., PTFE‑lined or tantalum‑clad equipment).

- Solvent extraction / ion exchange: Because tantalum and niobium chemistry is closely similar, separation requires multi‑stage solvent extraction with organophosphorus extractants, or ion‑exchange resins engineered for selectivity. Dozens of extraction and stripping stages are commonplace in commercial plants to achieve high‑purity separation.

- Oxide and metal production: After separation, tantalum is precipitated, calcined to Ta2O5, then reduced (often using sodium or aluminium) to produce tantalum metal powder or ingot. Powder is further processed (agglomeration, deoxidation, sizing) for capacitor‑grade material, typically achieving purities in the “3N” range (around 99.9%) or higher.

Each stage has distinct execution risks. HF consumption and off‑gas scrubbing drive operating cost and environmental compliance. SX circuits with dozens of mixer‑settlers require careful hydraulic, phase separation and crud management to maintain metal recovery and purity. Reduction reactors operate at high temperatures and demand stringent safety procedures for sodium or other strong reductants. Unplanned downtime at any of these stages reverberates rapidly through capacitor powder supply.

3.2 Hafnium: Extracting Parts per Hundred from Zirconium Streams

Hafnium separation is an extreme case of “difficult neighbours” on the periodic table. Zirconium and hafnium share nearly identical ionic radii and chemical behaviour, yet nuclear applications require them to be separated to very low residual fractions. Industrial flowsheets so focus on maximising an inherently small separation factor through very large numbers of stages.

- Zirconium feed preparation: Zircon concentrate is chlorinated or fused with alkali to produce zirconium tetrachloride or zirconium oxychloride. Hafnium follows the same chemistry and remains mixed through this stage.

- Solvent extraction: Multi‑stage extraction using organophosphorus extractants (for example, tributyl phosphate or more specialised ligands) partitions hafnium and zirconium between organic and aqueous phases. Hundreds of theoretical stages may be required for stringent nuclear specifications, leading to large solvent inventories and complex plant hydraulics.

- Hafnium purification and reduction: Hafnium‑rich streams are further purified, converted to hafnium tetrachloride or oxide, and reduced (e.g., by the Kroll process with magnesium) to sponge, then melted to ingot in vacuum or inert atmosphere furnaces. Additional remelting (electron beam or plasma) can achieve extremely low gas and metallic impurities for critical applications.

The result is a highly specialized, small‑volume operation typically co‑located with a zirconium plant. Hafnium supply is not constrained by ore; it is constrained by the willingness of zirconium producers to invest in, permit and operate a demanding side‑stream that handles aggressive chlorides and organics for very limited tonnage. This structural reality explains why global hafnium production is concentrated in a small number of plants in a few jurisdictions.

3.3 Energy, Water and Waste: Hidden Drivers of Capacity

Separation technologies for both metals are energy‑ and reagent‑intensive. Although public data on kWh per tonne for individual plants is limited, several general patterns are clear:

- Thermal steps concentrate energy use: Rotary kilns for calcining Ta/Nb oxides, chlorination furnaces for zircon, and vacuum melting systems for ultra‑high‑purity hafnium all operate at elevated temperatures and significant specific energy consumption.

- HF and chloride management dominate environmental engineering: Fume scrubbing, wastewater neutralisation and fluoride/chloride waste handling add both capital and operating cost. Scaling up capacity implies not just more reactors, but larger treatment plants and more complex residue storage solutions.

- Water is a hard constraint in arid regions: Gravity separation, solvent extraction and wash stages consume large quantities of water. In Western Australian pegmatite operations, for example, water balancing and recycling infrastructure can be as critical as ore grade in determining feasible throughput.

These factors collectively explain why capacity expansions are measured in years and why idle or legacy circuits are often hard to restart. Equipment corrosion, solvent degradation and changing environmental standards mean that “nameplate” capacity on paper often overstates what can be safely and compliantly operated without substantial refurbishment.

4. Structural Chokepoints and Geopolitical Exposure

The chokepoints for hafnium and tantalum sit mainly in the midstream: refining and separation capacity is geographically concentrated, and often controlled by a small number of firms which face tightening environmental and trade scrutiny. Upstream mining adds an additional layer of geopolitical complexity in tantalum’s case.

4.1 Tantalum: Conflict Minerals, ASM and Processing Concentration

Tantalum’s supply chain is often summarised as “Africa mines, Asia refines.” That is a simplification, but it captures two central realities:

- Conflict‑linked ore streams: Coltan from parts of the DRC and adjoining regions has historically funded armed groups. This triggered regulatory responses such as Dodd‑Frank Section 1502 in the U.S. and the EU Conflict Minerals Regulation, which explicitly cover tantalum. Smelters handling ore from these regions now operate under extensive due‑diligence and audit regimes (e.g., Responsible Minerals Initiative protocols).

- Concentrated refining: Chemical digestion and solvent extraction capacity for Ta/Nb is concentrated in a limited number of industrial clusters, including parts of East Asia and Europe. Many Western OEMs remain indirectly dependent on these processors even when purchasing from “clean” mine sources.

Efforts to re‑route supply through lower‑risk jurisdictions such as Australia, Brazil and Canada have led to new or restarted pegmatite operations, including lithium‑tantalum mines where tantalum is a by‑product. However, these flows often still rely on a small set of refiners that handle HF‑based chemistry at scale. Disruptions can come from localised events (e.g., plant outages, environmental enforcement actions) just as easily as from geopolitical tensions.

4.2 Hafnium: Small Volumes, Few Plants, High Leverage

Compared with tantalum, hafnium’s upstream geology is less politically charged, but midstream concentration is even more pronounced. Only a handful of zirconium producers operate dedicated hafnium separation units. Some of these are in jurisdictions that are the focus of broader technology‑export debates, while others are in countries aligned with Western defense supply chains.

Because global hafnium volumes are low, even relatively small absolute disruptions can have outsized effects on downstream users. A maintenance shutdown at a single separation plant, or a change in export licensing requirements, can tighten availability for turbine blade alloyers and nuclear component manufacturers simultaneously. In practice, large OEMs respond by qualifying multiple alloy suppliers and by building material buffers, but those buffers primarily mitigate short‑term shocks rather than structural under‑investment in separation capacity.

4.3 Regulatory Overlays: From Conflict Minerals to Export Controls

Both metals face an expanding overlay of regulatory attention that affects operational decisions throughout the chain:

- Conflict minerals and due diligence: Tantalum smelters and downstream manufacturers are subject to conflict mineral reporting in major markets. This drives traceability programmes, blockchain pilots and third‑party audits. The result is a bifurcation of the supply chain: approved, auditable flows that command a premium, and marginal, often ASM‑derived flows that struggle to find compliant outlets.

- Environmental regulation: HF use, fluoride emissions, tailings with thorium/uranium and chloride off‑gases are all under increasing regulatory pressure. Permit conditions for new plants are tighter, and older facilities often face upgrade mandates. These requirements directly affect capital budgets and timelines for any capacity expansion.

- Export controls and industrial policy: Recent export restrictions on other niche metals such as gallium and germanium have raised awareness that similar measures could apply to hafnium, tantalum or associated processing technologies. At the same time, Western governments have launched critical mineral strategies, including funding for new Ta/Nb and Hf projects and recycling.

The net effect is to turn what might seem like simple commodity flows into highly conditional, compliance‑loaded value chains. For materials that represent only trace weight fractions in final goods, the administrative burden is disproportionately large relative to tonnage.

5. Technology Innovation and Diversification Pathways

Hafnium and tantalum supply risk has triggered two broad categories of response: process innovation to make refining safer and more flexible, and demand‑side adjustments to reduce exposure. Neither category eliminates risk, but both alter the structure of bottlenecks.

5.1 HF‑Lean and HF‑Free Flowsheets for Ta/Nb

HF is the central hazard in conventional tantalum and niobium refining. It drives equipment cost (exotic alloys, PTFE linings), worker safety concerns, and wastewater treatment complexity. Several technology trends seek to reduce this dependence:

- Alternative lixiviants: Research and pilot‑scale work has examined chloride‑based or alkali‑based digestion systems, where concentrates are decomposed using sodium hydroxide or other reagents, followed by selective leaching. These flowsheets can reduce HF consumption but often trade that gain for increased energy use or more complex solid-liquid separation steps.

- Advanced ion‑exchange materials: New resin systems aim to improve tantalum/niobium selectivity at milder conditions, potentially reducing the number of SX stages. This is particularly attractive for small‑scale plants in jurisdictions with strict environmental permitting.

- Modular refining units: Containerised or skid‑mounted circuits for small Ta/Nb streams are being explored, especially for by‑product recovery from tin and lithium operations. Modularisation helps align capital cost with the modest tonnage typical of such streams.

From an execution standpoint, the main question is not whether such technologies exist in principle, but whether they can be run at industrial uptime and purity levels. Many flowsheets that look attractive on paper stumble at the interface between aggressive chemistry and real‑world maintenance environments.

5.2 Hafnium: Incremental Debottlenecking and Recovery from New Streams

For hafnium, radical new flowsheets are less visible than incremental debottlenecking and broader feed integration:

- Debottlenecking existing plants: Upgrades to mixer‑settlers, replacement of aged solvent, improved process control and better integration with zirconium lines can yield modest increases in effective separation capacity without entirely new plants.

- Recovery from alternative zirconium sources: Interest is growing in hafnium recovery from non‑traditional zirconium streams (for example, zirconium by‑products from nuclear fuel, or unconventional heavy mineral sands). These options often hinge on local regulatory acceptance of handling slightly radioactive or contaminated feeds.

- Recycling: Superalloy recycling and reclaim of hafnium‑bearing scrap offer a small but strategically meaningful supplementary stream. Vacuum remelting and powder metallurgy routes can integrate recycled material with careful quality control.

Because hafnium circuits are small, even modest improvements in recycling yields or feed integration can materially change available tonnage to aerospace and nuclear customers. The limiting factor is not always technology readiness, but rather the economic incentive to handle complex scrap and to manage its traceability.

5.3 Demand‑Side Adjustments and Substitution

On the demand side, engineers and materials scientists have pursued several levers to reduce exposure to fragile supply chains without sacrificing performance.

- Tantalum capacitors: Higher‑capacitance ceramic capacitors, niobium‑based systems and improved circuit designs can, in some cases, reduce reliance on tantalum components. Nonetheless, in high‑reliability, high‑temperature environments, tantalum remains entrenched because of decades of field data.

- Superalloy design: Some high‑temperature alloys have been reformulated to reduce critical element content (including rhenium and, in some cases, tantalum or hafnium) while maintaining performance through microstructural optimisation. Additive manufacturing also changes the material‑efficiency equation by reducing machining scrap.

- Alternative high‑k dielectrics: For semiconductors, hafnium oxide remains dominant, but research into alternative high‑k materials and stack architectures continues, partly motivated by both electrical and supply considerations.

Historical experience suggests that substitution typically reduces, rather than eliminates, demand for niche metals. Materials shift from broad use into fewer, but even more critical, roles where their unique properties are irreplaceable.

6. Operational Implications Across the Value Chain

From an operational perspective, the key insight is that hafnium and tantalum exposures are less about headline ore reserves and more about the interplay of by‑products, hazardous chemistry and compliance frameworks. Different segments of the value chain face distinct constraints.

6.1 Aerospace and Defense Superalloys

Jet engine and industrial gas turbine manufacturers rely on hafnium‑ and tantalum‑bearing superalloys for turbine blades, vanes and some hot‑section hardware. Qualification cycles for new alloys or new melt shops are long, involving extensive mechanical testing, creep data generation and, in aerospace, certification processes.

This long qualification tail means that even when alternate alloys or suppliers are technically feasible, practical switching speed remains slow. As a result, alloy producers place significant emphasis on:

- Secured feedstock streams from multiple refining regions to reduce exposure to any single jurisdiction or plant.

- Scrap management and revert programmes, where offcuts and used blades are carefully segregated and recycled into new melts, capturing residual hafnium and tantalum.

- Strategic engagement with zirconium and Ta/Nb refiners to understand capacity utilisation, maintenance plans and regulatory risks that might affect availability.

In practice, the bottleneck often appears not at the mine or even at the metal ingot stage, but at the interface between refined metal and certified alloy production capacity, where vacuum melting and powder metallurgy lines run near full utilisation.

6.2 Electronics, Capacitors and Semiconductor Supply Chains

For electronics, tantalum’s main exposure is in capacitor powder and wire. The number of certified powder producers and wire mills is limited, and each is tied to particular refining circuits and ore streams. The capacitor industry has historically experienced pronounced cycles when incidents at a small number of powder plants reverberated through device pricing and lead times.

Semiconductor use of hafnium, by contrast, hinges on chemical precursor supply rather than bulk metal. Metal‑organic and halide precursors for atomic layer deposition (ALD) require extremely high purity. Even if bulk hafnium metal is available, converting it into semiconductor‑grade precursors involves additional purification and synthesis steps, often in highly specialised facilities. Any contamination incident can force batch rejections and temporary shutdowns, amplifying the impact of upstream hiccups.

6.3 Risk Scenarios: What Breaks First

When assessing fragility in these supply chains, several structural failure modes recur across scenarios:

- Disruption in HF or reagent supply: Tightening HF regulation, accidents at fluorochemical plants, or trade restrictions on specialty reagents can indirectly constrain Ta/Nb refining. Plants built around specific reagent supply chains have limited short‑term flexibility.

- Sudden loss of a key refining site: Environmental enforcement, safety incidents or geopolitical measures targeting one large Ta, Nb or Hf separation plant can remove a significant share of global refining capacity overnight. Given the multi‑year timelines for building new SX circuits and effluent treatment, this is not easily replaced.

- Upstream co‑product shock: Closure or curtailment of a lithium‑tantalum pegmatite, a tin mine supplying coltan‑rich tailings, or a zirconium producer facing pigment demand swings can unexpectedly tighten feedstock for tantalum or hafnium even when their own demand is stable.

- Regulatory shock in ASM‑dominated regions: Stricter enforcement or political instability in ASM‑heavy tantalum jurisdictions can rapidly reduce ore availability that had previously flowed through semi‑formal channels.

Historical episodes in other niche metals – such as the effect of export restrictions on gallium and germanium – illustrate how quickly downstream industries can re‑rate the risk profile of small‑tonnage materials once trade policy enters the picture. Hafnium and tantalum sit in a similar position, with the added complexity of hazardous chemistry and conflict‑linked sourcing.

7. Conclusion: What Really Drives Hafnium and Tantalum Risk

Hafnium and tantalum are often framed as “minor” metals, yet from a technical standpoint they are system‑critical. The analysis above highlights three structural conclusions.

- Geology is not the primary constraint. Both metals occur in multiple regions and deposit types. The real limits are by‑product economics and midstream separation capacity built for other commodities (zirconium, lithium, tin).

- Hazardous chemistry concentrates refining. HF‑intensive flowsheets, solvent extraction with large organic inventories and aggressive chlorination discourage a wide base of entrants. A small number of operators carry the environmental, technical and financial burden, creating natural chokepoints.

- Compliance frameworks reshape trade flows. Conflict‑mineral rules for tantalum and tightening environmental standards for both metals mean that not all theoretical supply is practically accessible to high‑reliability end‑users.

For aerospace, defense and advanced electronics supply chains, hafnium and tantalum risk is therefore best understood as a question of process infrastructure and regulatory exposure, not just tonnes in the ground. Materials Dispatch continues to track weak signals that can disproportionately affect these metals: changes in HF regulation, new Ta/Nb flowsheet announcements, shifts in zirconium plant investment, and any move to extend export controls to additional niche tech metals.

Note on Materials Dispatch methodology Materials Dispatch integrates open‑source policy monitoring (including trade and export announcements by agencies such as MOFCOM and Western trade authorities), production and trade data from geological surveys and customs statistics, and close reading of end‑use technical standards in aerospace, nuclear and electronics. This triangulation focuses less on headline tonnages and more on the specific process steps and qualification bottlenecks that actually constrain industrial continuity.